Le trio infernal - When a Card Scheme, a Tech Provider and a Bank join forces

KEY FACTS

- Apple, Mastercard and Goldman Sachs team up to launch Apple Card; this in the context of Apple´s transformation towards a service provider

- US customers receive a virtual credit card directly in the app, the card comes with an attractive loyalty program and appealing conditions, rounded up with a stylish physical metal card

- Involved partners create a strong, cohesive ecosystem - other issuers, Visa as well as hardware competitors, are pushed into a more passive role

- Adaptation of this set-up in Europe would be attractive for European issuers in the short term, however, lasting downsides of a cooperation with Apple remain valid in the long term, and a fundamental negation of the cooperation without alternatives entails the risk of a comparative competitive disadvantage

- The multidimensional answer to the question of cooperation must therefore be embedded in a holistic payment strategy

REPORT

Electrifying triangular relationship

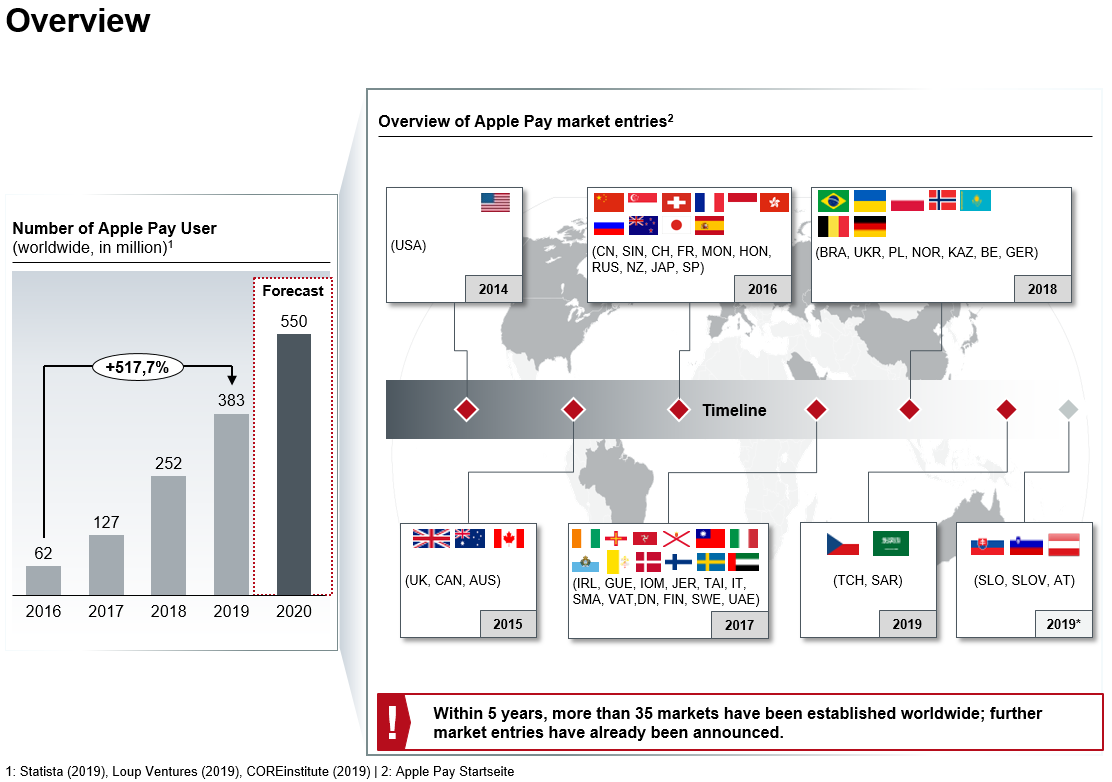

Since its introduction in the U.S. end of 2014, Apple Pay has recorded a moderate, but steady growth: According to its own figures, around 350 million users in 35 markets now use the card-based payment service from Cupertino - since end of 2018, Germany has also been one of these markets.

Figure 1: Number of Apple Pay users and overview of worldwide market entries

The incredible success story is put into another perspective once you consider that already more than one billion new iPhones have been sold since the introduction of Apple Pay and even older devices are able to support the solution as well. One of the underlying reasons is surely Apple's claim to receive a share of the card revenues from the issuing institutions (issuers) and various further obligations, such as guaranteed marketing budgets, strict SLAs or even exclusivity clauses. Issuers in the target markets therefore tend to react ambivalently, some even negatively, to the decision to introduce Apple Pay. An indication for this are the current proceedings by competition authorities in Switzerland and Australia.

