Value Creation revised — why old mechanisms are no longer enough

Technology in the focus of Value Creation at PEs

Key Facts

- Private equity firms are facing challenges in the current environment, including rising commodity prices, geopolitical tensions, and the consequences of the COVID-19 pandemic.

- Climate change and the need for decarbonization are adding complexity to the private equity landscape, as portfolios invested in carbon-intensive industries may face increasing costs due to regulatory sanctions and policies.

- The private equity market in Europe saw a decrease in activity in 2022, with a significant decline in deal volume and value, making exits more challenging.

- As a result, the valuegenerating mechanisms must be significantly more complex and solution patterns more multi-dimensional.

- Private equity firms are shifting their focus from leverage and price arbitrage to

operational improvements, driven by technological innovations and the need to adapt to digitization trends. - Thus, PE firms need to have a much deeper understanding of technology to continue to successfully drive value growth in portfolio companies in the technology space, but also companies in traditional industries.

Challenges of the current private equity environment

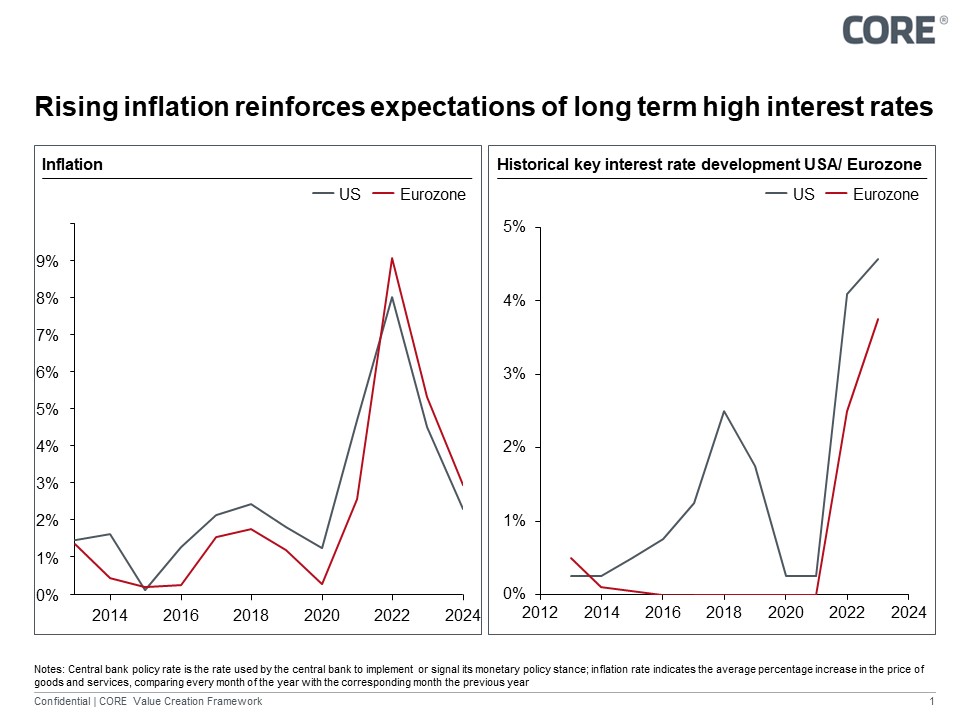

The world has reached a turning point. The skyrocketing commodity prices, increasing

