Instant payments – the challenges of “money in seconds” for banks

KEY FACTS

-

Instant payments announced, as a further innovation in pan-European payments, to promote free movement of capital in the European internal market

-

Payment transactions are to be processed within a few seconds, bringing major challenges for banks, especially in regards to IT

-

Various implementation options for instant payments under discussion

-

Final rules for SEPA Credit Transfer (SCT Inst) scheme published on 30 November, launch due in November 2017

-

Banks need to make use of additional potential of instant payments in combination with PSD II

REPORT

On 30 November of this year, the Euro Retail Payments Board (ERPB) released “Instant Payments Guidelines”, and more details are starting to emerge: banks and financial service providers will be required to implement instant payments in retail banking and operate them universally from November 2017. This requirement will create major challenges for many financial institutions. The legacy of their IT infrastructure (bringing “technical debt” in its train) means this requirement can only be met with high expenditure and lengthy lead-in times.

The European Central Bank (ECB) is the main driver of instant payments and set up the Euro Retail Payments Board (ERPB) for this purpose in December 2013. The ERPB is a strategic body within the ECB, with members drawn equally from financial service providers, end users, and representatives of national central banks. The aim of the ECB is to guarantee the innovation and competitiveness of the market for mass payments in the long term as well as promoting rapid pan-European movement of capital.

