Libra against the rest of the world

FINMA TAKES A STANCE ON LIBRA, WHILE STATE STABLE COIN IN CHINA IS ABOUT TO GO LIVE

Key facts

- FINMA specifies the regulation of stable coins, formulates high requirements and also takes a position on Libra

- Statements raise doubts about the short-term launch of Libra in the first half of 2020, especially as other national regulators (e.g. Germany and France) explicitly position themselves against Libra and, according to reports, first members of the association are starting to question their support for the initiative

- Parallel to this, the chinese stable coin developed by the chinese state-initiated DC/EP (Digital Currency/Electronic Payments) project, remains largely unnoticed by the media in Europe and the USA

- Threat of the international central banking system being undermined is not perceived acutely with regards to DC/EP. However, the project still remains controversial due to potential for political abuse

- The capital markets and regulators are lacking an answer of their own to the supply shortfall of efficient and scalable digital currencies, that currently is addressed by Libra and DC/EP

Background

The Libra Association, which was founded 2019 in Geneva, says that its domiciliation falls within the regulatory scope of the Swiss Financial Market Supervisory Authority FINMA, although an official regulatory classification remained open until recently. On September 11th 2019, FINMA published a position paper on the proposed regulation of so called stable coins, i.e. crypto currencies, whose exchange rate against fiat currencies is hedged with corresponding assets (currencies, commodities, ...) – for Libra this is covered by a stable currency basket. In this context, FINMA also confirms the request of the Geneva-based Libra Association for a regulatory assessment of the Libra project.

FINMA points out that financial market regulation in Switzerland is principle-based and strictly technology-neutral, and explains that in Switzerland such a project would most likely be regarded as an infrastructure and - due to Facebook's considerable reach - systemically relevant right from the start. This in turn would mean that a financial market law approval by FINMA would become necessary as a payment system on the basis of the Swiss Financial Market Infrastructure Act (FinfraG). In terms of combating money laundering, this implies the need to ensure the highest international standards throughout the project's ecosystem, so that the project as a whole is immune to increased money laundering risks. Furthermore, FINMA also clarifies that the planned services of the Libra project go beyond those of a pure payment system and that therefore bank-like regulatory practices must be implemented. These would concern in particular the distribution of capital, liquidity and risk (for credit, market and operational risks), as well as the requirements for managing the reserve.

As a result of this assessment, a basic prerequisite for the approval of Libra would also be that the income and risks associated with the management of the reserve would be borne entirely by the Libra Association and not - as is the case, for example, with a fund provider - by any owners of the stable coin.

FINMA also states that the planned international scope of the project will make it necessary to define the requirements for managing the reserve, corporate governance and combating money laundering internationally. Finally, it is emphasised that the comments are merely an initial indicative classification, as no concrete licence application has yet been received.

Is the Libra timeline still realistic?

According to the white paper, Libra was originally scheduled to be launched in the first half of 2020.

This timeline was revised as early as July 2019, when David Marcus, Facebook's Libra officer, was heard in a hearing at the US Senate Banking Committee: Marcus stressed that the launch of Libra would require the approval of all relevant authorities and thus responded to the previously increasingly negative reactions of politicians, banks and regulators (see Global, digital currency - utopia, dystopia or liberation?). Marcus stated that FINMA was the primary regulatory body responsible for this matter and said: "We had preliminary discussions with FINMA and assume that we will work with it to develop a suitable regulatory framework for the Libra allocation”.

FINMA's statement and in particular its explicit categorisation as an "indicative classification" on the basis of a pending licence application suggest that regulatory analysis and approval of Libra is far less advanced than David Marcus suggested in July 2019. However, in an interview with the Frankfurter Allgemeine Zeitung on 28 September 2019, Bertrand Perez, Director of the Libra Association, announced that they "had applied to the Swiss Financial Supervisory Authority Finma for a licence as a payment service provider". In this respect, all questions about the design of Libra in the near future will be addessed by a well-founded supervisory answer. aAlthough in the same interview, Perez spoke of a planned launch in the second half of 2020, which would already postpone the initial timeline from the Libra white paper by half a year.

That this revised plan still seems ambitious, becomes conclusive when one takes a closer look at the minimum regulatory criteria cited by FINMA: The reference to analogous claims against banks with regard to KYC and AML processes means a considerable hurdle in exactly the area for which Libra leaves concrete answers open in its white paper (cf. Blogpost Global, digital currency - utopia, dystopia or liberation?) and thus allows the interpretation of wanting to outsource this responsibility to possible wallet providers - in compliance with the requirements of the respective jurisdiction. However, this logic would be negated by the FINMA guidelines.

