Hybrid engagement in wealth management

Unlocking the digital future: Playbook for innovative Wealth Managers

Key Facts

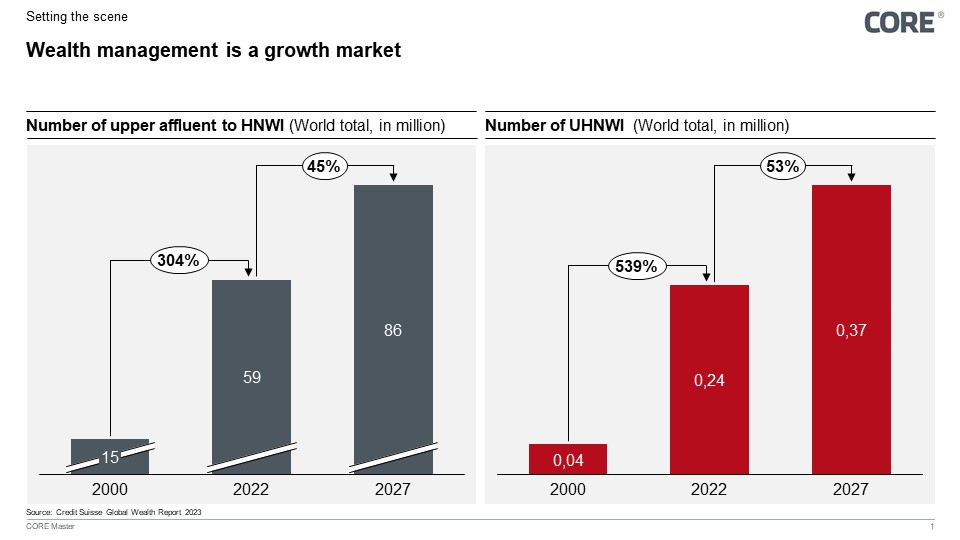

- Wealth management, the banking industry's most lucrative sector, delivers a Return on Equity (ROE) that normally surpasses the banking industry average. Fueled by a rising clientele, the market is set to expand further with the population of high-net-worth individuals (HNWI) and ultra-high-net-worth individuals (UHNWI) projected to surge by 45% and 53% respectively by 2027.

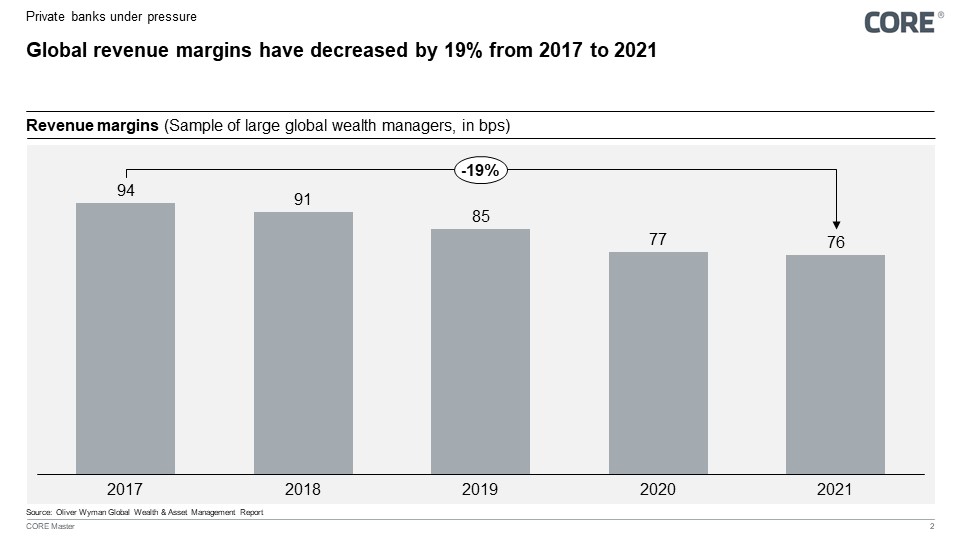

- Global revenue margin for wealth management is under pressure with a 19% decrease from 2017-2021. However, the largely untapped affluent sector, expected to account for ~60% of the total revenue and generate about $45 billion in new revenues between 2021-2026, presents significant growth potential.

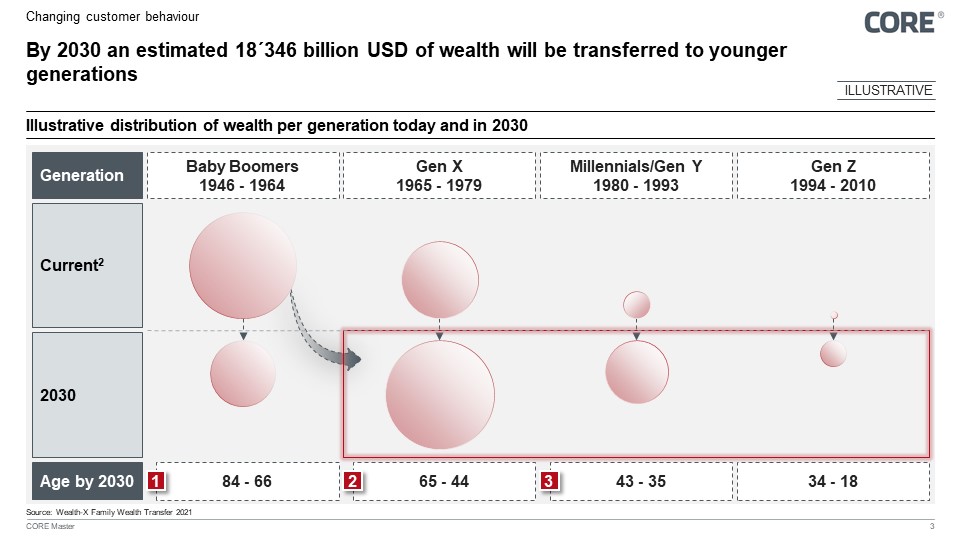

- The greatest intergenerational wealth transfer in the history is happening. Between 2023 and 2045, $84 trillion in assets will be handed down to Millennials and members of Generation X. High-net-worth individuals with a net worth of at least $5 million—will be passing down $15.4 trillion of wealth to the next generation by 2030.