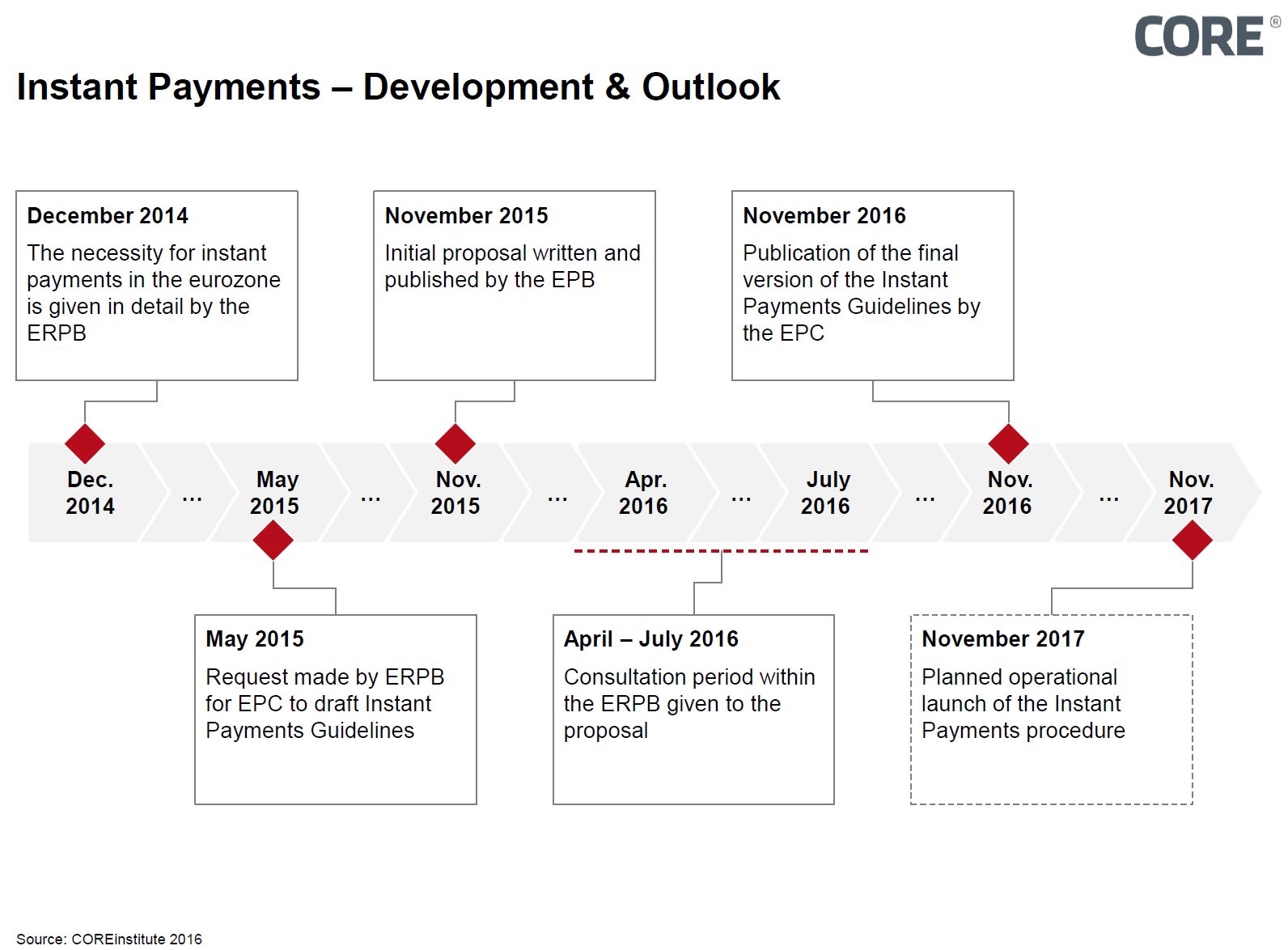

Figure 1: Development of Instant Payments

The SEPA format provides the basis for the continuing harmonization of payment transactions. Back on 1 December 2014, the ERPB recommended that an instant payments solution be set up that would be accessible Europe-wide for all payment service providers. The European Payments Council (EPC) produced a draft of rules for instant payments based on the SEPA standard (Instant SEPA Credit Transfer – SCTInst). In November 2015, the EPC submitted the document to the ERPB for approval. After a period of consultation, the guidelines were published on 30 November 2016 and are to be operationally implemented as from November 2017.

The term “Instant payments” refers to guaranteed year-round payment processing (7/24/365) where transactions are processed in a matter of seconds. Debiting the amount from the payer and crediting it to the payee are to occur simultaneously, and the recipient of the payment has access to the amount credited to them within a few seconds. The ECB stated a timeframe of up to ten seconds for the entire transaction to be completed. The transaction threshold is initially due to be set at 15,000 euros.

Numerous effects are expected as a result of implementing instant payments. On the consumer side, it is hoped that this change will bring about greater transparency in personal liquidity management, enable peer-to-peer payments without third-party involvement, and see the end of express payments. From the point of view of companies, potential benefits include the optimization of cashflow management, a reduced need for external capital, and a smaller risk pool.

The ability to undertake instant payments can be implemented in two very different ways, although no mandatory preference can be derived on the basis of the final SCTInstguidelines.

- According to a real-time model, instant payments are implemented end-to-end (“straight through processing”). The banks proceed directly from payments to clearing, meaning the settlement is also carried out immediately

- On the other hand, a guarantee model envisages banks providing each other with guarantees, also allowing them to issue the payment recipient with a guarantee. This would lead to a “near-instant” solution