The international coordination of AML requirements and processes postulated by FINMA as a necessary precondition is likely to place a further burden on the ambitious timeline, and the fact that even large and established financial institutions have repeatedly complained about unrealistic AML requirements in the recent past testifies to the multiplying complexity of this task in operations.

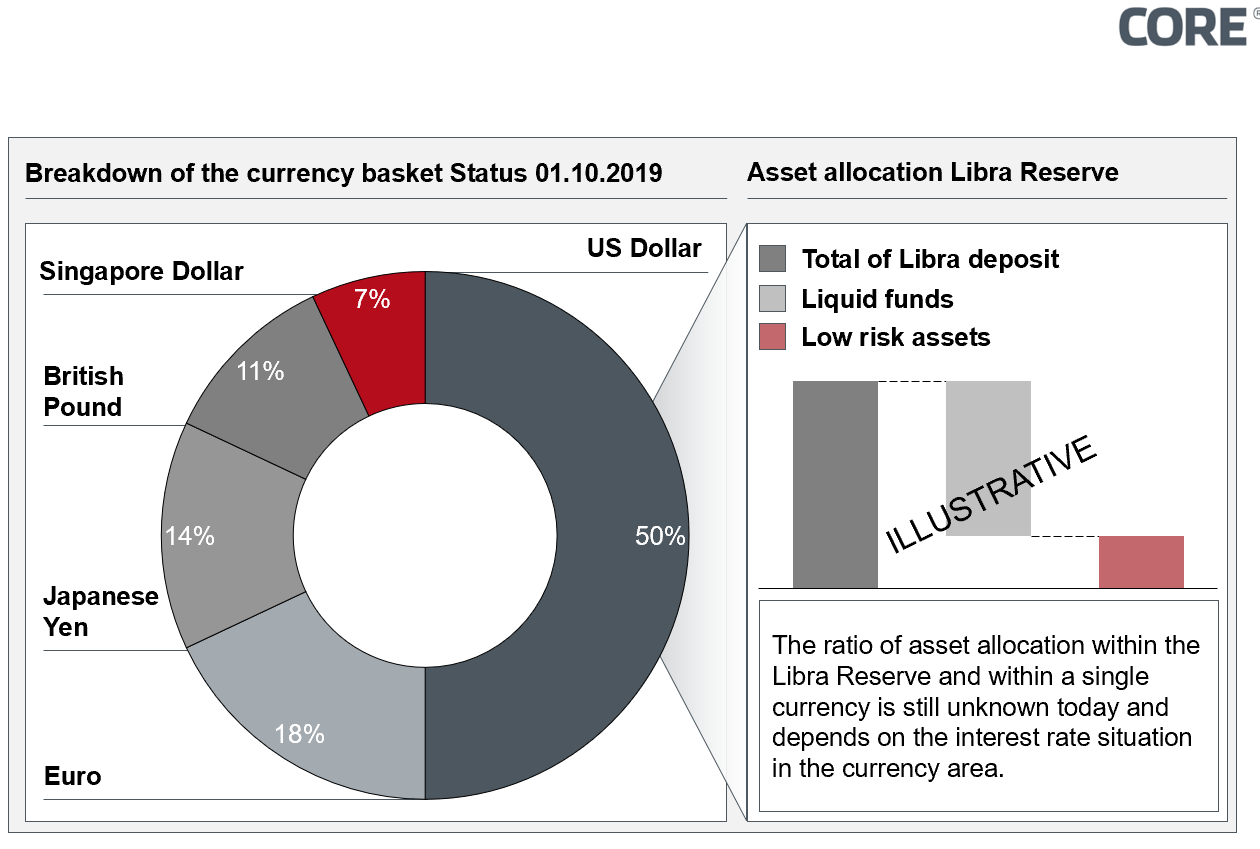

Figure 1: Libra Reserve - Breakdown of currency basket and asset allocation

Figure 1: Libra Reserve - Breakdown of currency basket and asset allocation

Furthermore, FINMA's requirement that the capital risks resulting from the Libra Reserve be borne by the Association and not passed on to the holders of the Libra Coins implies potentially elementary effects on the ecosystem: The Libra concept envisages investing part of the reserve in "high-yielding but low-risk investment opportunities, such as short-term government bonds issued by stable governments", with the capital income from the allocation being due to cover its costs and, if applicable, to the founding members as a "dividend". On 23.09.2019 the Libra Association officially announced how the distribution of the reserve is to take place. At 50%, the US Dollar represents the highest share of the reserve. This is followed by the Euro with 18%, the Japanese Yen with 14%, the British Pound with 11% and finally 7% of the Singapore Dollar (Figure 1) It is striking that the Chinese Renminbi is not supposed to be part of the reserve. Libra does not provide an official justification for this. It is quite likely, however, that this is a reaction to the public and political pressure. Most recently, for example, the democratic senator Mark Warner spoke out against the inclusion of the renminbi in the Libra ecosystem.