Conversely, this also means that Apple Pay is required to look for solutions to maximize its coverage and reach, while at the same time making itself independent of the individual approval of issuers in each target market. A first approach was the cooperation of Apple Pay with the American Bank Green Dot in 2017 resulting in the new service Apple Pay Cash. The service offers a dedicated prepaid credit card, which is instantly issued in a lean process and thus typically reaches (but not only) customers whose house bank may not participate in Apple Pay yet. With Boon, Wirecard has already established a similar procedure in Germany prior to Apple Pay market launch.

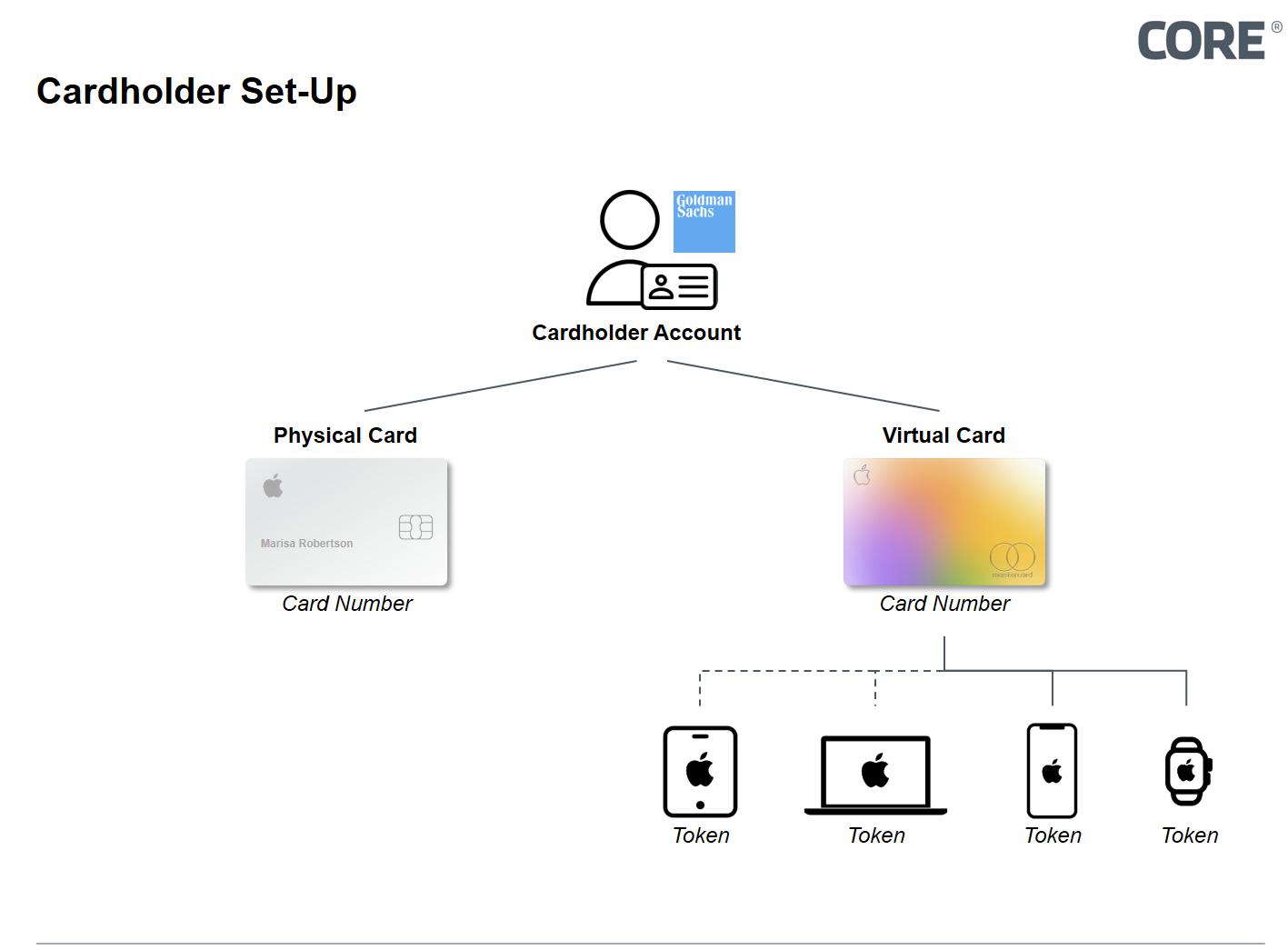

In Apple´s Keynote on March 25th 2019, the next step of these exploration efforts was announced. This initiative however involves, unlike the small players Wirecard or Green Dot Bank, two big players from the financial industry: Mastercard and Goldman Sachs. The Apple Card - a credit card optimized for Apple Pay - will be launched in the U.S. this summer. One can register for this card directly in the Apple Wallet, the card is then issued by Goldman Sachs and is accompanied by an attractive loyalty program.

With just a few taps on their smartphone, customers can apply for a virtual credit card from this renowned bank, which can subsequently even be supplemented by a physical card made of titanium at the customer's request. It is noteworthy that this card is exclusively designed for Apple Pay and comes extremely simplified without a visible card number, without a CVV/CVC security code and without even a signature. Furthermore, it does not even support NFC. Therefore, solely the physical card can be used for card-present transactions with a PIN at the POS. For all other usage cases, the virtual card within the Apple Wallet would have to be used.

The product is advertised as completely free of charge, interest rates vary between 13% and 24% p.a. for granted credit lines, depending on the creditworthiness of the customer (for comparison: the American APR average is ~16%). In the Apple Wallet, users can track, categorize and thus optimize their expenses in the sense of a financial assistant. On top of that, Apple offers up to 3% cashback on each card transaction with its in-house loyalty program Daily Cash, being directly credited to Apple Pay Cash and posing a significant threat to established loyalty programs.