- Market trends necessitate a digitalized engagement model, however most wealth managers in the DACH region lack comprehensive digital solutions, with CORE research indicating that 90% of the researched wealth managers do not offer digital onboarding and only 3% of them provide digital advisory services; furthermore, despite some experimentation with AI assistants, many still rely on less user-friendly traditional digital channels.

Wealth Management - A growing market

In the vast world of banking, wealth management stands out as the most profitable sector, with impressive Return on Equity (ROE) numbers. For example, JPMorgan's wealth management unit had a remarkable average Return on Equity (ROE) of 27.3% in the three years leading up to 2019, which significantly outperformed the group-wide average of 13.8%. Bank of America's wealth management unit achieved an annual ROE of approximately 22% in 2017, nearly tripling the group-wide average of 8.1%, which emphasize the attractiveness of wealth management as a lucrative sector in the banking industry.

In addition, the client pool has been significantly increasing: As shown in the graphs below, the number of individuals of upper affluent to the HNWI category is growing, which is expected to persist. Similarly, the number of UHNWI follows this growth path.

Figure 1: Rising HNWI and UHNWI population

Figure 1: Rising HNWI and UHNWI population

Market Trends

Currently four pivotal trends reshaping the market are observable:

Trend 1: Wealth management profit margins are under pressure

In recent years, the field of wealth management has encountered a tough environment as the profitability of banks has not maintained pace with the increasing market potential.

Figure 2: Declining profit margins

Figure 2: Declining profit margins

There are several reasons: as the client mix concentrates towards UHNWI, their high negotiating power results in pressure on mandate margin even without actual bargaining discussion. The continued change in product mix towards cheaper passive products is another reason. Besides, the deposition margin contraction between the interest rates banks earns on loans and the interest rate they pay on customer deposits also leads to pressure on revenue margins. Moreover, increased competition in the sector adds to the pressure as the spending on customer acquisition and retention is higher and it may cause price cuts.

Trend 2: The greatest intergenerational wealth transfer has started

Another prominent transformative trend is the intergenerational wealth transfer of $84 trillion2 in assets that will be handed down to Millennials and members of Generation X between 2023 and 2045. The world’s richest individuals – those with a net worth of at least US$5 million – will be passing down $15.43 trillion of wealth to the next generation by 2030.

The next generation are more tech savvy and keen on socially responsible investing. They have a fundamentally different expectation about the products, the services and the way wealth managers interact with them. Wealth managers need to get ready for the demographic change.

Figure 3: Wealth generation trends: A look at today and projected changes for 2030

Figure 3: Wealth generation trends: A look at today and projected changes for 2030

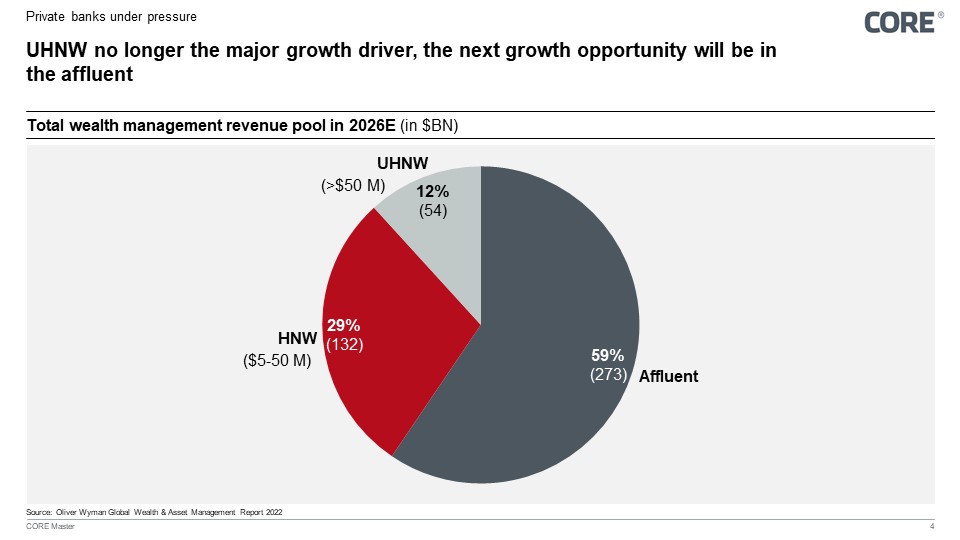

By 2026, it is estimated that UHNWIs with assets exceeding USD 50 million are projected to contribute only 12% to the total wealth management revenue pool. The remainder of 88% is distributed between HNWI (29%) and Affluent (59%). While the lower end of affluent customers (USD 0.3 - 0.5 million) is actively served by retail banks, and the higher HNWI (USD >10 million) actively by private bankers, there is a vacuum for the customers between USD 0.5-10 million. This customer segment’s needs are too complex to be served by the typical retail bank, but its wealth is not enough for wealth managers to grant a full white glove4 service.

Yet, this segment constitutes a huge market opportunity. It is simpler to be served than the current target group is, and less likely to negotiate harshly the management fees. However, the expected revenue per customer is much less than that of the top 20% of the highest wealth band. Therefore, the cost to serve need to be reduced to meet a healthy cost-income ratio.

Figure 4: Revenue pool in 2026

Trend 4: Technological disruption accelerates competition

Private banking, traditionally rooted in personal relationships, faces heightened customer expectations set by tech giants like Netflix, Google, Amazon, and Apple. These companies have raised the bar for convenience and digital experience, compelling wealth managers to carefully design and execute luxury experiences in the digital realm. For instance, Amazon, known for its seamless shopping experience, has also influenced customer expectations. As customers increasingly engage with seamless digital experiences, wealth managers must leverage state of art technology to authentically replicate these expectations.