However, the currency shares mentioned, do not only represent cash reserves, but also include "short-term, low-risk government bonds", whereby Libra has not yet made any concrete statements on the bond type, relative distribution and maturity of these very bonds.

If, despite a low-risk investment strategy, individual investments were to become deficit-intensive or even defaulted (e.g. due to a national bankruptcy of a bond issuer), the resulting loss in value of the reserve due to the hard coupling of the stable-coin libra to the reserve would mean a proportional loss in value of the coins. Since FINMA stipulates that this must not be passed on to users, any losses would have to be levelled out by the libra allocation against the reserve. How often and to what extent these events occur depends to a large extent on the investment strategy and at the same time influences the possible return targets. The fact that Libra's vision of using the capital gains from the reserve as a primary source of money for operations, further development and possibly even distribution of dividends to its members was already regarded as ambitious, this is further reinforced by the form of risk allocation demanded by FINMA.

In parallel with FINMA's comments, a second strand of action is developing, which makes a short-term introduction of Libra appear unlikely: After the American regulators and even Donald Trump expressed reservations about the project shortly after the publication of the Libra White Paper, there is now explicit resistance in Europe as well: On September 13 Germany's Federal Minister of Finance Olaf Scholz expressed his views:

"The issue of a currency does not belong in the hands of a private company, because it is a core element of state sovereignty. The euro is and remains the only legal tender in the euro area."

In doing so, the German government joins the recently published opinion of France's Finance Minister Bruno Le Maire, who wants to "slow down the plans of the Internet giant Facebook for the digital currency Libra". The negative attitude of the Federal Government is also formalised in the blockchain strategy of the German Federal Ministry of Finance published shortly afterwards on 18.09.2019: Embedded in a multi-layered plan of measures to develop the application potential of blockchain technology in the German and European financial industry (e.g. for securities trading), it is stated that the German government intends to work on a European and international level to ensure that stable coins such as Libra will not substitute state currencies. Diametrically, however, it is stated that "the dialogue with the German federal bank on digital central bank money is to be expanded" and "the state of development is to be sounded out". This fits in with the CDU partys call for a "digital euro" published shortly after the publication of the Libra White Paper, although the anticipated responsibility for implementation by the European Central Bank or the national central banks still seems unclear.

According to information from the financial service Bloomberg, the critical positioning of numerous regulators also explains that the card schemes Visa and Mastercard, as well as the payment service providers PayPal and Stripe, are currently questioning their membership in the Libra Association, although no official statement has yet been issued by the companies in question.

Notwithstanding the aforementioned resistance, the discussion with the national regulators of Libra will continue to be actively shaped - as recently at the meeting of 26 central bank representatives in Basel on 24.09.2019, where David Marcus stated about Libra that "The Libra Network should be made generally accessible according to the initially planned timeline, while on a country basis the availability and number of wallets will be ambivalent. However, the Calibra Wallet will only be available in countries where it can be offered in accordance with local legislation“.

Meanwhile in China

While resistance against Libra and support for a European response is growing in Europe, China has already taken a considerable step forward: since 2014 a research group of the Chinese central bank has been working on the introduction of a Chinese digital currency as part of the DC/EP (Digital Currency/Electronic Payments) project on behalf of the Chinese government.

Background and objectives of the DC/EP coin

The officially proclaimed goals of the DC/EP coin are 1. to reduce the costs of traditional paper money, 2. to sharpen the instruments against AML, tax evasion and fraud, and 3. to strengthen the (direct) control of the liquid money supply by politicians. As with Libra, it is supposed to be a stable coin, but in this case its value is exclusively linked to the Renminbi. Similar to Libra, the crypto currency should also be usable without the need for a bank account. DC/EP coins should be available in dedicated wallets, but can also be used with the Messenger WeChat, which is very widespread in China, or via the payment service provider Alipay. Furthermore, it is stated that no Internet connection is necessary for a transaction, which means that the DC/EP coin can also be used in crisis situations - such as a power failure after natural disasters.

