By Launching a Virtual Credit Card, Cornèrcard Carves Out a Path to Market for Apple Pay

KEY FACTS

-

Market entry of Apple Pay in Switzerland, without market leaders UBS and Credit Suisse

-

Cornèr launches Cornèrcard Instant – a purely virtual prepaid credit card that is straightforward to apply for and can be issued immediately – especially for Apple Pay

-

The launch of a purely digital credit card for Apple Pay taps into huge potential of acquiring new customers and consumers switching card providers

REPORT

Less than a month after the announcement at the Apple Worldwide Developer Conference (WWDC), Apple Pay went live on the Swiss market on July 7, 2016. Up until then, there had been no sign of the revolution at Swiss NFC terminals predicted by Apple, which was mainly due to the fact that only three card issuers – Cornèr Bank, Swiss Bankers, and Bonuscard – support Apple Pay. Major players such as Credit Suisse, PostFinance, Raiffeisen, UBS and ZKB – who, between them, account for the majority of the Swiss payment card market – are not currently taking part in the Apple Pay program.

Cornèr’s launch of the Cornèrcard Instant on July 12, 2016 – five days after the go-live date – can, however, be interpreted as a subtle attack on the members of the TWINT network, as Cornèr is skilfully deploying Apple Pay as an instrument for acquiring new customers. This purely digital prepaid card specifically designed for use with Apple Pay claims it can be issued in a matter of minutes and was launched just a few days after the introduction of Apple Pay in Switzerland.

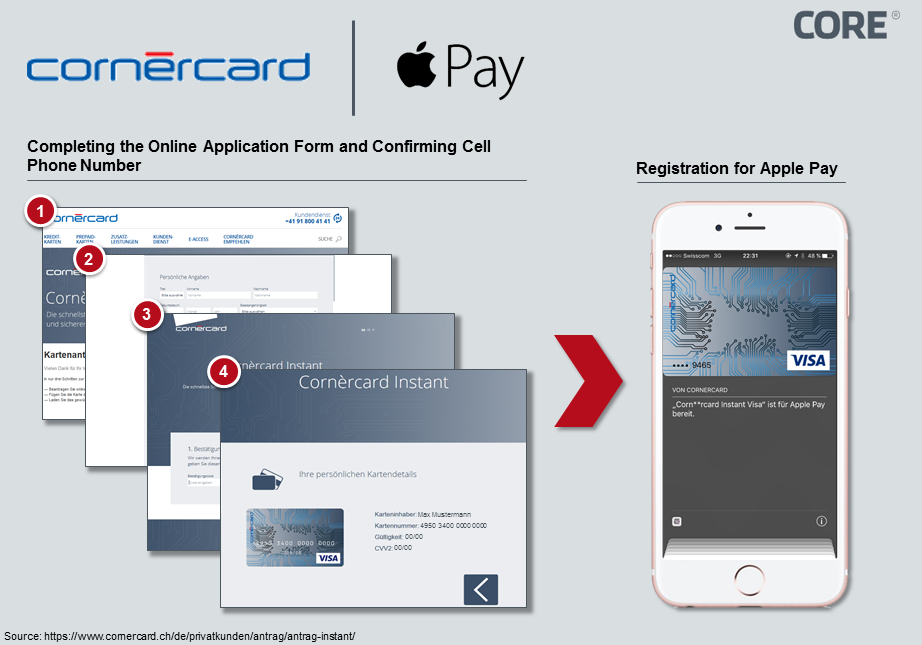

Customers can apply for the credit card by filling out a form online. Due to the nature of the card being prepaid, the form requires only personal details and a cell phone number, as, for instance, there is no need for a credit check. Once the customer has confirmed their cell phone number, using a one-time password sent by text message, their digital credit card is issued and ready to use immediately. Users can then activate the card and top up credit on their iPhone using the standard Apple Pay activation process.

By the nature of a straightforward process and low switching costs, the offer is aimed first and foremost at customers who would like to try out the technology but who do not hold a payment card from a participating bank. Due to the digital nature of the card, the customer is neither required – unlike with conventional credit cards – to be a Swiss citizen nor a resident in Switzerland, potentially expanding the reach of interest groups to tourists.

Figure 1: Simplification and for Apple Pay optimized application process for Cornèrcard Instant

The Cornèrcard Instant costs CHF 19 a year and is subject to an annual credit limit of CHF 2,500. A 3% fee of the top-up amount is also added. This means that the variable additional costs for the client are considerable, in contrast to conventional payment methods such as credit cards, which rules it out from being used permanently as a preferred means of payment. Instead, this innovative and immediate method of issuing a digital credit card is being successfully harnessed to target the maximum number of potential customers for Cornèr, with Apple Pay serving as the catalyst. Since there is no mobile payment solution in Switzerland with a comparable number of acceptance points until the launch of the new TWINT network, this temporary near-monopoly is being efficiently exploited.

As a result, this solution can be seen as a model approach for making the most of comparative competitive advantages generated by the market entry of technology providers. As demonstrated by the similar solution “boon by Wirecard” in the UK, banks not supporting new payment solutions are not necessarily an effective method of preventing customers from using them. Events in the UK and Switzerland will need to be closely monitored by decision-makers in the European credit card industry, who will also need to draw their own conclusions.

SOURCES

Cornèrcard, 2015

Ben Schwan, 13.07.2016