While Universal banks can deploy their experience with the digitization of retail and affluent segments to their private banking divisions, pure play wealth managers have no rich experience in the digital space.

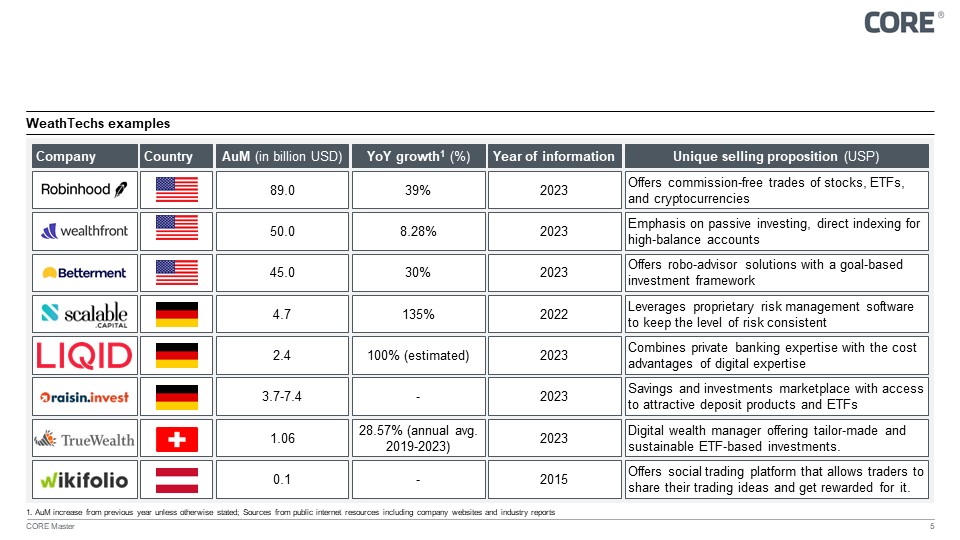

Additional market contenders such as wealth techs are trying to attack the customer interface by providing witty frontends and seamless processes.

Figure 5: Wealthtech examples

Figure 5: Wealthtech examples

Facing these innovations, wealth managers are either developing digital solutions or acquiring wealth techs like these to stay competitive, leveraging their technology to bridge the digital gap in the rapidly evolving financial sector.

Current digital offering of wealth managers in the DACH region

To understand the positioning of established wealth managers considering the mentioned market trends, an outside-in assessment of the existing digital offerings was conducted.

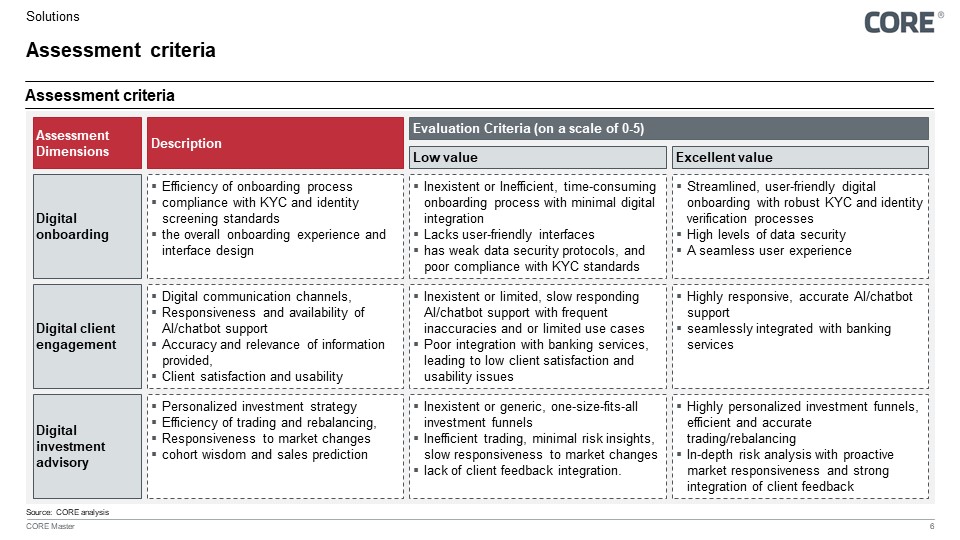

Assessment criteria

Our research on 52 samples wealth managers in the DACH region has showed that while most pure-play wealth managers in the region offer digital banking through web and mobile platforms, their services are not comprehensive. We assessed the institutions in 3 key dimensions.

Figure 6: Assessment dimensions and criteria

Figure 6: Assessment dimensions and criteria

This research is based on publicly accessible information and is intended to provide an 'outside-in' perspective. While we strive for accuracy with four-eyes principle, we acknowledge that it can exhibit discrepancies due to the nature of the sources. As an independent third-party consulting firm, we assure readers that we maintain a neutral stance in this assessment.