Status of implementation

According to Mu Changchun, Deputy Director of the Payment Settlement Department of the Central Bank of China, the DC/EP coin is nearing completion and could be introduced soon. According to the Reuters news agency, the pilot is already scheduled for Q4 2019.

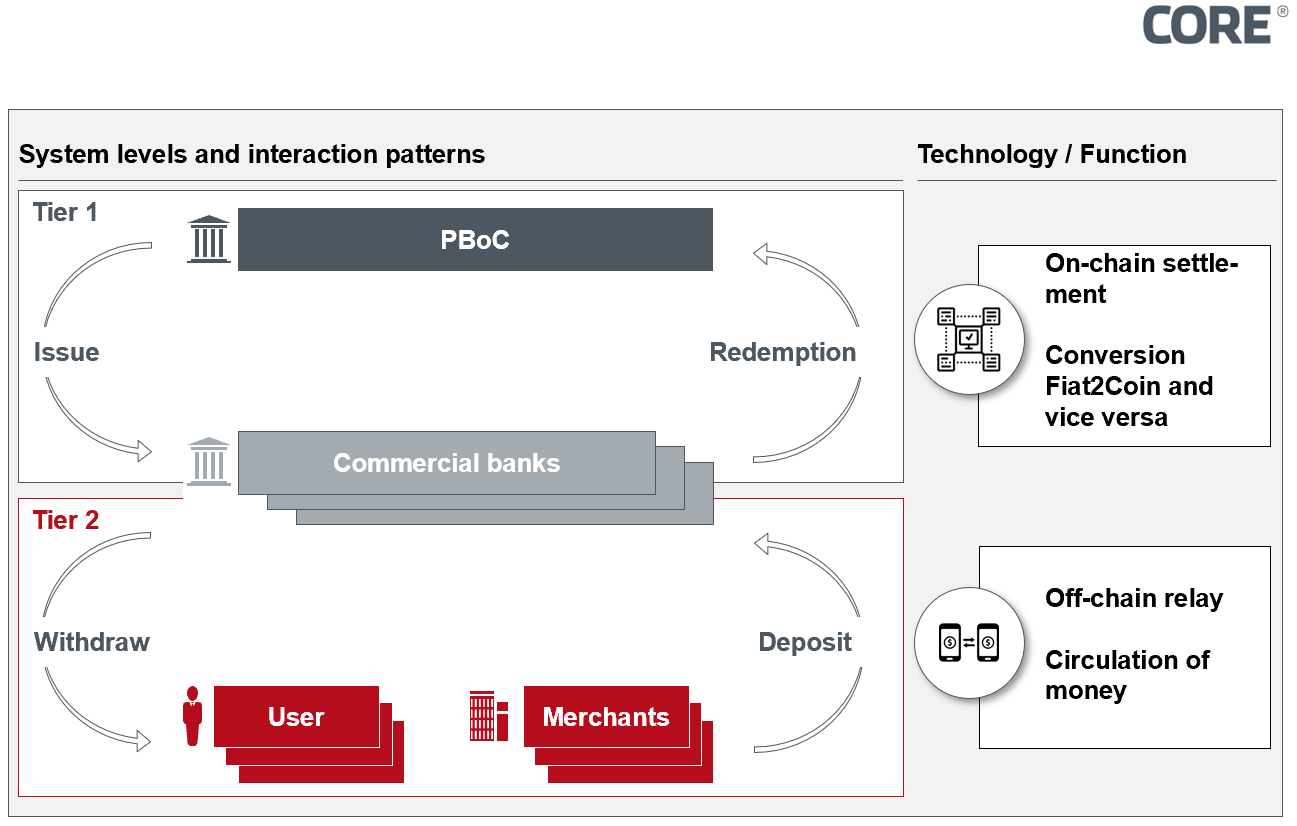

The DC/EP coin is to be implemented as a two-tier system. The first layer (Tier 1) is the Chinese central bank, which generates the coins via a block chain and distributes them to commercial banks in China. Commercial banks act as so-called "conversion agents" and distribute the coins7 to other market participants in the second layer (Tier 2), whereby no further details are known from the official side with regard to the technological approach and consequently different options are discussed: Since Tier 2 is estimated to have a utilization rate of approximately 300,000 transactions per second and no known blockchain has reached this cadence, the DC/EP project is either working on an innovative, high performance blockchain, or - more likely - no blockchain will be used in Tier 2. The latter variant would explain the independence from an available network connection and is also supported by statements of the deputy director of the Digital Money Research Institute of the Chinese Central Bank, Di Gong: Gong mentioned several times publicly that the idea of a digital currency does not necessarily imply the use of a blockchain. The combination of blockchain and offline capability could be explained, for example, by an "off-chain relay, on-chain settlement" setup, in which transactions are validated offline via a cryptographically secured mechanism and cleared and settled online downstream - e.g. when a network connection is next available (Figure 2).