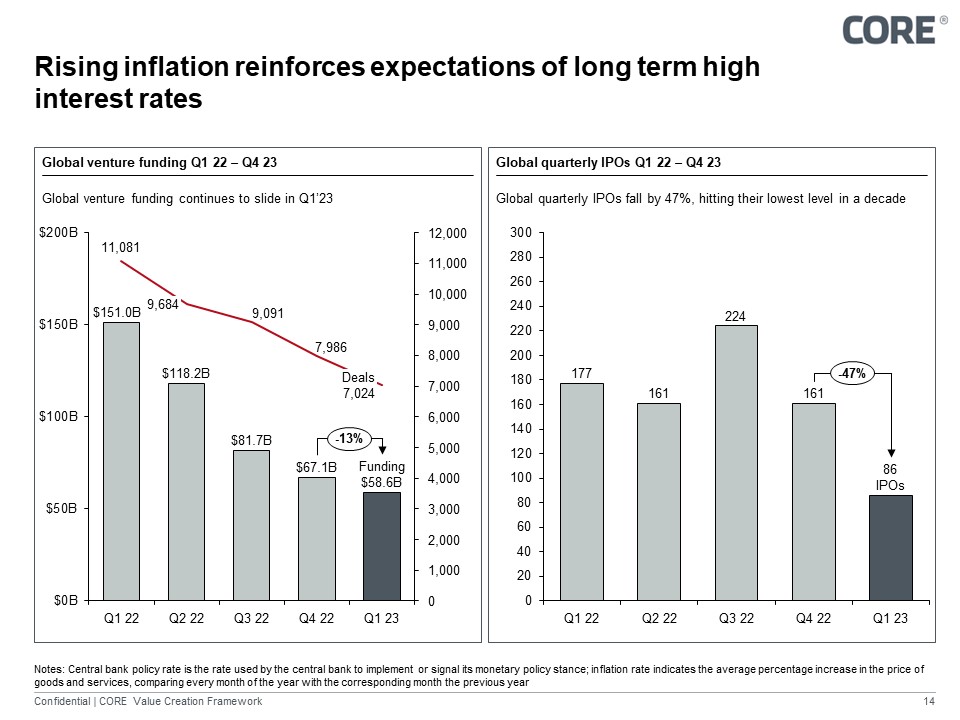

geopolitical tensions, the Ukraine war, and the consequences of the global COVID-19 pandemic are fundamentally impacting companies and value chains and causing considerable market distortions. The sharp rise in inflation is forcing central banks to tighten the ultra-loose monetary policy of the past decade(s). As shown in Figure 1, the US Federal Reserve (the FED) is not the only one attempting to suppress the rapidly spreading inflation with sizeable interest rate rises. Most recent publications from governing bodies, such as the ECB and the FED, show a further decrease of the inflation rate in the US to 4.9% and a slight increase in the Eurozone to 7.0 up 0.1% from 6.9% in March 2023. Even though the monthly inflation rates are declining in the long term, the regulators must keep interest rates high indefinitely to reach the 2% target.

Figure 1: Inflation and key interest rate developments

This challenging environment is further complicated by climate change, the global crisis overlaid in many places by current events and by no means under control. Fundamental investments are necessary in the resilience of the social and economic infrastructures, as well as for climate protection. Decarbonization of the economy and the promotion of green tech are some of the solutions pursued by governments and the private sector locally and internationally. However, significant efforts and concerted action are further required to transition away from the established carbon-intensive mechanisms. Some market participants interpret these developments as indicators of a deglobalization trend.

The private equity (PE) firms need to navigate this increasingly complex environment not only by accounting for the high inflation and high interest rates, but also by considering the costs of climate related risk. If the latter is not accounted for, the portfolios invested in carbon intensive industries are likely to experience increasing costs over time due to rising regulatory sanctions and restrictive policies aimed at transitioning the economy towards net zero.

However, without going into full detail, these developments will lead to a further increase in uncertainty and upheavals in business models and processes occurring at an increased speed. Planning is becoming more difficult, hence thinking in scenarios is necessary. But such times of change are - as they always have been – accompanied not only by considerable risks, but also by considerable opportunities.