Result summary: wealth managers’ digitalization still in an early stage

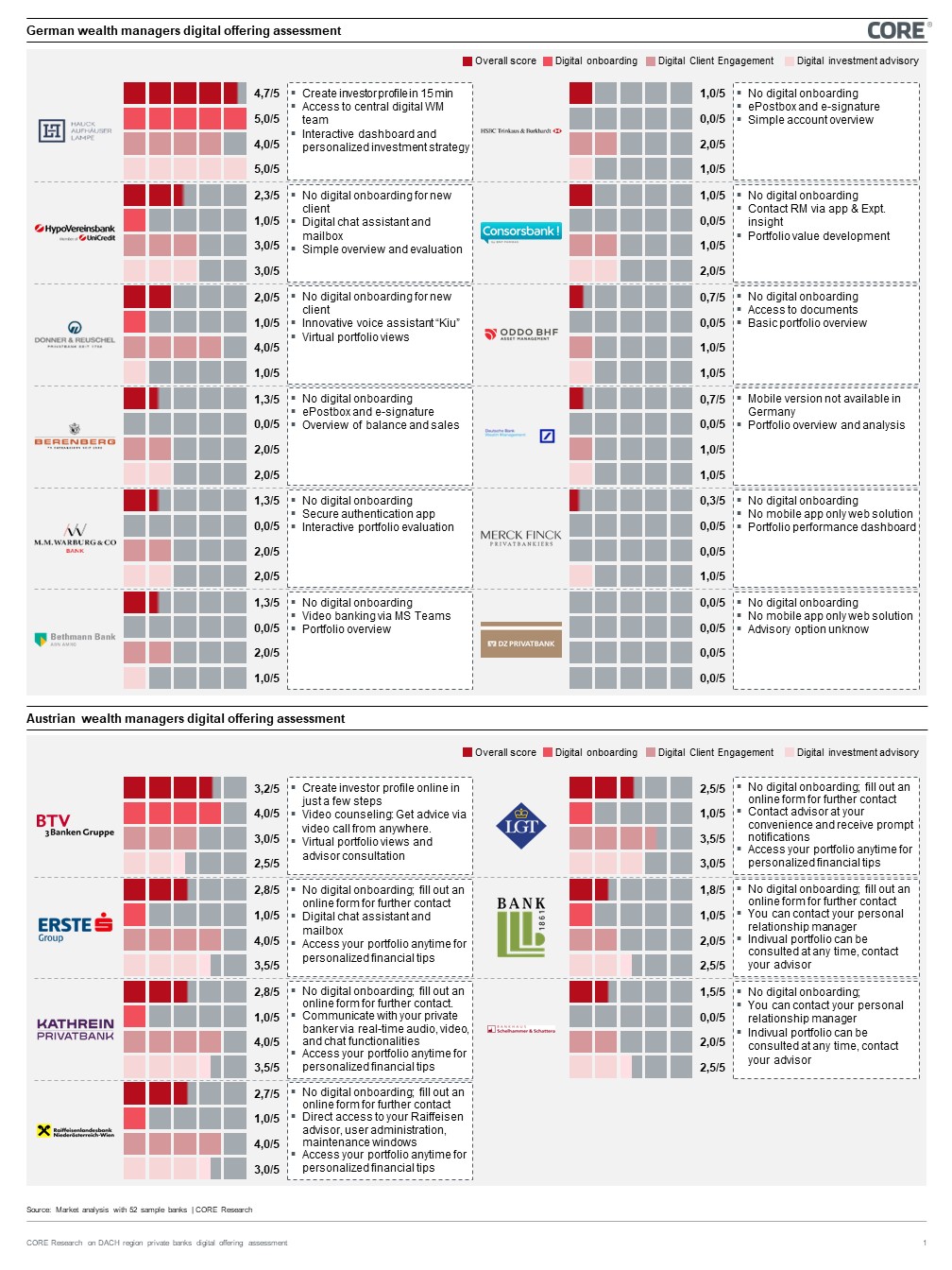

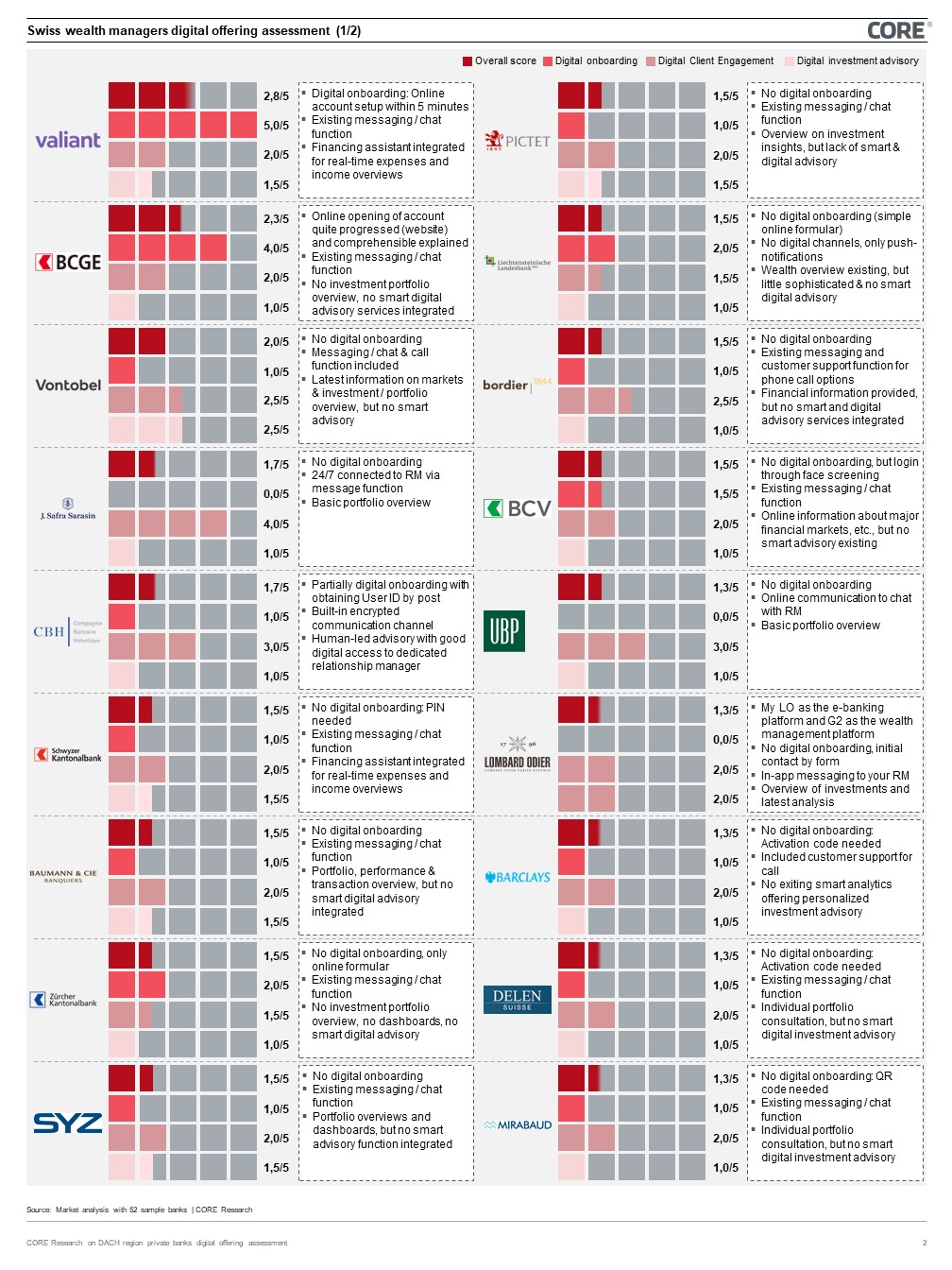

The research result reveals that 90% of these banks lack digital onboarding, requiring the assistance of a relationship manager for customer enrollment. Only 3% provide remote digital advisory services for customers to distill a personalized investment strategy for a discretionary mandate by themselves. On a more positive note, over half of these banks offer digital communication channels, including secure in-app messaging and video conferences. This research indicates that most wealth managers in the DACH region do not offer a comprehensive digital solution and still heavily rely on a costly, non-scalable, relationship manager-centric approach.