Figure 2: Possible technical design of the two-tier setup of the DC/EP coin

Figure 2: Possible technical design of the two-tier setup of the DC/EP coin

Furthermore, the statements that DC/EP should make double-spent and coin forgeries cryptohraphically impossible by design, as well as the stated use of Secure Elements on the end-devices of the users, suggest that the transaction processing is token-based.

In view of the associated data protection implications, Yao Qian, former head of the Digital Currency Research Department of the Chinese Central Bank, characterizes the term "controlled anonymity" of the DC/EP coin, which is to be based on the principle of "voluntary anonymity in the frontend as well as the real name in the backend". As a result, following the introduction of the DC/EP coin, the Chinese state has a holistic transaction view that can be traced back to the individual payment participant and can thus also track the movements of DC/EP coins abroad. Based on this data, machine learning algorithms should be able to better predict the multi-variable environment of macroeconomics and thus derive advantages for steering the Chinese economy.

Evaluation of the DC/EP project

The fact that little concrete information on the technical approach is yet publicly known can be interpreted in different ways: On the one hand, the Chinese government could deliberately withhold detailed information in order, for example, to safeguard the envisaged competitive advantages resulting from a state digital currency against copy by other nations. On the other hand, the state of implementation could simply be less advanced than publicly suggested, so that the communications of a forthcoming market launch could rather be a reaction to the discussions about Libra.

In addition, the goals, motivation and implementation approach of the DC/EP coin can also be critically questioned: The relative share of cash in circulation in China has declined steadily in recent years. One reason for this is that the share of private e-money wallets - especially Alipay and WeChat with a combined market share of over 90% - accounts for a considerable proportion of the payment traffic volume and amounted to cumulated 277 trillion RMB in 2018, which was about 38 times the amount of circulating cash in China. The fact that money that once flowed into the wallets of Alipay and WeChat tends not to leave these ecosystems again due to the high acceptance range and, in some cases, the applied disbursement fees, means for commercial banks and central banks a strong reduction of the sphere of influence - especially since Alipay and WeChat are not banks and are therefore more difficult for the Chinese central bank to grasp from a regulatory point of view. The increasing expansion of the market reach of Alipay and WeChat beyond China further reinforces this limitation from the perspective of the Chinese central bank. The concept of the DC/EP coin could initiate a counter-movement and return the claimed direct sphere of influence to both the commercial banks as "conversion agents" and the central bank as the technical and organisational core of the ecosystem. The motivation of the DC/EP project is therefore probably not just a monetary policy departure or a short-term reaction to Libra, but rather the logical continuation of a phenomenon that has been observable in China for years now, namely the steady reduction of the money supply M0 (simplified: cash in circulation).

The fact that the DC/EP coin is also to be integrated into the wallets of Alipay and WeChat is by no means to be interpreted as a contradiction here: The wallet providers would become distributors of the DC/EP coin technically controlled by the central bank and could thus positively influence the market adaptation, while at the same time the central bank - in contrast to the current situation - would gain control over cash flows and user data and could thus limit the information advantage of the firms and opens up for itself the possibility to limit indirectly also the sphere of influence of Alipay and WeChat.

However, the full sovereignty of the state over the DC/EP project can also be interpreted as a significant political risk: For example, the usability of the DC/EP coin could be centrally orchestrated for limitation to selected recipients by technical means. On the premise of a sufficiently high market penetration, the DC/EP coin could thus be used as an effective measure of foreclosing the market from foreign economic entities. Especially in times of the trade conflict with the USA, this could be a possible instrument to influence the trade balance, e.g. by technically forcing the boycotting of American products and services. Furthermore, the DC/EP coin potentially provides the Chinese central bank and ultimately the government with full transparency over all transactions settled with it. Particularly under the scenario of a far-reaching substitution of cash envisaged by the central bank, this power could be used as a tool of economic and political control of the Chinese population - additionally strengthened by integration into the ecosystems of WeChat and Alipay. Since China is increasingly becoming one of the most important sales markets for western companies as well, the Chinese government would have a powerful instrument at its disposal with the DC/EP coin.

