The Digital Markets Act and Apple's concessions

Viel Wirbel um nichts, oder Opportunität für EU-Banken?

Key Facts

- The Digital Markets Act, which came into force in November 2022, requires six gatekeepers to fulfill certain "do's" and "don'ts" as of March 2024 to grand fair conditions for other service provider making business on a platform.

- Apple is one of the gatekeepers named. Consequently, Apple must make the NFC interface accessible to third-party providers, which means that banks and payment providers now have the option of offering a contact-free mobile payment service that is equivalent to Apple Pay

- In addition to the potential for differentiation and the strengthening of the company's own customer interface, the main reasons for formulating its own offering are to avoid significant fees to Apple

- Against the backdrop of regulation, Apple has formulated a proposal for concessions on

which interested market participants can comment by February 19th, 2024 - Irrespective of an existing Apple Pay product offering, banks should consider their options for action and their strategic positioning of any alternative products, as well as examine Apple's concessions in detail to help shape the regulatory process

Digital Markets Act - the EU is getting serious

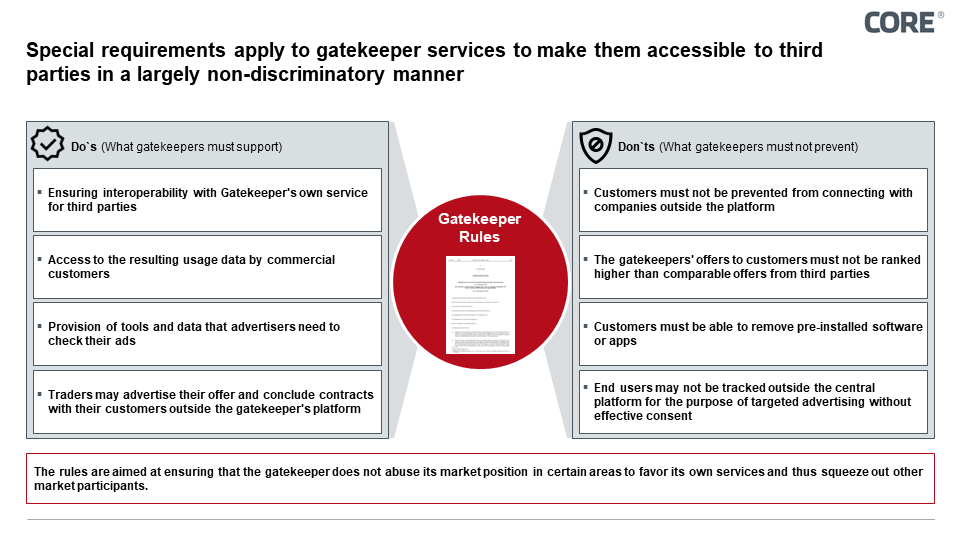

For a long time, the market power of large platform operators was a thorn in the side of the EU Commission, not at least because it also harbors geopolitical risks. The "Digital Markets Act" (DMA)1, which came into force on November 1st, 2022, set a regulatory counter-impulse: Threshold values were defined based on which platform operators with market power as a link between companies and consumers were identified as so-called "gatekeepers". Platform services that are actively used by at least 45 million customers are now subject to defined "Do's" and "Don'ts", which are intended to prevent the dominant market position from being used to improve their own product offerings on the platform.

Figure 1: "Do's" and "Don'ts", the specifications for gatekeepersr

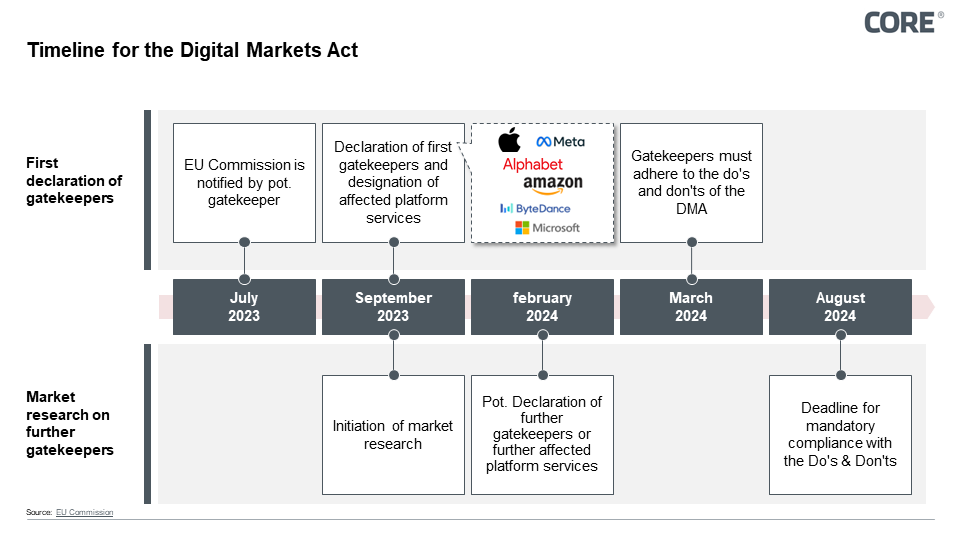

Specifically, six platform operators (Alphabet, Apple, Microsoft, Amazon, Meta & ByteDance3), with selected services were declared "gatekeepers" in September 2023. They have been given six months from the date of appointment to comply with the relevant requirements - heavy penalties wait for any violations (fines up to 10% of global group sales or even 20% for repeated violations). The companies are therefore obliged to implement corresponding measures by March 2024.