Private equity shows signs of weaknesses

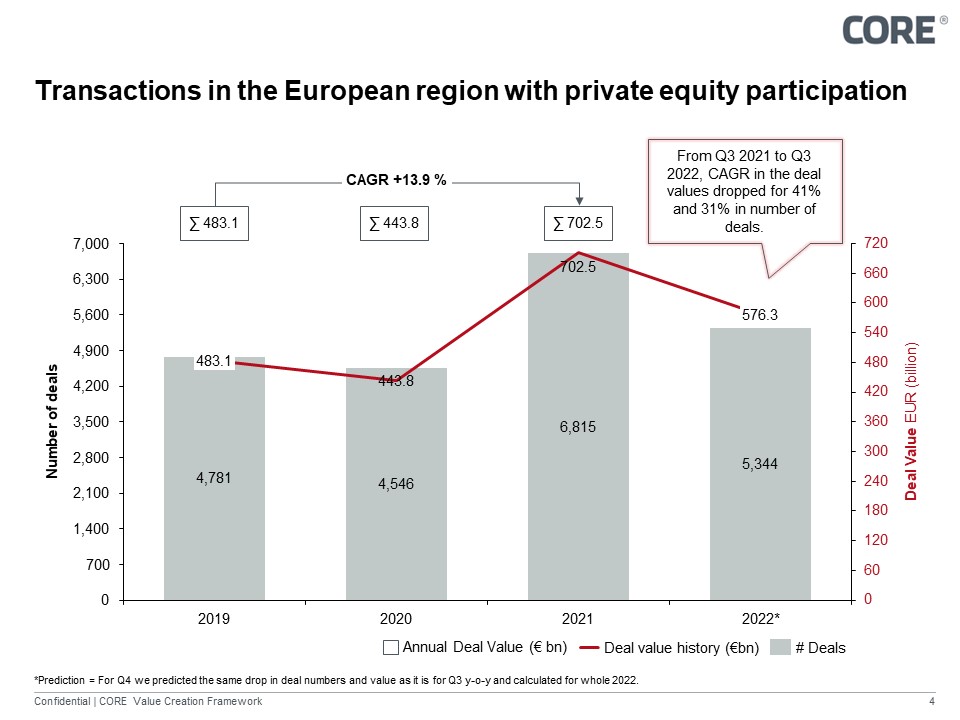

In Europe, private equity (PE) has demonstrated significant earnings strength and resilience during exceptional conditions in 2021. Even while large parts of the economy remained in a virtual shock freeze during the global pandemic, the transaction volume of PE investments increased by 13.9 % between 2019 and 2021, reaching a total value of EUR 702.5 billion in 2021 (Figure 2). Nevertheless, in 2022, the consequences of the global challenges have reached the PE firms’ balance sheets. While the deal market in Europe saw an increase in value in 2021, activity decreased significantly by 31% (41% in deal value) on a yearly basis in Q3 2022, indicating that cited problems are having a noticeable impact on the PE market.

Figure 2: European private equity transactions

Figure 2: European private equity transactions

In the presented situation, exits are becoming significantly more challenging. For instance, sponsor-to-sponsor trading has been noticeably reduced, and companies are once again more deliberate towards their cash flows and earnings. The method of a special purpose acquisition company (SPAC) as an alternative option has also become virtually non-existent. Exit activity has continued to decline towards the end of the year, as only the deals up to EUR 31.4 billion were completed in Q3 2022. With public market values decreasing, the initial public offering (IPO) route is less attractive. There have been indications that the falling public values may spread to private companies as well. This set of factors means that current investments will tend to be held for a longer period.

Figure 3: Overview global venture funding & IPO activities

The end of dozen years of growth in excess capital

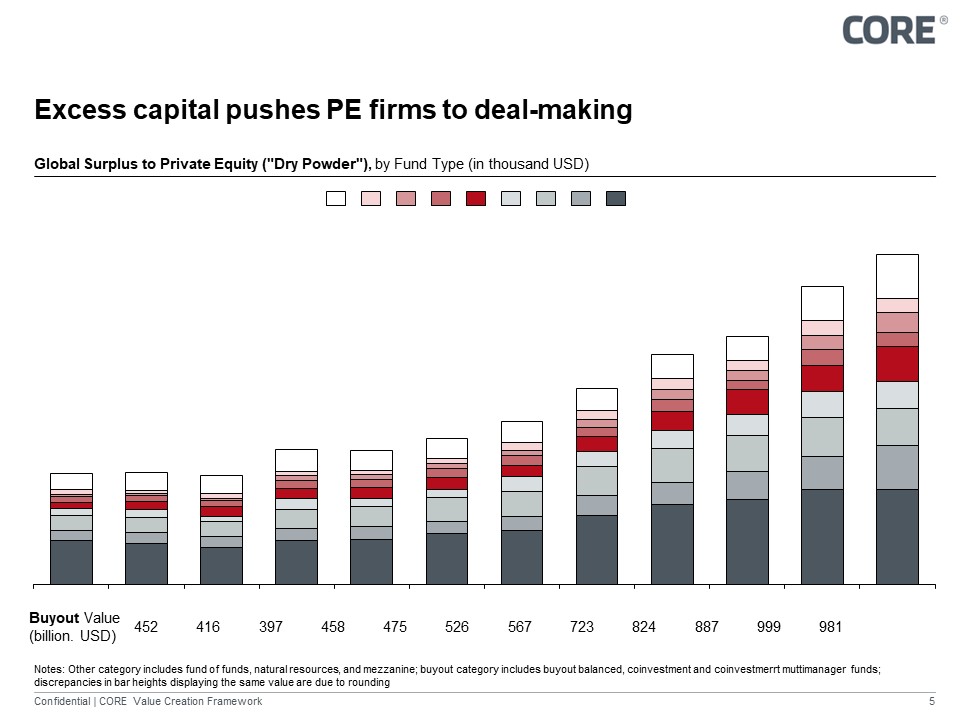

"Dry powder" in the private equity sector increased considerably to set new records in 2021 (Figure 3). “Dry powder” refers to cash reserves held by PE firms that are ready to be invested. While the excess capital of PE firms increased only moderately in the first half of the 2010s, this increase in “dry powder” accelerated in the second half. As shown in Figure 3, this trend is particularly evident in buyout deals, but also in investments in growth companies. In 2021, excess capital of USD 3.4 trillion was recorded, reflecting a tripling of "dry powder" within a decade. In 2022, based on the currently available data, this excess capital has been predicted to increase to USD 3.6 trillion, indicating that PE firms are well positioned to ride out the downturn and prepare for the recovery. In some cases, PE firms do this by testing out various downturn scenarios within their portfolio companies and, based on the results, adjusting their due diligence approach.