Discourse on Libra and DC/EP coin in comparison

Both initiatives, Libra and DC/EP, postulate the necessity of a payment ecosystem that is adequate, efficient and scalable to today's technological potentials and address precisely this supply gap. Although, the official motivation is largely congruent, the market environments, the implementation approaches and the subsequent reactions are fundamentally divergent:

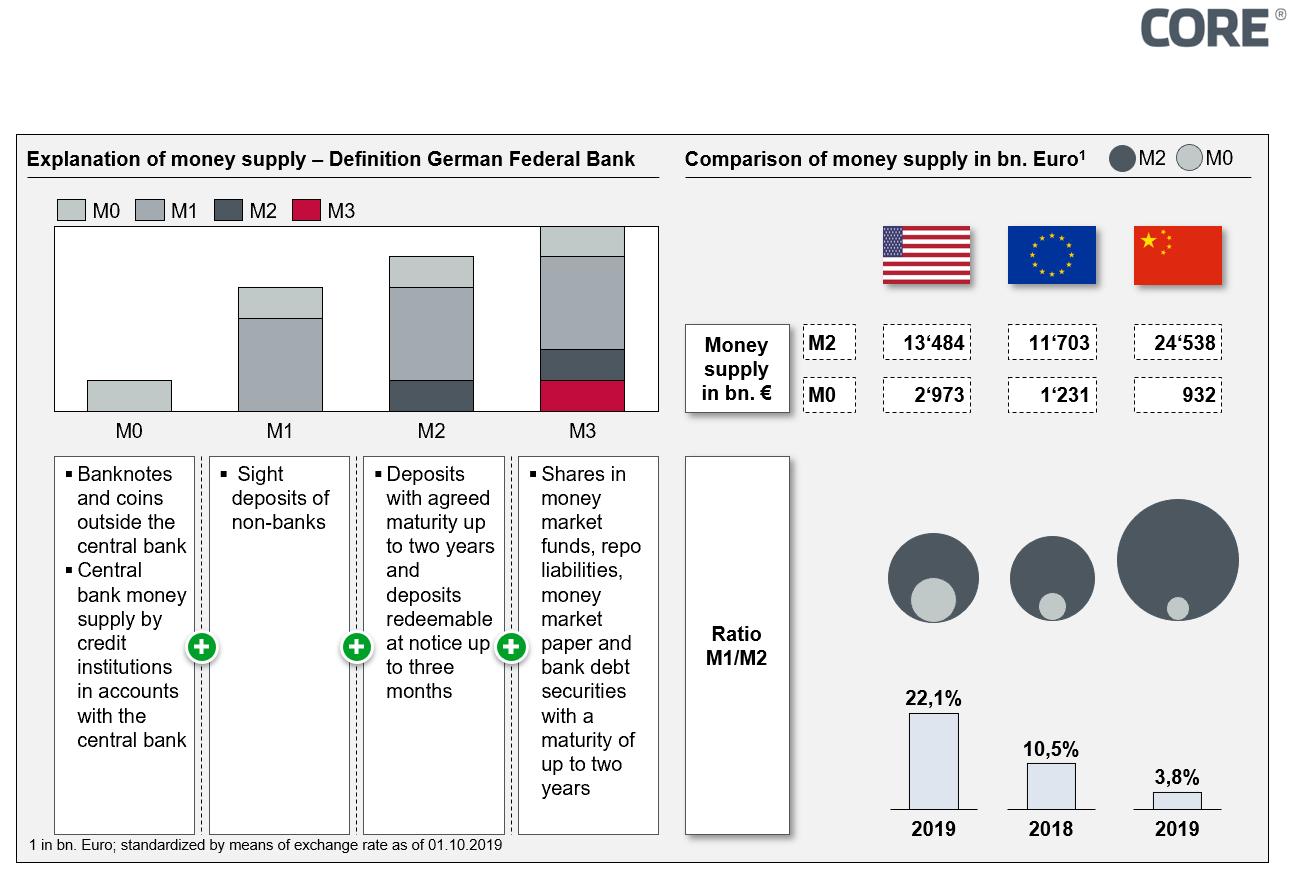

With regard to the use of cash, the target markets of Libra and the DC/EP project differs funda-mentally. This can be illustrated by the share of cash circulation in the money supply M2. The definition of M2 varies slightly depending on the defining institution but generally refers to the sum of M1 (Cash in circulation plus overnight depositis) and short term saving deposits e.g. deposits with an agreed maturity up to 2 years and deposits redeemable at a period of notice up to 3 months. As shown in Figure 3, this percentage for China is just under 4% which is around 2.5 times lower than in Europe and the USA.