Figure 2: Timeline of the Digital Markets Act

Figure 2: Timeline of the Digital Markets Act

Relevance for banks and payment transactions using Apple as an example

The Apple Pay payment solution has been celebrating a global triumph since its launch in 2014: Continuously growing transaction volumes, numerous new markets opened, constant functional development and a de facto lock-in effect for banks that cooperate with Apple and offer the service to their customers - no bank has yet switched off Apple Pay!

This is possible not only due to the extraordinary usability, but also because Apple actively prevents the establishment of alternative NFC-based payment methods on Apple devices and thus (to date) access to the NFC interface for third parties in payment transactions (e.g., for the bank's own wallets). The card-issuing banks are increasingly being pushed into the background in terms of customer perception and at the same time must share income from the card business with other participants, such as for example Apple for providing the service.

Figure 3: Crowding out of traditional banking services by the Apple Pay ecosystem

Figure 3: Crowding out of traditional banking services by the Apple Pay ecosystem

Attempts have been made before (e.g., 2019 by the federal government as part of the "Lex Apple Pay") to dissolve the exclusivity for the use of the NFC interface, but so far without sustainable success. However, this is now likely to change: Even if there is no reference to the DMA in the proposal from Apple, the EU Commission published an offer from Apple on 19.01.2024 - i.e., shortly before the deadline expired - a, as we find, considerable concession towards the EU4. Apple offers the following proposal::

- Enabling third-party providers to access the NFC function of iOS devices free of charge (!), without having to use Apple Pay or Apple Wallet. For this purpose, Apple would provide APIs to enable equivalent access to the NFC components via

a host card emulation (HCE) architecture. - Scope of application would be for all third-party providers based in the European Economic Area (EEA) and for all iOS users with an Apple ID registered in the EEA. Furthermore, Apple will not prevent the use of these apps for payments in stores outside the EEA.

- Provision of additional features and functions, including the preset provision of preferred payment apps and access to authentication functions such as FaceIDand a suppression mechanism.

- Application of fair, objective, transparent and non-discriminatory criteria for granting NFC access to mobile wallet app developers.

- Establishment of a dispute resolution mechanism, in which Apple's decisions to deny access to NFC function are reviewed by independent experts.

These concessions will initially apply for 10 years. Interested parties have until February 19th 2024, to comment on Apple's proposals. This possibility to influence the design, in particular on a, with the Apple Wallet equal, option to set up the default payment application, banks and third

parties should definitely perceive.

The opportunity for banks and other payment players is therefore obvious: A proprietary NFCbased payment solution could also be offered for iOS devices, thus avoiding fees to Apple, tapping into differentiation potential and strengthening customer loyalty..

Does David stand a chance against Goliath?

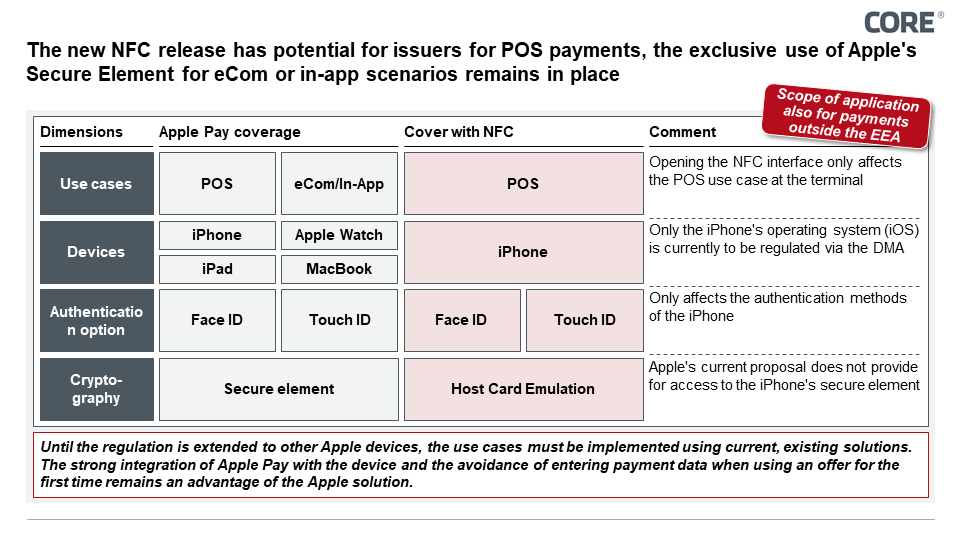

The proposal under discussion initially creates the basic conditions for an equivalent solution at the POS::

