AliPay – the main silent competitor for digital payment solutions

KEY FACTS

-

AliPay, which currently has 450 million customers, processes 34% of the total billing volume of 860 billion Dollars outside China

-

To respond effectively to Chinese tourists in Europe, a push has been made to increase the number of sales points in Europe that accept AliPay through partnerships with Wirecard (February 2016), Concardis (June 2016), Ingenico (August 2016) and SIX (December 2016)

-

AliPay has the potential to become a significant threat to the customer interface, currently provided through banks and underlying earnings, without actively being noticed.

REPORT

Changing customer needs, the liberalization of regulations, and the related digitalization of the payment market are having an ever greater effect, as seen in the proportional increase in the use of mobile payment methods. This being the case, it is expected that the global customer base will have increased by ~51%, and the volume of transactions by ~85% by the end of 2020.

In anticipation of this trend, globally active technology firms are setting their sights on the potential returns in tandem with direct access to the customer interface through the aggressive placement of digital payment solutions such as AliPay, Apple Pay, Android Pay, and Samsung Pay.

In terms of its customer base, AliPay, the payment method introduced by online retailer Alibaba, stands out because of its leading position in China (currently 450 million customers), which is three times the customer base of PayPal and significantly larger than that of Apple Pay.

In recent years, Alibaba has focused on the national market where it has a share of ~80%, processing payments worth 568 billion Dollars mainly within China via its own AliPay app in 2015. However, the rise of the middle class, and the ensuing exponential increase in this group’s readiness to travel, has led to positive growth in payments outside the country to the tune of 292 billion Dollars . This means that ~34% of AliPay’s total transaction volume is already processed abroad, and this is acting as a catalyst for expansion on the European market.

- February 2016: Partnership with Wirecard – Wirecard develops the app scanAliPay to allow AliPay to be accepted on mobile terminals without the need for cash register integration. Traders across Europe are able to accept and process AliPay transactions by scanning the QR code.

- June 2016: partnership with Concardis – Concardis, one of the leading payment providers in Europe, integrates AliPay within its comprehensive trader portfolio. The Concardis solution is directly integrated into the retailer’s existing equipment, so no additional infrastructure is needed. The activation of the AliPay solution is carried out through a normal software update and upon the retailer signing the acceptance contract.

- August 2016: partnership with Ingenico – the Ingenico Group integrates AliPay into its in-store payment gateway, meaning the acquiring partners throughout Europe are able to offer AliPay to the merchants behind it.

- December 2016: partnership with SIX – the agreement between the Alibaba Group and SIX allows traders whose SIX terminals are NFC-capable to accept AliPay across Europe.

Alibaba Group is currently still focusing on making access to AliPay for Chinese tourists in Europe as easy as possible. However, in the next few years, there is a significant danger that the rapid increase in locations where it is accepted will enable it to undergo an aggressive transition as a competing product in the various national markets, thus driving the banking sector out of the core of the digital payment market.

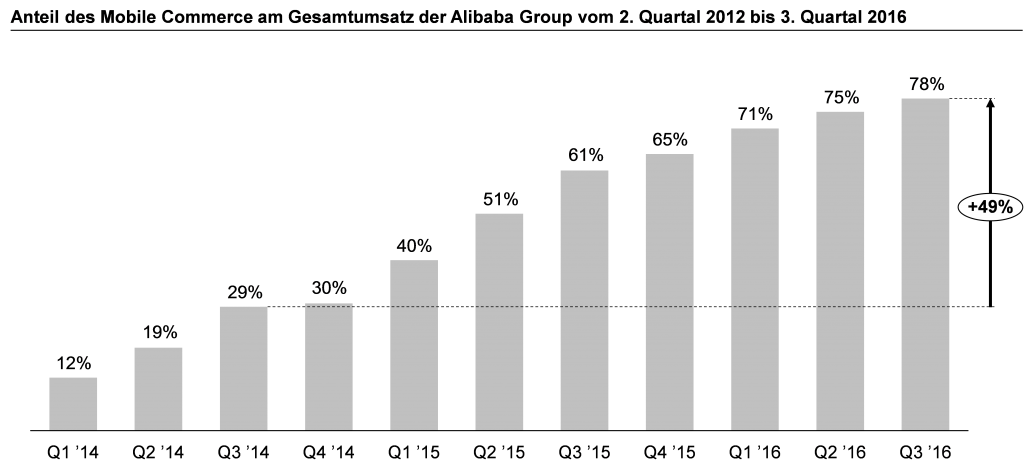

This effect is accentuated by the growing importance of mobile online retail for the parent Alibaba Group. In the third quarter of 2016, 78% of its aggregate turnover was generated through mobile commerce.

Figure 1 – Mobile commerce as a percentage of Alibaba Group’s total Revenue, from Q2 2012 to Q3 2016

It is therefore recommended to give full weight to AliPay when assessing risks and competition, alongside Apple Pay, Android Pay and Samsung Pay, and also to evaluate AliPay’s strengths when developing in-house bank-based payment solutions.

SOURCES

Internet

https://www.wirecard.de/AliPay

https://www.concardis.com/at-de/artikel/partnerschaft-mit-AliPay

Meet our authors

Expert En - Artur Burgardt

Artur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment ...

Read moreArtur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment and banking products, modern technologies / technical standards, architecture conceptualisation and their use in complex heterogeneous system environments.

Read less