Figure 3: Comparison between the relative share of cash in circulation in M2 in the USA, the eurozone and China

Figure 3: Comparison between the relative share of cash in circulation in M2 in the USA, the eurozone and China

It can thus be stated that the amount of cash used in the Chinese economy is remarkably low. The motivation of the DC/EP project is therefore probably not just a monetary policy departure or a short-term reaction to Libra, but rather the logical continuation of a phenomenon that has been observable in China for years now, namely the steady reduction of the cash in circulation. According to Libra, on the other hand, it focuses on use cases that are not currently depicted with cash, such as international payments.

While the realization approach of Libra is a private and supranational initiative to issue a new currency that is detached from state monetary policy and which is primarily a global payment ecosystem, the DC/EP project focuses on the electrification of an existing Fiat currency (here: Renminbi). As the initiator of the DC/EP coin, the Chinese central bank emphasizes that the project focuses on the home country and that the state DC/EP coin could achieve higher value stability than the private sector initiative, Libra. However, this interpretation can be contradicted by the fact that the value stability of the DC/EP coin actually depends only on the Renminbi exchange rate, whereas the value stability of the libra is pegged to a basket of different fiat currencies and short-term government bonds - i.e. the Libra reserve has a higher risk diversification.

However, the biggest discrepancy between Libra and DC/EP lies in their perceived impact on the existing monetary and financial systems, which also explains the widely differing discourses in scope and emotionality:

In the case of Libra, from the point of view of existing persons in charge, there is a risk that the state's currency sovereignty will be undermined and that central bank technical or political influence on interest rates and money supply will be limited in order to control economic strength. These concerns also explain the media presence and increasing resistance in the USA and Europe. It is therefore not surprising that Libra is vehemently trying to refute the concerns and accusations that have been raised and is partly presenting itself as a victim of one-sided reporting.

Similar concerns are not anticipated in relation to DC/EP, as the central bank concerned is itself the initiator of the project. On the contrary, the associated potential could further expand the economic and political influence of the Chinese central bank and thus also of the Chinese government while enabling the potential for state abuse.

In summary, both Libra and DC/EP have well-founded concerns. However, both initiatives should be appreciated for their attempt to formulate an answer to the obvious market demand for a value-stable and sufficiently accepted digital currency, which has not yet been answered. While in Europe protectionism and reservations dominate the discourse and a European response beyond a non-binding target module in the national blockchain strategy of the German Federal Government is not (yet) discernible.

Bottom line

FINMA's comments, the latest statements by European governments and rumours of the withdrawal of some members of the Libra Association make the short-term introduction of Libra unlikely. The arguments put forward against Libra are divided into operational concerns (e.g. lack of information with regards to the envisaged KYC and AML processes) and fundamental reservations about supranational or private currencies (leveraging the control functions of central banks as market risk). Due to the initiation and control by the Chinese government as well as the national limitation of the DC/EP project, the latter argument only has a limited impact there and thus also explains the comparatively low media presence and reflection of the project in Europe.

The concentration of the European discourse on Libra does not do justice to the complex situation: the fact that the sovereignty and control function of DC/EP remain with the Chinese central bank and thus in the hands of the state by no means prevents economic interactions with the rest of the world, but rather opens up possibilities for the political exploitation of the digital currency. A political attention to DC/EP in the USA and Europe that is equivalent to that of Libra therefore seems appropriate.

Whether Libra, DC/EP, Euro-Coin or other initiatives currently observable in the market: The current debates are characterized by the position "digital currency is new territory". This is because the still young field of research into digital currencies must first form a common area of experience from which the framework for possible digital currencies can develop. In particular, the undeniable potential of digital currencies such as cost efficiencies, higher transaction speeds, accessibility by "non/under-banked people" and the prevention of criminal activities (money laundering, terrorist financing, tax evasion, etc.) are not yet sufficiently reflected in the current debates. Consequently, politicians, regulators and banks should seek a global and unbiased discussion to avoid a crypto arms race as well as protectionism against innovation.