For the three cooperating providers, this is a win-win-win setup: Goldman Sachs accompanies the current attempts to break into in the retail business with an enormous potential for new customers and benefits from card revenues (interchange and overdraft interest), Apple has - in line with the current transformation from hardware to service provider - a powerful instrument for customer loyalty, and Mastercard is transferring its business model into the digital world while realizing the usual scheme fees.

Figure 2: Cardholder Set-Up: Virtual Card linked to device-specific token

Liaison can become dangerous for other market participants

After Apple’s described cooperation with Green Dot and after the recently initiated cooperation between Mastercard and Paypal to issue a dedicated Google-Pay debit card in Germany, this Apple Card initiative is not surprising. Though, rather impressive is the service scope and the choice of the partner.

At second glance, the latter is a very coherent trio: In addition to the strong name, Goldman Sachs offered itself for an obvious reason, as unlike other (potential) Apple Card issuers, Goldman must not fear cannibalization or margin degression of existing products due to its weak retail business. Thus, the case can be almost completely understood as a "New Business". One might also wonder whether Apple will apply the usual transaction fees and known contractual clauses to its partner Goldman Sachs - even though it can currently only be assumed how the trio will share the revenues.

Mastercards’ involvement, on the other hand, goes far beyond the monetary perspective: Whilst in other markets card schemes like Mastercard mandate issuers to personalize the outdated and prone to fraud Track 1 on the magnetic stripe, in order to promote maximum POS acceptance, Mastercard offers Goldman an exclusive set-up of issuing a credit card without PAN, CVCs, a signature field, NFC and a magnetic stripe.

With its information services and loyalty program, this setup offers for the first time more than just transaction processing, but will nevertheless only be a further step in the same direction. To dare a look into the future, a look into the past can often be promising: About 9 months after Apple Pay was launched in the U.S., it became available in the United Kingdom. It then took another 3 years until Apple Pay was usable with cards of German issuers, such as Deutsche Bank or N26. Meanwhile, Apple Pay Cash has been available in the US since December 2017 and the first rumors about a launch in Great Britain are currently only emerging. When exactly Apple Card will reach further markets is therefore open, but the fact that Apple is also striving for an internationalization of the service, can be considered very likely.