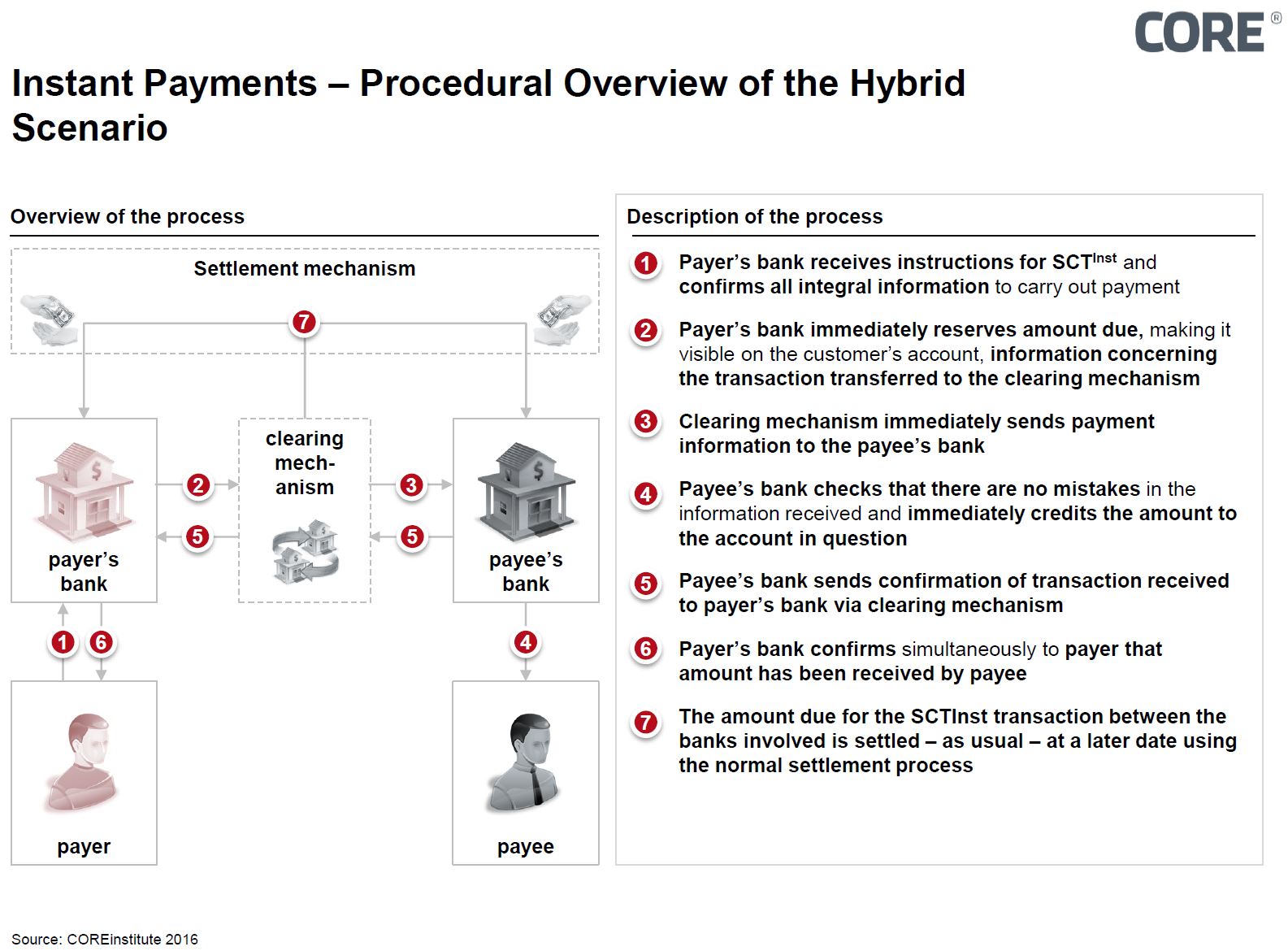

This hybrid solution means that sufficient liquidity must be in place, so-called “pre-funding” for the settlement. The complete instant payments process under the hybrid model can be presented in seven steps:

Figure 2: Process overview

As a result of the growing complexity of clearing processes resulting from the requirements for instant payments, adjustments need to be made to the system and process landscape of financial institutions. These modifications involve adapting key banking systems to enable instant debit and credit payments, as well as implementing an online gateway to process instant payments. The latter will require a direct link to the key banking system. Furthermore, GPS-generated systems such as “Know Your Customer” (KYC) and limit checks will need to be adjusted to take into account applicable compliance rules concerning the changed circumstances of instant payments. The main challenge for IT systems set up for batch processing will be to guarantee that systems are constantly available.

Financial institutions are currently very much preoccupied with implementing the requirements of PSD II. Few institutions have the resources to determine the potential of instant payments. This is all the more regrettable given that looking at PSD II and instant payments together seems likely to be highly advantageous. First, if instant payments were taken into account now, there would be no need to make individual adjustments for it later on. Secondly, it is only possible to tap into the business potential arising from the combination of these two aspects by considering them together. The ability to make a payment at any time with immediate knowledge of the transaction and availability of the money will soon be taken for granted just as SEPA payments are today. Given open access to information, this will also offer significant opportunities for innovation to third parties.

SOURCES

European Payments Council, 2016

EBA Clearing, 2016

Europäische Kommission, 2016

http://ec.europa.eu/finance/payments/framework/index_de.htm

VDB, 2016

https://www.vdb.de/Instant-Payments-Positionspapier-Juli-2016-V12.pdfx?forced=true&forced=true

Finextra, 2016

APCA, 2016

http://www.apca.com.au/about-payments/future-of-payments/new-payments-platform-phases-3-4

Meet our authors

Expert En - Artur Burgardt

Artur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment ...

Read moreArtur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment and banking products, modern technologies / technical standards, architecture conceptualisation and their use in complex heterogeneous system environments.

Read less