Figure 4: Worldwide private equity surplus

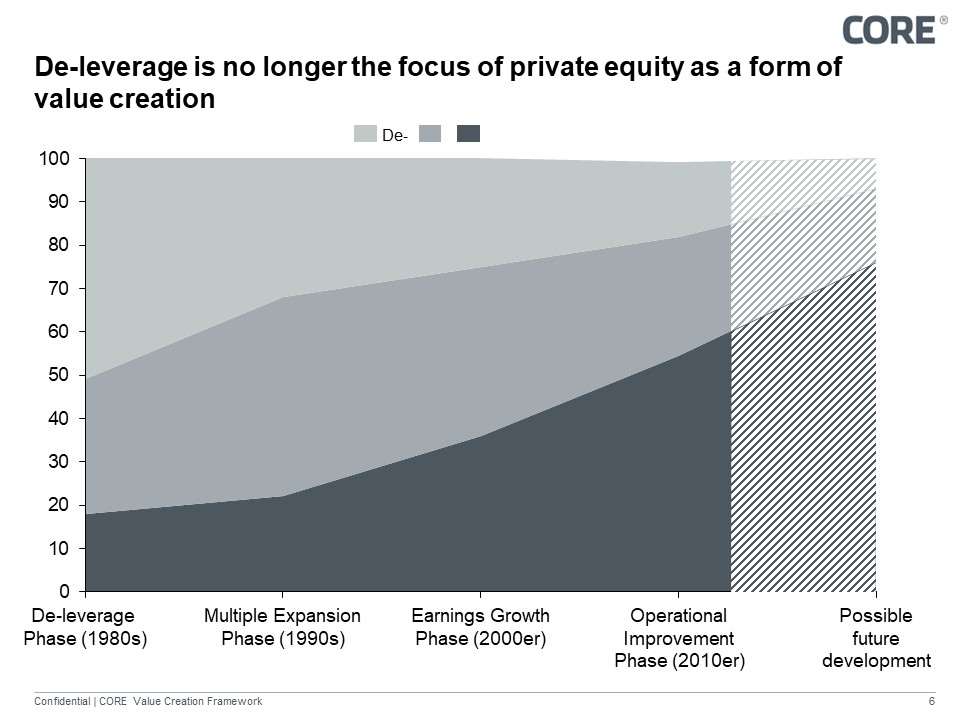

From leverage to operational improvement

Private equity firms as an alternative asset class encourage investment from wealthy sources by boosting greater return on investment (ROI) than other alternative classes. In 2022, both the expected ROI and the general rise in interest rates are putting additional pressure on earnings, while making it more expensive to access previously favourable debt capital (e.g., growth financing). Above all, the process of value creation must also be adjusted. Whereas in the 1980s, such investments primarily focused on debt reduction financed by private equity (Figure 4), and then on growth financing in the 1990s, today's focus is increasingly on operational improvements. This is driven by technical innovations, ongoing digitization, and, especially in the wake of the pandemic, by megatrends in automation, deglobalization and virtualization. The continuous development of new technologies, such as artificial intelligence (AI) and machine learning (ML), opens new possibilities of analytics for detailed consumer insights. The change in purchasing behaviour and trade conflicts are the catalysts for this development and are significant value drivers for the economy. The digitization of sales models, the development of digital business models, analytics, AI, and the automation of business processes are significant value drivers that stimulate both bottom-line and top-line growth in companies.

Figure 5: Focus of value added per decade has shifted in last 40 years

To increase investment returns, operating groups within PE companies have gained in

significance. Often combining internal and external expertise, the operating groups focus on strategic alignment and support within the portfolio companies. The proliferation of operational teams is consistent with the general philosophical shift among leading private equity firms to strategically align their assets post-acquisition and improve operational performance. To meet this requirement, employees from the middle, specialist management and former consultants are drawn into the companies, which contrasts with the traditional focus of C-level replacement/reappointment. In this way, private equities hope to gain more internalized knowledge, which can be used for even stronger bottom-line optimization. A survey by McKinsey & Company on the future of company composition of private equity firms also found that the industry plans to become even more actively involved in its portfolio companies in the coming years. This is also consistent with the recent results of a survey by PricewaterhouseCoopers (PwC). The results show that two-thirds of respondents (66%) indicated that the impact of "operational improvements" on return on investment has increased significantly over the past three years. 52% of the participants also see this effect with digitization and again 71% of the respondents assume that digitization as part of "Operational Improvements" will have an even more considerable influence on the return on investment in the future. It is therefore not surprising that buyout funds, which both have a major influence on the invested companies and bring industry expertise, can achieve the greatest value growth.

