Money via Email – Google and Square Enable Transactions by Email

KEY FACTS

-

Google and Square integrate the sending and receiving of money via email in the US

-

Increased convenience for customers

-

Providers aim to increase user numbers

-

Greater use of digital channels for peer-to-peer payments and transfers

-

Different demands in European and German markets

REPORT

Google only recently announced that it would enable users to send money via its email service, and now Square has announced a similar option with its service “Square Cash”. What is so interesting about transferring money and making payments via email? Of what use is this to customers, and to the providers? And what is the backstory behind this development in regard to the Payment Transactions segment?

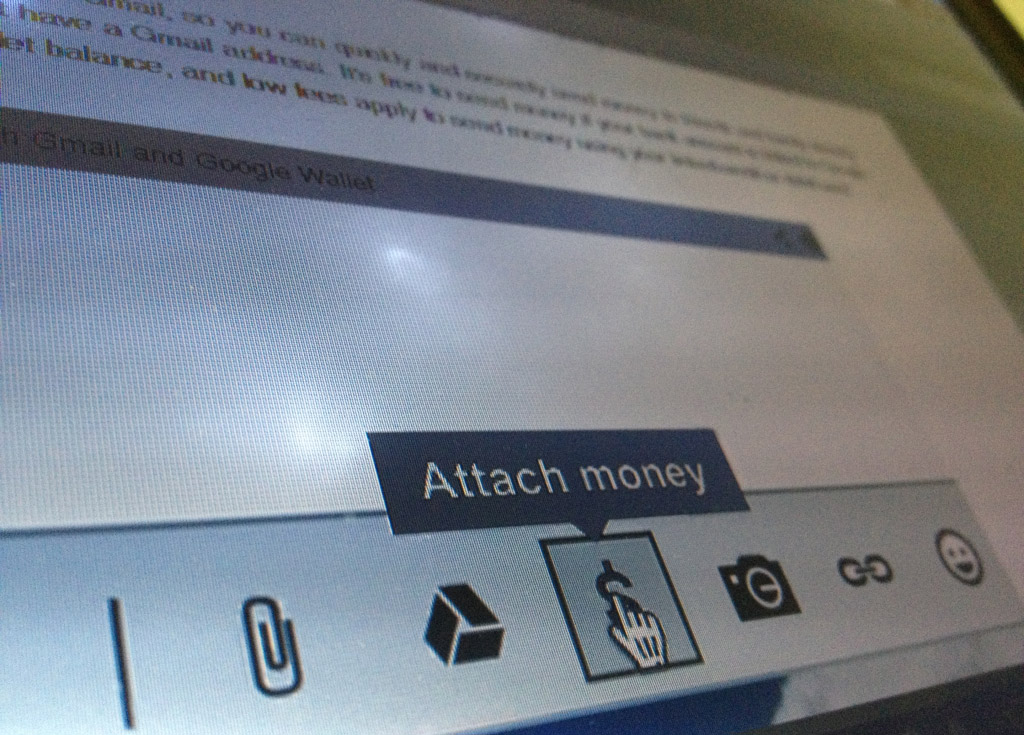

Google is combining its email service Gmail and its payment service Google Wallet into a service that allows users to send money via email. In order to do so, users must have a Google Wallet account. The transfer then takes place via the prepaid credit in the account, the user’s bank account, or his credit or debit card. In order to receive money, a user must log into his Google Wallet or set up a Google Wallet account. From there, the user can apply the money to a payment transaction or transfer it into his bank account.

Figure: “Attaching” Money via Gmail

Square announced that it will also enable the sending of money and the carrying out of payment transactions via email. At the moment, this service is only available to select users, but some information about the service is already available publicly. According to this information, users can send money to any email address they wish. The sender simply writes “pay@square.com” into the CC field and the sum into the subject line of the email. The receiver then links his debit card with the receipt and Square transfers the sum into the bank account connected to the card. So far it is still unclear what information the sender must supply to the service and how he is to prove his identity.

While Square charges a fixed fee of 0.50 USD per transaction, Google uses a more differentiated cost structure. Sending money from pre-paid credit or a bank account does not incur any charges, while sending money using a debit or credit card costs 2.9% per transaction, at minimum 0.30 USD.

Both Google and Square are providing their users with added convenience as a result of these services. Google is drawing on its ecosystem and combining it with money transfer via email. Square does not possess an ecosystem of its own and has no plans to create one in the near future. Instead, it uses bank accounts and debit cards for its services – at least for the receivers – and operationalizes emails in an indirect way, as it does not hold the money itself but routes it directly to the bank account of the user.

Aside from charging a fee for this service, Google’s advantage lies in forcing users into its ecosystem by requiring them to open a Google Wallet account in order to receive money. In addition, the data that is received from this service will also be of great interest to the internet company. By contrast, revenue from transaction charges seems to be a driver for Square, and its collaboration with JP Morgan Paymentech probably also plays a role.

For the user, these services make it possible to transfer money in a very easy way. The user’s email address is operationalized as a “unique identifier” in these transactions. In general, these services tap into the field of peer-to-peer transfers and expand the companies’ core services with this component that is suitable for transferring money to friends as well as for making payments.

It is unclear to what extent these services, which are currently offered only in the US, can be applied to European markets and the German market in particular. As it is notoriously difficult to transfer money in an uncomplicated way in the US, it’s possible that these services will not be successful there. In Europe, on the other hand, customers’ most important criteria when choosing and evaluating payment transactions are the security of the process and the credibility of the provider. A survey of German consumers shows ECC study IZV10 that consumers continue to place a great deal of trust in retail and savings banks. In answer to the question “Which provider of payment systems do you trust?”, 58.5% answered “retail and savings banks”, while only 7.8% also trusted internet service providers. It therefore remains to be seen whether the services by these non-banking providers will assert themselves in Germany.

SOURCES

Google, Gmail and Wallet

http://googlecommerce.blogspot.de/2013/05/send-money-to-friends-with-gmail-and.html

Square Cash

https://square.com/cash

https://squareup.com/help/en-us/article/5139-square-cash-overview

http://techcrunch.com/2013/05/20/square-cash-will-let-you-send-money-to-your-friends-by-email/

Meet our authors

Expert En - Artur Burgardt

Artur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment ...

Read moreArtur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment and banking products, modern technologies / technical standards, architecture conceptualisation and their use in complex heterogeneous system environments.

Read less