Market entry strategies of technology providers with own mobile payment solutions – opportunities for banks through a cautious approach

KEY FACTS

-

Technology providers are launching mobile payment solutions (wallets) in conjunction with schemes and national card providers

-

The analysis of Apple Pay market entries has shown a significant decline in transaction fees for issuers, indicating that the primary aim of technology providers is to generate a sufficiently sizable user base and not necessarily to generate earnings with these services; an accelerated global market presence could be achieved by adjusting the initial fees model

-

Leading banks have recognized these developments and are achieving better terms by conducting intensive negotiations and/or gaining independence by developing their own solutions

REPORT

The virtual payment market is in a state of flux due to the increasing importance of e-Commerce and contactless payments at the point of sale. This results from the increasing prevalence of NFC-enabled terminals and the simultaneous provision of mobile payment solutions (wallets) by technology providers. Along the conventional processing structure comprising schemes and issuers, a third kind of player is establishing itself: technology providers such as Apple, Samsung and Google are joining forces with international credit card companies to successfully provide end consumers with mobile payment solutions on their devices, and are, therefore, gaining even more ground on global markets.

The tech companies are pursuing a variety of strategies to tap into new markets: Samsung and Android Pay for example are forcing rapid market penetration by focusing on the comprehensive placement of their products with customers and pursuing an aggressive fees strategy in the form, that the usage of the wallet is free of charge for both card providers and end customers.

While Apple Pay is also free of charge for end customers, a charge applies to the issuing banks. Participating credit card providers agree to transaction fees depending on the conditions of the national market. On the one hand, partnerships of this kind represent an opportunity for issuing banks to offer their customers an innovative and global mobile payment solution. On the other hand, the providers are making themselves reliant on technology companies and are handing over at least a part of their customer interface to them.

The strength of Apple’s market position and the extent of its assertiveness – even whilst facing opposition – were demonstrated with the reversal of Barclay’s decision to not support Apple Pay in the UK – a move that strengthened Apple’s negotiating position in the long term. On the other hand, the global rollout is proving to be extremely time-consuming and is being increasingly hampered by a decreasing adoption rate on the part of customers in established Apple Pay markets. Between June 2015 and January 2016, for example, the relative share of users in the US using Apple Pay regularly after trying it out once fell from 19% to 15%.

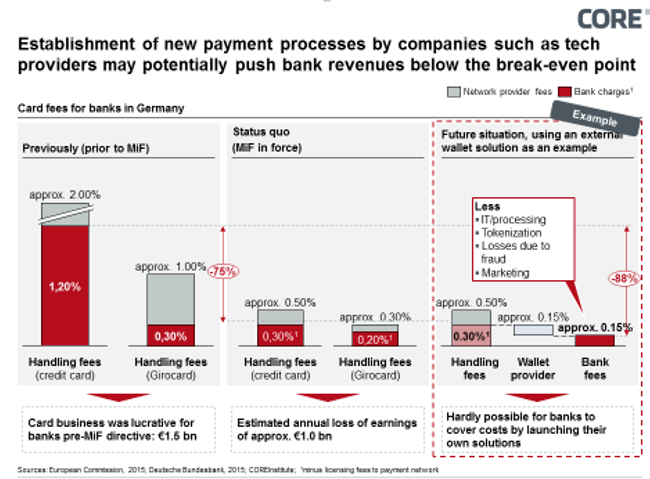

Figure 1: Card fees for banks in Germany

At the same time, completed market launches of Apple Pay point to the following trend:

- When Apple Pay was first launched in the US in 2014, the usage fee for issuers stood at 15 basis points of turnover.

- Just eight months later, when the service was launched in the UK in July 2015, participating credit card companies were already demanding significant reductions in fees.

- When the service went live in China on February 18, 2016, a fee of 7 basis points was agreed with the banks participating in the rollout.

This corresponds to only roughly half of the fees charged to US banks and is even better in the light of a two-year moratorium.

This trend could be viewed as Apple’s response to an intensification of the market situation caused by fierce competition with Android and Samsung Pay. Samsung Pay, for instance, has not only been active in Apple’s domestic market since September 2015, it has also announced plans for a rollout to Australia, Singapore and Spain in 2016. As a result, Apple and Samsung will potentially be competing in four shared target markets by the end of the year.

It may be assumed that it is critical to Apple’s success to tap into new markets and thus build up a sufficiently large user base, and it cannot be ruled out that the company aims to achieve this by marginalizing transaction fees in future market entries.

Looking beyond the market environment, the negotiations between Apple and Chinese banks started back in 2014 suggesting that the intensity of negotiations with issuers represents a determining factor in the level of fees and that it pays off for banks to be patient.

Leading banks have recognized these developments and are currently attempting to achieve better starting points and conditions – as they recently did in Germany, Canada and Australia – by conducting intensive negotiations while developing their own solutions. In turn, it will be interesting to see whether the local competitors in each country find common responses to their newly arriving global rivals or whether the competition is stepped up between previous systems, newer systems and the technology providers.

In summary, it may be assumed that financial institutions with experienced negotiating teams, clear corporate objectives in terms of payment transactions and an efficient IT setup are in a better position to delay the loss of current revenues and instead to harness the potential of these innovative technologies and tap into new market share.

SOURCES

Finextra, Chinese banks charged half the fees levied by Apple Pay on US banks, 2016,

Graham Spencer, The State of Apple Pay, 2015, https://www.macstories.net/stories/the-state-of-apple-pay/

Arnold Martin, UK banks put squeeze on Apple Pay fees, 2015

www.ft.com/intl/cms/s/0/02287f44-2a3d-11e5-8613-e7aedbb7bdb7.html

Zhang Yuzhe, Chinese Banks to Pay Much Smaller Fees to Apple Pay than U.S. Counterparts, 2016,

http://english.caixin.com/2016-02-22/100911334.html

Malarie Gokey, Everything you need to know about Samsung Pay, 2016,

http://www.digitaltrends.com/mobile/samsung-pay-news/

Kesh, 2015, http://www.kesh.de/

Paydirekt, 2016, https://www.paydirekt.de/

Jon Fingas, Apple Pay finally becomes useful in Canada, 2016, http://www.engadget.com/2016/05/10/apple-pay-gets-wide-support-in-canada/

David Glance, Apple Pay in Australia: Customers lose out and all parties share the blame, 2015,

Meet our authors

Expert EN - Fabian Meyer

As Managing Partner at CORE, Fabian Meyer is responsible for the implementation of complex IT projects with a focus on digitalization projects in the banking industry. He has several years of consu...

Read moreAs Managing Partner at CORE, Fabian Meyer is responsible for the implementation of complex IT projects with a focus on digitalization projects in the banking industry. He has several years of consulting experience in the banking sector and in transformation engineering.