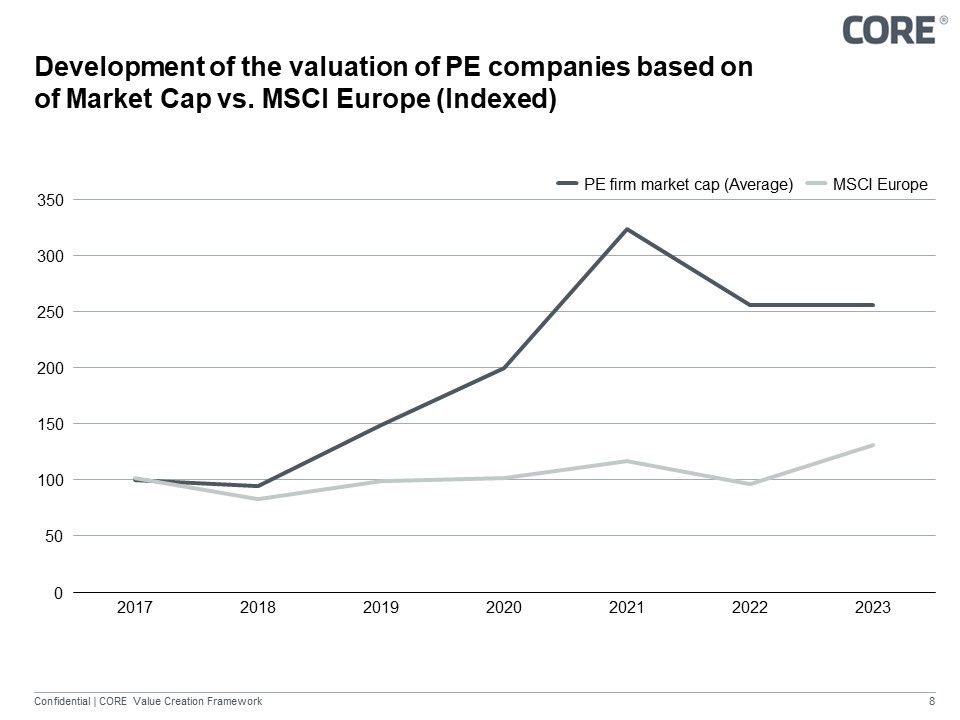

As a result, the value-generating mechanisms must be significantly more complex and solution patterns more multi-dimensional. This increasing pressure is also reflected in the valuation of PE companies. Figure 5 compares the valuation of listed PE companies operating in Europe with the development of the MSCI Europe Index over the same period and shows a similar trend with an exponentially higher valuation. To summarize, investment companies have paid record prices for their acquisitions, and in the short term they find themselves in a market with significantly worse conditions. To realize a successful, profitable exit, a more active approach designed to increase value is therefore necessary.

Figure 6&7: Valuation of private equity firms in the last 6 years compared to MSCI Europe

Figure 6&7: Valuation of private equity firms in the last 6 years compared to MSCI Europe

Value creation challenges - exponential digitization

The challenge in value creation today is based on the inherent pressure of technologization, and technological development is exponential in accordance with Moore's Law. New playing fields in the context of new business models (especially driven by tech companies) require increasingly strong technical knowledge in the context of opportunity evaluation and the identification of saving potential. In the early phases of the value creation approach, especially in the case of private equities, leverage then multiple expansion developed into earnings enhancement. Today the area of "operational improvement" is playing an increasingly important role. This development, which began in the 2010s, can be extrapolated further in today’s market. Private equity's traditional tools for delivering performance have become less effective, which is a natural evolution for a maturing industry. Leverage and price arbitrage are less effective than in the past and difficult to control. As the number of PE firms has steadily grown, returns from the former instruments have been largely crowded out.