In summary, the parties involved create a strong, mutually optimizing ecosystem - whilst other issuers, other schemes and other hardware competitors such as Samsung are sidelined to be observers. The case once more underlines how powerful and exclusive such ecosystems are, how much power payment schemes actually bear and how quickly banks can be degraded to infrastructure providers through cooperations with Apple & Co. Not even Goldman Sachs is immune to the latter in the medium term, as the issuer is probably the most exchangeable party in this setup. In the future, it would even be conceivable that Mastercard or Apple itself would become a card issuer - according to numerous reports, corresponding bank licenses were already issued.

CONCLUSION

This case clearly shows, that banks which follow established methods and accustomed business strategies are losing in the long run:

If a bank is currently considering to cooperate or is already participating with Apple Pay, an obvious deduction would be to become the European counterpart to Goldman Sachs in order to acquire new customers and expand market shares. Regardless of the fact that the solution for the European market would have to be adapted in some parts - for example, revolving credit cards such as Goldman's have empirically little acceptance among end customers in Europe - this tactic would have realistic chances of success in the short to medium term. In the long run, however, the corresponding issuer would quickly become sidelined by Apple and Mastercard, the most powerful partners in this setup, and would have to play by their rules or get replaced by the next more cooperative issuer.

A strategically farsighted bank, banking group or financial center should not blindly engage in this tactic and instead use its energy to decrease existing dependence on American payment schemes, potentially even with its own national or trans-European alternative (https://core.se/techmonitor/card-schemes). However, only relying on this path means quickly being overtaken by direct competitors participating in Apple Pay in the short term. The response to the delayed Apple Pay introduction of Barclays in Great Britain in 2015 or that of the Sparkassen in Germany currently show that customers and the media take little account of the strategic considerations of the respective institutes.

Banks should therefore analyse the aggravating situation and identify and assess the options for action for the respective institution, group and financial centre. Taking into account the current product portfolio, the customer base, the competitive environment and the regulatory requirements, a smart answer must be provided to the question whether to cooperate with Apple or not. This answer should however, definitely be embedded in a holistic long-term payment strategy.

Provided that the necessary expertise and resources are available, a two-pronged strategy can be promising for the moment. On one hand, the cooperation with Apple should be sought in order to meet customer needs directly, on the other hand, an overarching answer to the noticeably increasing challenges has to be found. In this complex situation for banks, this approach would not be the easiest to implement, but would give them the chance of further market participation in the medium and long term.

It should be recognised that this dilemma, which has been looming for more than five years, should no longer be ignored and that a short term answer should be developed, tailored to the individual institute.

SOURCES

- Figure 1: Number of Apple Pay users and overview of worldwide market entries

Statista (2019), Loup Ventures (2019) COREinstitute (2019) - Figure 2: Cardholder Set-Up: Virtual Card linked to device-specific token

medium.com/rivero-ag/top-10-questions-about-apple-card-9bf458649d03 - Website Apple

https://www.apple.com/apple-events/march-2019/ - Was die GAFAs in der Finanzbranche wirklich wollen

Hartmut Nielsen 26.11.2018 / Private Banking Magazin

https://www.private-banking-magazin.de/google-amazon-facebook-und-apple-was-die-gafas-in-der-finanzbranche-wirklich-wollen/ - Absatz von Apple iPhones weltweit in den Geschäftsjahren 2007 bis 2018 (in Millionen Stück)

Statista

https://de.statista.com/statistik/daten/studie/203584/umfrage/absatz-von-apple-iphones-seit-dem-geschaeftsjahr-2007/ - Barclays und die Einführung von Apple Pay – Handlungsmöglichkeiten der Banken

Volker Koppe / Annual Report Visa Europe

https://annualreport.visaeurope.com/de/uber-visa/presse-und-news/barclays-und-die-einfuhrung-von-apple-pay-handlungsmoeglichkeiten-der-banken-37962?returnUrl=/de/uber-visa/presse-und-news/listing?tag=visa - Apple Card Uncovered - Top 10 Q&A

Riverio AG 26.03.2019 / Medium Rivero

https://medium.com/rivero-ag/top-10-questions-about-apple-card-9bf458649d03 - Apple Pay Adoption Continues to Climb

Gene Munster, Will Thompson 19 Februar 2019 / Loupventures

https://loupventures.com/apple-pay-adoption-continues-to-climb/ - Average Credit Card Interest Rates (APR) - March, 2019

Federal Reserve G19 Report, Consumer Protection Bureau/ Valuepenguin https://www.valuepenguin.com/average-credit-card-interest-rate