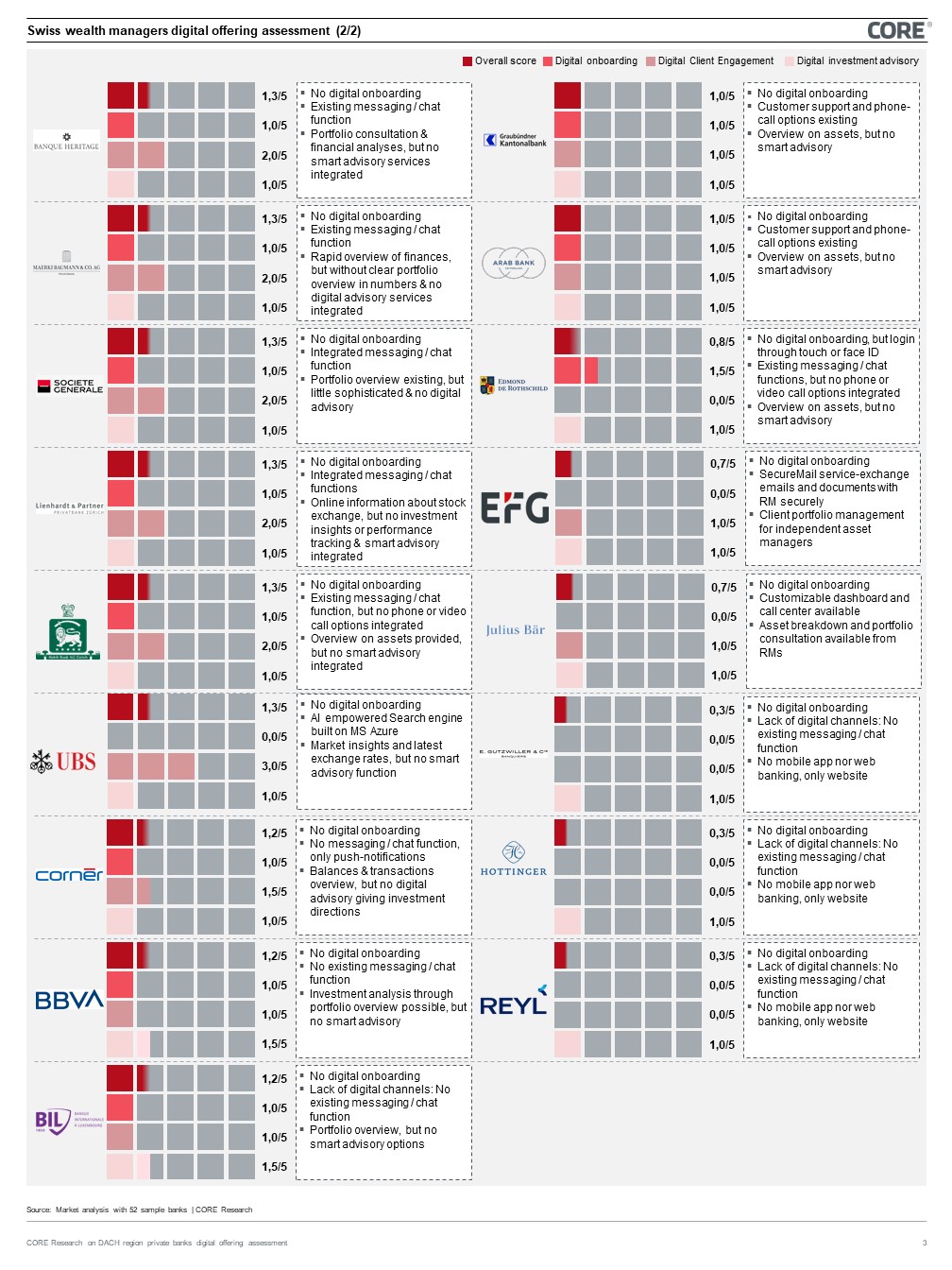

Detailed result by three markets

Figure 7: German and Austrian wealth managers digital offering assessment

Figure 8: Swiss wealth managers digital offering assessment (1/2)

Figure 9: Swiss wealth managers digital offering assessment (2/2)

The need to transform

The market assessment confirmed that the digitalization progress in wealth management is not far progressed. Even if the market players currently do not yet feel larger issues in their daily business so this topic could be perceived as a minor problem, the lack of digital offerings could become business critical in the foreseeable future:

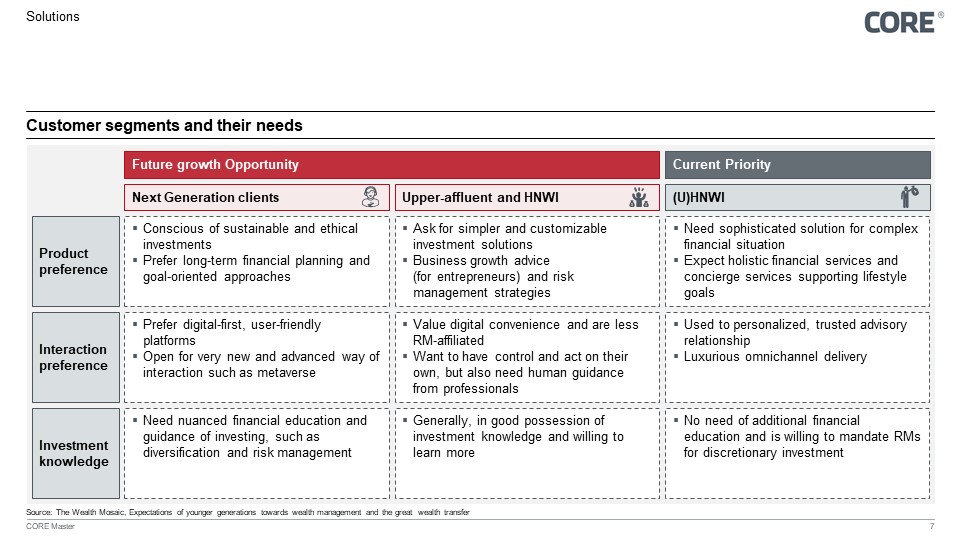

Emerging client segments have different needs

As stated in the market trends, the great intergenerational wealth transfer will bring in next generation clients. And the under-served upper affluent to lower HNWI segment is the next growth opportunity. In comparison to traditional upper HNWI and UHNWI segments, these emerging groups exhibit unique and distinct needs.

Next generation clients

This demographic is transitioning from the affluent category into higher wealth brackets. They are either beneficiaries of substantial wealth transfer or self-made individuals, primarily through entrepreneurship. Their key need from a bank is support in understanding and managing stock portfolios, financial planning, and taxation. Given their mobility and the need for constant access, these clients require round-the-clock banking advice and services.

Upper affluent – lower HNWI (USD 0.5 -10 million)

Customers of top private banks within the 0.5 -10 million EUR bracket have traditionally been served in a primarily reactive manner. They would appreciate a more proactive and engaging relationship with their bank. These clients, possessing substantial banking experience, require investment services that are both straightforward and customizable. However, given the demographic diversity of this segment, there is a varied demand for levels of human interaction.

Upper HNWI – UHNWI (> USD 10 million)

These customers expect the service to continue as-is. However, they too require access to a seamless digital experience.

Figure 10: Current focus and future growth opportunities

Figure 10: Current focus and future growth opportunities

While the three different segments have varying needs, they share a common denominator: a seamless digital experience combined with varying levels of personalized human-led service.

Traditional engagement model is not suitable to serve new client segments

Wealth managers offer private clients a broad variety of services and charge a management fee on the assets under management (AuM). They service their clients historically through excellent relationship managers and an array of subject matter experts such as art consultants, tax specialist, and even lawyers. The revenue formula for wealth managers is simple: AuM multiplied by revenue margin (normally in bps). Following the Pareto principle, where 80% of wealth is held by 20% of the population, revenue drivers are primarily concentrated within the top 20% of a bank’s customer portfolio. Due to capacity limitations of relationship managers (RMs) and the high cost to serve, banks typically focus on proactively managing the highest AuM clients.

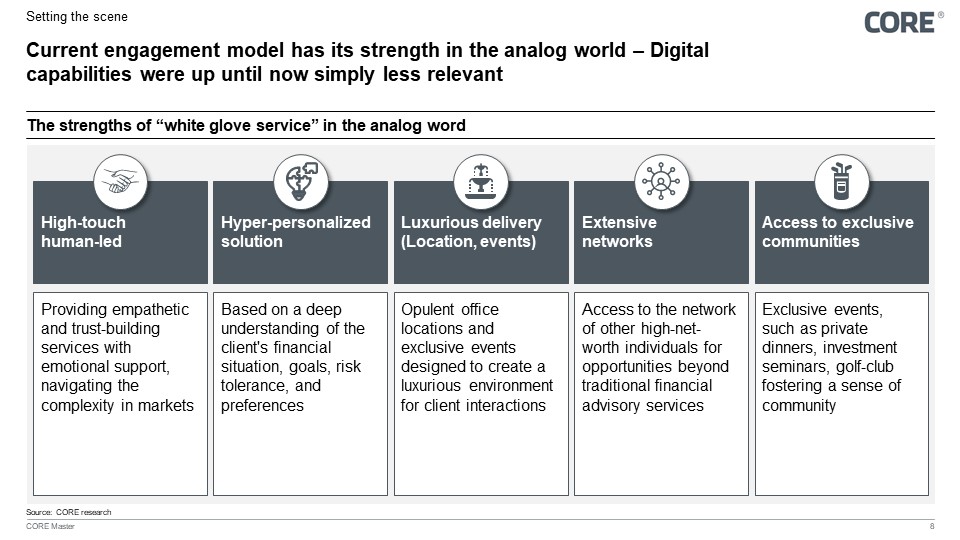

The “white glove service” provided by relationship managers has its strength in the analog world:

Figure 11: White glove service strengths

Figure 11: White glove service strengths

However, this type of 'white glove service' is not sufficiently scalable to expand the customer base and pro-actively serve it in a meaningful, revenue-increasing way. This is due the incompatibility of today’s high cost to serve structure with the smaller profits gained per customer. On the other hand, clients in the upcoming segment have simpler wealth management needs. The traditional white glove service and in-depth expertise would not be appreciated by the high-affluent to lower-HNWI clients. In the worst case, the service could be perceived as unnecessary and expensive. Lastly, relationship managers will not have the capacity to maintain such a high level of service for each of their clients.

Cost to serve too high: Digital tooling can improve the efficiency

The next generation clients and the high potential affluent clients will be the major force contributing to the revenue pool of the future wealth management sector. To serve a larger and different client segment, the current traditional client engagement model needs to transform to be more effective and more cost-efficient.