The strategy of buying assets relatively cheaply and selling them expensively for multiple expansion is also less popular nowadays, as the business models of the investment objects have also changed significantly or may change during the investment period. For technology companies in particular, classic process optimization, simple outsourcing or cost-cutting no longer offer sufficient effects in value creation - the reason for this is more digitized or technologized business models, which often already offer lean processes and less room for business process outsourcing (BPO). Technology does not develop linearly; it often requires jumping to the next technology curve. Conversely, this means that PE firms need to have a much deeper understanding of technology to continue to successfully drive value growth in portfolio companies in the technology space, but also companies in traditional industries. Our clients cite outdated legacy systems, nonharmonized IT landscape, and a lack of attractiveness for know-how carriers as the biggest challenges, but also inadequately exploited digitization opportunities that prevent the expansion of new and old business models into digital services. Ergo, financial modelling is no longer a core competence for PE companies. It needs to be complemented by the ability to identify and mitigate challenges in the technological basis of their portfolio companies and to tap the resulting growth potential. Some companies in the market are not able to follow this trend or not fast enough.

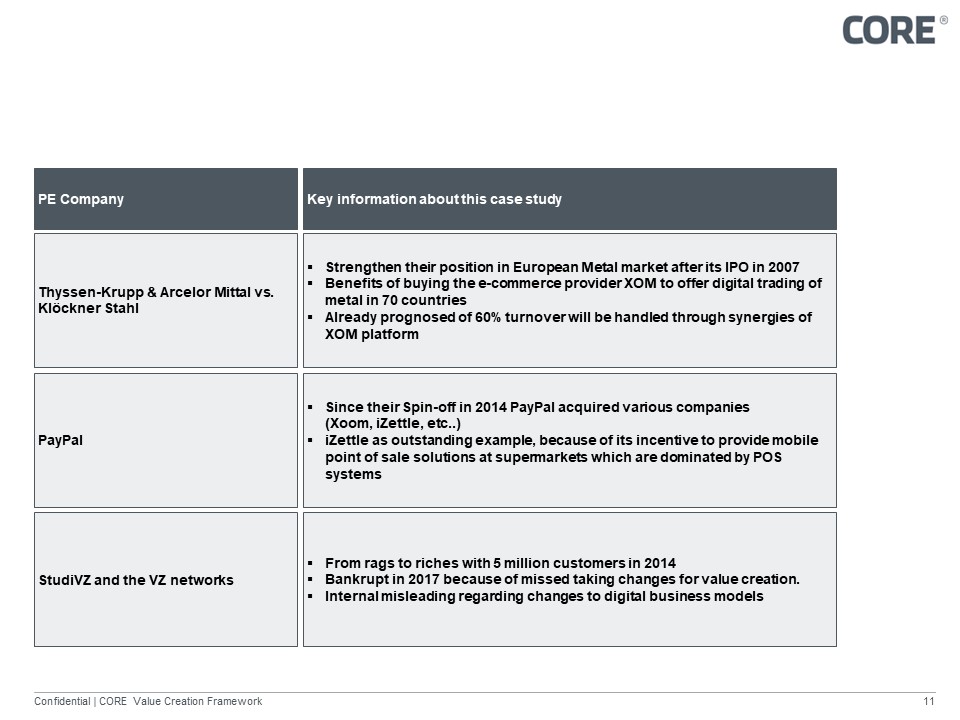

Table 1: Exemplary case studies

Table 1: Exemplary case studies

Why do synergy expectations fail?

Although the above examples represent only part of the challenge in value creation, it can be summarized that often the synergy expectations to increase the company value in M&A projects fail because the premises and fundamental mechanisms of action of technologies are disregarded. In the past, this was reflected, among other things, in the planned merger of two acquiring platforms, both of which relied on an outdated technology base. The merger has thus not only caused high running costs, but the parties were also incompatible concerning consolidation. The expected synergies and those factored into the deal could not be leveraged or could only be leveraged slowly, resulting in an insufficient increase in the value of the company. It is often observed that the overall picture of transactions and their respective objectives are not or not sufficiently in focus. Even when merging platforms, the decision for a target platform is decisive for the (technological) future of the company as well as the potential increase of the company value.

Thus, to achieve the target values of their transactions, PE companies need a clear general picture of the opportunities for technological development of their portfolio companies. These could be either to improve the top line (increased sales) or to realize necessary savings in the bottom line (decreasing costs). Already during due diligence in the deal phase, the initial situation should be understood at an early stage and precisely these levers should be identified so that they can be operationalized directly after the transaction has been completed. It is important to consider not only the financial targets, but also the technological restrictions and opportunities.

Often, incremental improvement is just an illusion, and the more promising and feasible approach is a different one.