- A communication technology that is compatible with existing terminals; this would be the case with the NFC interface

- Convenient authentication options for the release of payments by the user; this would be given via the use of TouchID and FaceID

- The function to set a payment method of an alternative payment solution as "preferred payment method"; this would also be possible

- Payment option also beyond the borders of the EEA; this would also be given

The necessary condition for offering alternatives on iOS devices would now be met. Moreover, this is not limited to the payer side: acceptance solutions (like Tap-to-Pay) for the iPhone would also be conceivable and would enable banks to offer products for SMEs, for example. However, there are also limitations: End customers may still only be able to use Apple Pay for payments with the Apple Watch, as the separate operating system (WatchOS) is not covered by the current proposal. Furthermore, Apple's current offer to release the NFC interface only covers use case scenarios at the POS terminal. Payments in eCommerce and in-app purchases are not affected by this, although Apple Pay also has a strong market position here - particularly due to its integration in the App Store. However, the regulator has already initiated examinations regarding iPadOS.

Figure 4: Use case and functional coverage with an NFC-based solution compared with Apple Pay

Figure 4: Use case and functional coverage with an NFC-based solution compared with Apple Pay

What should banks do against this background?

In the status quo, most banks offer Apple Pay to their customers and thus accept that a significant proportion of their card revenue is transferred to Apple. For those banks that have spoken out against the introduction of Apple Pay due to the ongoing costs, there would now be the opportunity to formulate their own counteroffer to their customers. However, banks that currently offer Apple Pay should also examine whether long-term cost savings and strategic advantages could be realized based on the changed conditions - whether through an alternative offer or as a negotiating lever

The following applies in principle: The implementation of a payment solution is always a project with a significant up-front investment. When setting up their own NFC-based payment solution, banks must expand their own iOS app to include a corresponding NFC component, as well as https://core.se/en/insights /blog/from-digital-markets-act-and-apples-admissions central security components (e.g. tokenization services) integrate and - depending on the solution option - complex certification procedures (e.g. those of the Card Schemes).

Against this background, the question of the implementation approach arises, whereby three overarching scenarios are conceivable:

-

In-house development of required components

Such an option could be useful for larger banks that want to offer their customers an alternative to Apple Pay, with a focus on time-to-market, differentiation potential and flexibility. The costs for this would have to be paid individually by that bank. - Integration of a 3rd party solution (SDK or white label app)

Banks are looking for software providers, which can offer a corresponding solution for iOS. Potential providers are those who currently offer NFC wallets as an SDK or whitelabel app for Android and could adapt these for iOS. Banks could save time and sometimes also development effort by using ready-made SDKs and it can be assumed that those providers benefit from their experience on Android devices and increase efficiencies. Because iOS solutions would first have to be developed by these providers and then adapted by the banks, the expected time-to-market is likely to be similar to an individual development, but the differentiation-potential significantly lower. Costs can be socialized for this

- Solution development in an alliance

Banks join an association or initiate one with the aim of collaboratively tapping the new potential solutions that arise. In addition to the possibility of cost socialization, it should be emphasized that initiatives such as the European Payments Initiative (EPI) for account and Instant based payments already cover other facets of payment transactions, which means that an extension of the solution to include contactless payment would not be limited to the NFC use cases granted by Apple. For example, due to instant payments eCom or in-app payments are also possible. In the medium term, even POS payments would be conceivable, for which - assuming support by the terminals - the IBAN is exchanged between the payer and payee via NFC, meaning that there would no longer be any need for a card scheme to be involved. This should also be in line with the EU's regulatory agenda..

But how can consumers who have grown fond of Apple Pay be persuaded to accept an alternative offer from the banks? One possible approach for banks would be to use the avoidable fees to Apple for customer-centric cashback programs, provided this is compatible with the commercial guidelines from the contracts with Apple (keyword "non-discrimination rule"). Also, functional additions which are not yet offered by Apple in this country (e.g. Buynow-pay-later) could be a lever. Banks are therefore, regardless of a possible existing Apple Pay offering, well advised to follow the developments described closely and to formulate answers to the questions that arise on their short-term strategic agenda. Software-providers or initiatives such as EPI should also reassess their strategic positioning and resulting options. They should, just as banks, use the opportunity, to give their feedback on Apple's offer regarding the NFC interface by February 19th to the EU Commission, so that ideally interests of alternative payment methods are also considered.