Table 1: Average cost to serve in different delivery models

Digital tools can reduce costs in three ways:

- Reducing personnel cost: By automating repetitive and time-consuming routine tasks, such as data entry, transaction processing, and document management, digital tools can free up RMs to focus on client-centric activities, optimizing workforce and allocating personnel where they add the most value. Digital tools also enable wealth management firms to scale their operations without significantly increasing their workforce. As the client base grows, firms can handle more clients with minimal additional staffing costs.

- Reducing operating expenses: Operating expenses include rent, equipment, inventory costs, payroll, marketing, insurance, and resources allocated for research and development. Digital tools enable cost-effective communication with clients through video conferencing, secure messaging platforms, a lot of expensive in-person meetings and associated travel expenses can be saved. Marketing activities are also mainly focusing on online initiatives which are more cost effective than traditional marketing campaigns. Moreover, most administrative processes can be digitalized which saves time and money.

- Avoiding investment errors and compliance risk: Digitalization streamlines portfolio management tasks such as rebalancing, tax optimization, and performance tracking. These processes become more efficient and less resource-intensive. Automating compliance checks and reporting through digital tools can reduce the risk of regulatory fines and the costs associated with manual compliance efforts.

In addition to cost savings, the adoption of suitable technologies enables mass personalization and overcomes the bottleneck of human capacity. A data-driven approach empowers relationship managers to efficiently cater to a large clientele, ultimately enhancing customer value and satisfaction.

The challenges to transform

In the face of competition from digital native wealth techs and universal banks equipped with robust digital capabilities, pure-play wealth managers must take proactive steps to avoid falling behind in response to market trends and the need to transform.

However, established and pure-play wealth managers in most cases need to face some challenges:

Technology: Lack in digital capabilities

Certain digital capabilities are crucial, including advanced data analytics for personalized marketing and sales facilitating, omnichannel integration capability and accessibility, AI-enhanced client interaction, data-driven investment advisory, automated reporting and RegTech solutions. However pure-play wealth managers often lack such digital capabilities.

Many of pure-play wealth managers still operate with outdated technology infrastructure, which hampers their ability to effectively implement digital engagement models. Furthermore, the online presence may be weak, which can lead to a poor customer experience, making it challenging to attract and retain tech-savvy customers.

Money: Costly initial investment and heavy technology debt

The burden of heavy technology debt is a major obstacle for pure-play wealth managers looking to transition to new models. Many of these banks rely on legacy systems that were not designed for modern digital interactions. These outdated systems often lack the flexibility and integration capabilities needed to support digital engagement effectively. Moreover, modernizing legacy systems to support digital models can be costly and complex. Integrating new technologies with existing infrastructure while maintaining reliability and security is a significant challenge.

Organization: Not ready for change management

Adapting to new engagement models often requires a fundamental shift in the organization's culture and practices. However, pure-play wealth managers may encounter resistance to change within their organizations. RMs may be hesitant to embrace the changes necessary for adopting these models, leading to slowdowns and internal friction.

Skill gaps can be another issue, as RMs may lack the necessary expertise to operate in a more digitally oriented environment, offering extensive training and development programs to align the organization's culture with the demands of digital transformation is a task that requires ongoing effort and commitment.

Compliance: Data privacy and security concerns

One critical challenge is compliance, with a particular focus on data privacy and security concerns. As the financial industry is highly regulated, wealth managers entering the digital realm must navigate a complex web of rules and regulations to ensure their online operations meet stringent legal and ethical standards. The digital transformation involves processing and storing sensitive client information and transaction data online, which raises significant compliance hurdles. Besides adhering to the General Data Protection Regulation (GDPR) in Europe, wealth managers must also address regional data protection laws, such as the Personal Data Protection Act (PDPA) in Singapore, the UK Data Protection Act, or Switzerland's Federal Act on Data Protection (FADP), depending on their operational regions.

These banks must provide robust assurances to clients that their confidential data remains impervious to cyber threats and breaches. Moreover, given the dynamic nature of compliance standards across various jurisdictions, continuous adaptation is essential, especially for banks engaged in cross-border operations. Thus, maintaining a thorough understanding of compliance with a diverse range of relevant laws and regulations is essential to ensure ethical and legal standards are consistently met in the ever-evolving landscape of financial services.

Brand and value proposition: Balancing high-tech and high-touch

It is ideal to segment different clienteles into different types of engagement model, however, in reality, it is much more difficult to implement. Even within the same segment, customer preferences can vary significantly, with some clients seeking face-to-face interactions, while others prefer automated, digital experiences. Finding the optimal allocation of resources to meet the diverse needs of the customer base can be complex.

Digitalization can help wealth managers increase the scalability of their business model significantly. However, it also gives rise to another problem: as the bank broaden its customer reach, will the premium or even luxurious brand value be diluted?

Therefore, balancing high-tech and high-touch in a scalable and customer-centric manner without diluting the brand value presents a significant challenge for the pure-play wealth managers.

The hybrid wealth proposition as a promising solution

So, what is the recommendation to digitalize and transform the wealth management business model to the changing market requirements?