Sources

- Testimony of David Marcus

https://www.banking.senate.gov/imo/media/doc/Marcus%20Testimony%207-16-19.pdf

- FAZ vom 28. September 2019

- Facebook adds singapore dollar to libra crypto basket

https://www.coindesk.com/facebook-adds-singapore-dollar-to-libra-crypto-basket

- Visa und MasterCard überdenken Libra-Beteiligung

https://www.spiegel.de/wirtschaft/unternehmen/facebook-kryptowaehrung-libra-visa-und-mastercard-sollen-nach-kritik-zoegern-a-1289636.html

- Interview: David Marcus über Libra: «Wenn wir den Zahlungsverkehr nicht revolutionieren, machen es andere»

https://www.nzz.ch/finanzen/wenn-wir-den-zahlungsverkehr-nicht-revolutionieren-machen-es-andere-ld.1509960?fbclid=IwAR15IeGDQ3Elfr8DMTtyE7yCnsObrfbGrsCs5c4D0aBjiahLMED9RuqbKSk

- Chinas digital currency will be two tiered replace cash binance

https://www.coindesk.com/chinas-digital-currency-will-be-two-tiered-replace-cash-binance

- China’s proposed digital currency will help banks bridge gap on mobile payment, curb dominance of Alipay, WeChat

https://www.scmp.com/print/business/banking-finance/article/3023309/chinas-proposed-digital-currency-will-help-banks-bridge

7 things you probably didn’t know about China’s digital currency – Global Coin Research

https://www.theblockcrypto.com/post/37782/7-things-you-probably-didnt-know-about-chinas-digital-currency-global-coin-research

- Chinas digital currency will be two tiered replace cash binance

https://www.coindesk.com/chinas-digital-currency-will-be-two-tiered-replace-cash-binance

- Interview: David Marcus über Libra: «Wenn wir den Zahlungsverkehr nicht revolutionieren, machen es andere»

https://www.nzz.ch/finanzen/wenn-wir-den-zahlungsverkehr-nicht-revolutionieren-machen-es-andere-ld.1509960

- Interview: David Marcus über Libra: «Wenn wir den Zahlungsverkehr nicht revolutionieren, machen es andere»

https://www.nzz.ch/finanzen/wenn-wir-den-zahlungsverkehr-nicht-revolutionieren-machen-es-andere-ld.1509960

- https://www.ft.com/content/746808a0-d9f6-11e9-8f9b-77216ebe1f17

China’s digital currency similar to the Uruguay e-peso pilot

https://www.emmanueldaniel.com/chinas-digital-currency-copies-the-uruguay-e-peso-pilot/

China Is Almost Ready to Roll Out Official Digital Currency, PBOC Official Says

https://www.yicaiglobal.com/news/china-is-almost-ready-to-roll-out-official-digital-currency-pboc-official-says

State-Issued Digital Currencies: The Countries Which Adopted, Rejected or Researched the Concept

https://cointelegraph.com/news/state-issued-digital-currencies-the-countries-which-adopted-rejected-or-researched-the-concept

- FINMA Positionspapier

https://finma.ch/de/news/2019/09/20190911-mm-stable-coins/

- Banken mit Geldwäscheanforderungen überfordert

https://www.faz.net/aktuell/wirtschaft/diginomics/it-deutsche-bank-muss-von-hand-auf-geldwaesche-pruefen-15721612.html

- Libra bekommt Konkurrenz aus China

https://www.golem.de/news/libra-facebooks-digitalwaehrung-bekommt-konkurrenz-aus-china-1909-143747.html

- China’s Central Bank Prioritizes Development of Digital Currency

https://cointelegraph.com/news/chinas-central-bank-prioritizes-development-of-digital-currency

- First Look: China's Central Bank Digital Currency

https://info.binance.com/en/research/marketresearch/DC/EP.html

- Bundesregierung stellt sich gegen Libra

https://www.faz.net/aktuell/finanzen/bundesregierung-stellt-sich-gegen-facebook-waehrung-libra-16383516.html

- Mit dem „digitalen Euro“ will die CDU das Facebook-Geld abwehren

https://www.welt.de/finanzen/article195909017/Kryptowaehrung-CDU-will-mit-digitalem-Euro-Facebooks-Libra-abwehren.html

- Chinas digital currency is being built in a secret office with restricted access

https://www.coindesk.com/chinas-digital-currency-is-being-built-in-a-secret-office-with-restricted-access

- Chinas Digitalwährung – Was steckt hinter den Plänen?

https://de.cointelegraph.com/news/digital-yuan-weapon-in-us-trade-war-or-attempt-to-manipulate-bitcoin

- Facebook wehrt sich gegen politische Bedenken

https://www.finanzen.net/nachricht/devisen/abgesicherter-coin-facebook-wehrt-sich-gegen-politische-bedenken-zu-digitalwaehrung-libra-7997810

- First Look: China's Central Bank Digital Currency

https://info.binance.com/en/research/marketresearch/DC/EP.html

- A systematic framework to understand central bank digital currencyhttps://link.springer.com/article/10.1007%2Fs11432-017-9294-5