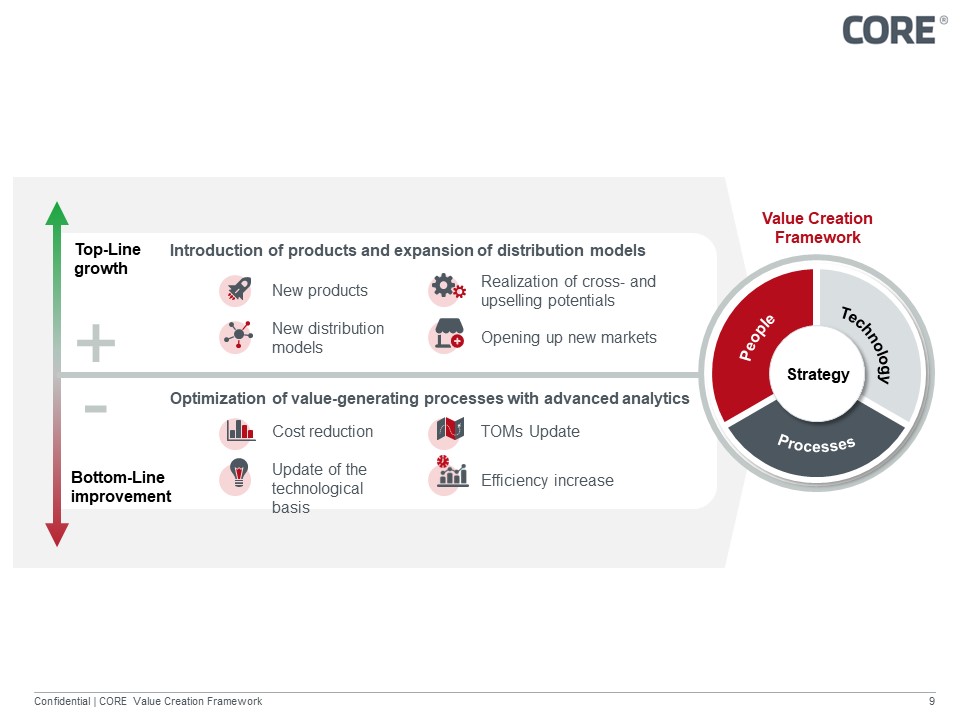

Figure 8: CORE SE - Value Creation Framework

Figure 8: CORE SE - Value Creation Framework

The traditional mechanisms of top-line growth and bottom-line optimization still apply. However, even though these two overarching levers have been tried and assessed for decades, the specific adjusting screws and mechanisms of action underneath them are constantly changing. With this purpose in mind and a focus on technological advancement, we have developed the CORE Value Creation Framework over the last few years. The goal was to find the IT-based levers within the top-line and bottom-line that would have a lasting positive impact on the company's value. At its best, the measures in the areas of top-line growth and bottom-line optimization support each other so that the maximum effect of value creation can be identified, generated, and made measurable.

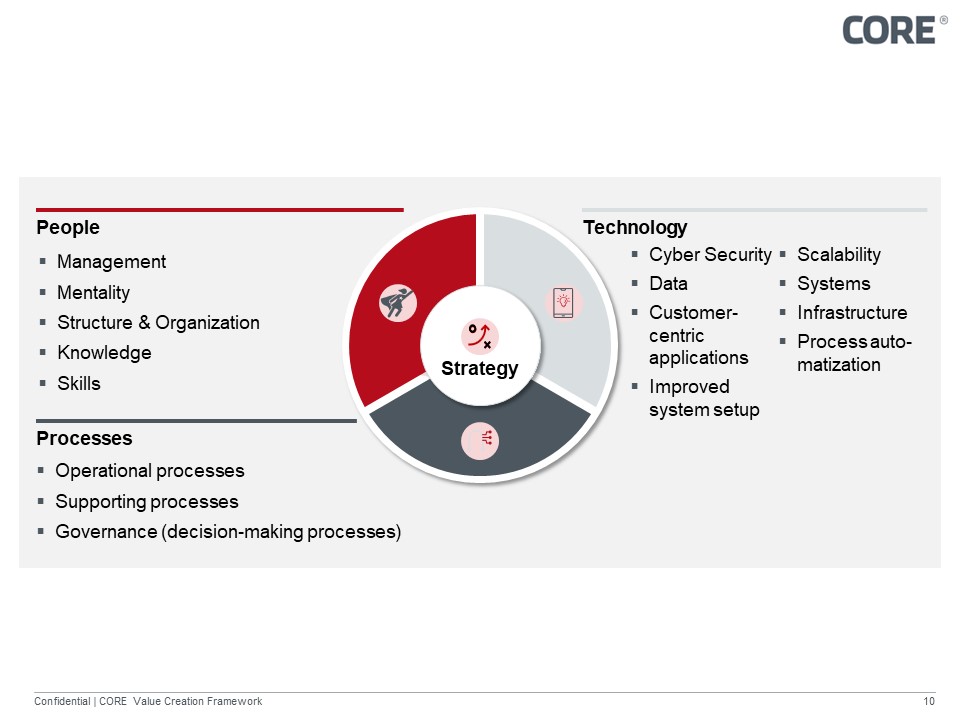

Figure 9: CORE SE - Value Creation Framework Deep-dive

Figure 9: CORE SE - Value Creation Framework Deep-dive

The four dimensions of the framework are applicable and valid for both top-line growth and bottom-line optimization. At the core of the framework is the strategic orientation of the respective company as well as the investment thesis. The focus for further consideration within the framework is also decided along the strategic alignment in the three dimensions of "personnel", "processes" and "technology". In the process, we see technology as the driving factor, after strategy, for the other two areas.

Strategic objective: At the heart of every acquisition - and the same applies to existing portfolio companies - is the strategic objective pursued and the investment thesis. This can either be determined within the company itself, or it can be predetermined (especially in PE portfolio companies). Regardless of whether the buyer has an increase in potential sales or an increase in efficiency in the target company's operations, all transactions impact the dimensions of personnel, processes, and technology. These interact with each other and determine whether the targeted improvements can be translated into reality. Mergers or carve-outs during the investment period expose the complexities, but also the opportunities.

Personnel: Employees affected by a takeover have a significant influence on the success or failure of a transaction. Private equities should not only attach importance to the involvement of top management, which in turn should demonstrate an open change mindset and pass this on to their employees. Middle management as well as (ex-) consultants can also positively influence the know-how in the company and contribute to value enhancement (often already relevant in the DD phase). In addition to soft factors, reviews of required and existing skills are part of the PE's job. Through appropriate training and the inclusion of necessary expertise in companies, the conditions for an improvement of the company situation are to be created. This also includes the retention and institutionalization of existing, market-differentiating knowledge. In any case, the personnel must be adapted to the changed processes and technology basis - if applicable - since a major skillset change is often required.

Processes: A similar principle is to be followed in the analysis of existing processes. PEs should identify procedures and strategically important processes when looking at a company to enable long-term success. Processes that do not add any differentiating value should be standardized and kept as lean as possible, or even fully automated or outsourced. Decision paths and options must follow the processes and technology in the company. The conversion of existing processes, which may have been in place for many years, again requires close coordination with the people affected and demonstrates how technology can promote the successful conversion of a company.

Largely unexploited is the possibility of joint coordination of services of portfolio companies (such as capital-forming benefits or insurance for employees) to reduce costs. The bottom-line value generated in this way optimally complements the vertical value of the companies. Other horizontal services can also contribute to increasing the value of the portfolio.

Technology: As a third factor, we consider technology as the one with the most potential for generating value for PE firms. In most companies today, it is interwoven with the core of their business and therefore offers broad opportunities for influence. For example, substituting old legacy software can significantly reduce long-term operating costs. At the same time, projects to modernize the IT landscape also offer the opportunity to simplify processes and realize the automation of processes. The introduction of solutions that are used profitably in other portfolio companies can also contribute to value creation through PE. Thus, the technology also offers cross-company potential for PEs. A so-called "best-of-breed" approach with different technology components in different portfolio companies can further positively influence value growth. The high relevance of technology is also reflected in the levers that have proved particularly profitable in recent years. These include the digital transformation of customer-centric technology, data analytics and cyber security, as well as the transformation of back-end processes, customer relationship management (CRM) systems and the digitization of manufacturing technologies. The post-transaction phase requires a comprehensive "blueprint" to demonstrate the potential of the portfolio company and realize it through dedicated projects. Detailed implementation plans, clear responsibilities, and a selection of metrics that measure operational and financial improvements are necessary to achieve this. Practice shows time and again that a 100-day plan is an important lever for identifying and implementing these measures. The measures are implemented by identifying key priorities such as new product launches, productivity-enhancing measures in sales or the integration of further acquisitions. Workshops with management provide a structured, interactive forum for investees and managers to develop a value enhancement plan. Speed is playing an increasingly important role here - approximately every second PE company has started planning and implementing value creation approaches earlier and earlier in the last 3 years. At present, increasing the value of companies can no longer be achieved (only) through a simple platform or business model consolidation, but works primarily in IT in bottom-line optimization. At the same time, IT is one of the most critical factors for many business models and thus also for value creation approaches for PEs. The good experiences show that with the help of this framework and the toolboxes below, value creation goals can be identified, evaluated, and implemented together with private equity companies.