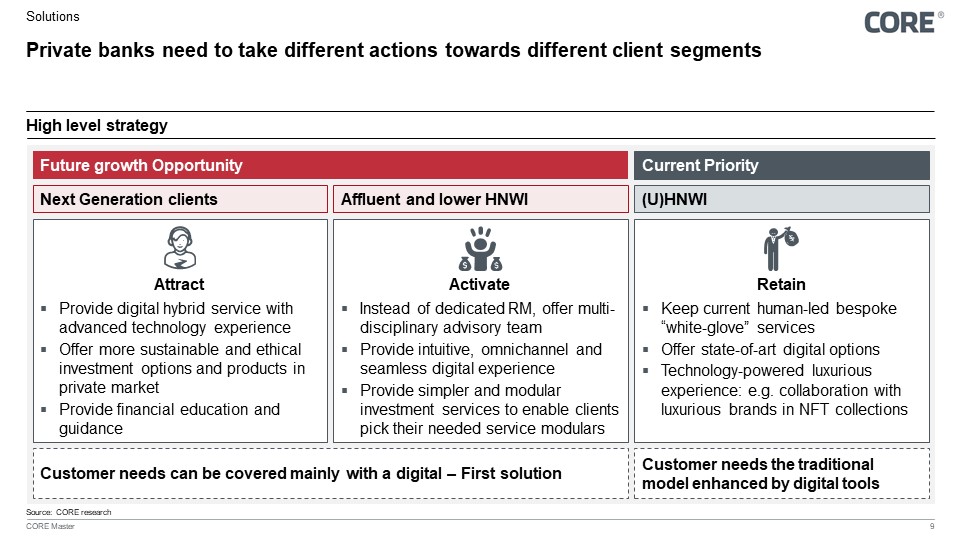

The high-level strategy: Attract – Activate – Retain

Wealth managers are navigating two essential priorities. Firstly, they must preserve their core clientele — High Net Worth Individuals (HNWIs) and Ultra High Net Worth Individuals (UHNWIs) — who expect and receive bespoke white-glove services. Maintaining this standard is crucial as it distinguishes wealth managers in a competitive market. Secondly, wealth managers must prepare for impending growth by engaging the next generation of clients and tapping into the potential of the 1-10 million EUR segment, which presents a substantial market opportunity.

To thrive within each segment, a tailored strategy is imperative. These strategies must align with the bank's unique positioning and the specific needs of its clients. While strategies will vary, this publication offers a high-level approach for addressing the key objectives of attracting, activating, and retaining clients across segments:

Figure 12: High level strategy

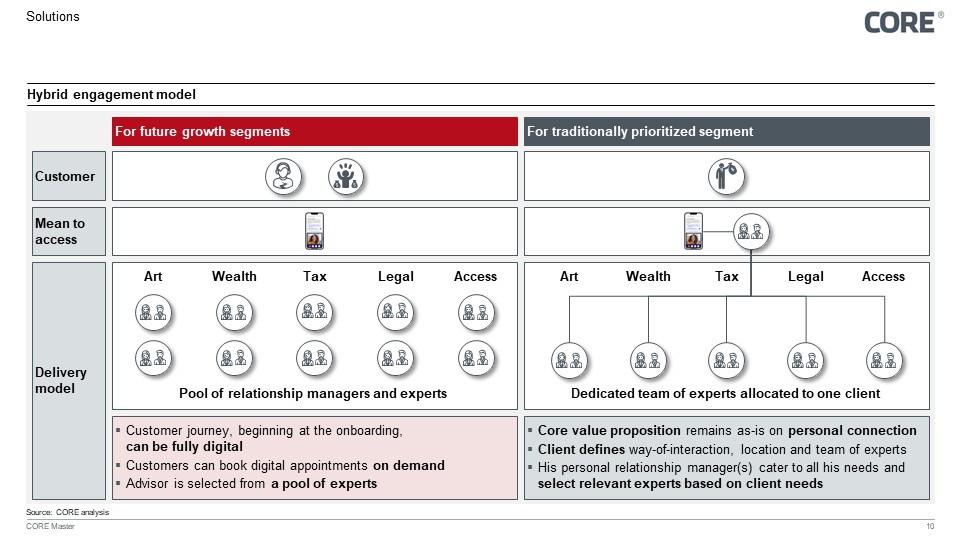

Hybrid engagement model for different client segments

Figure 13: Hybrid engagement model

Figure 13: Hybrid engagement model

A hybrid engagement model is a strategy that integrates traditional, human-driven advisory services with data-driven digital solutions to meet the diverse needs and preferences of various client segments. This model aims to capitalize on the strengths of both a high-touch relationship manager-led approach and a high-tech digital tool to effectively serve a broader range of clients and enhance their overall experience.

By applying varying degrees of digitalization tailored to different client segments, the hybrid engagement model empowers wealth management firms to strengthen their existing priorities while unlocking future growth opportunities.

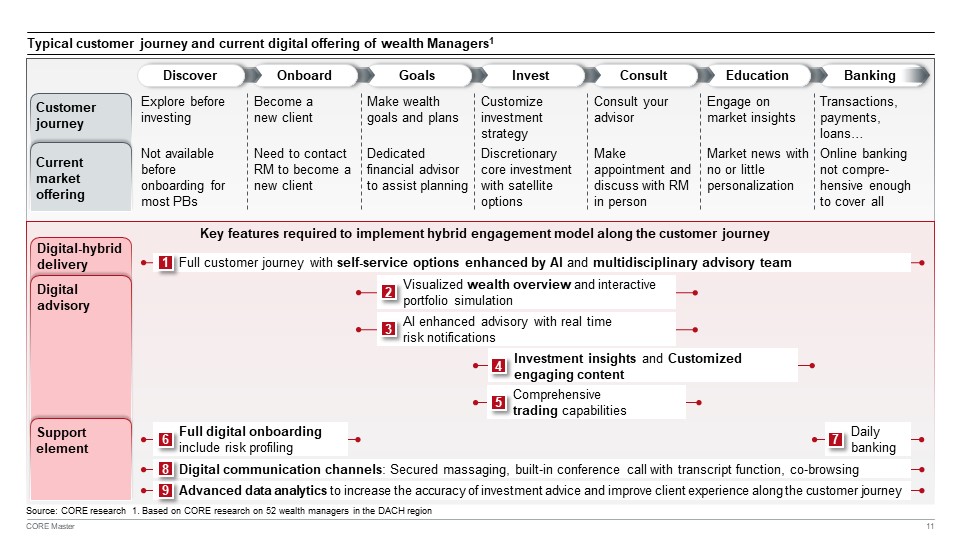

Key client experiences included in the hybrid engagement model

A comprehensive overview of the within the hybrid wealth management engagement model, highlighting the progression from initial exploration of the offering to the utilization of banking services.

Figure 14: Key features required to implement hybrid engagement model along the customer journey

Figure 14: Key features required to implement hybrid engagement model along the customer journey

From initial curiosity to dynamic wealth management, the hybrid engagement model guides clients through a seamless journey of financial discovery, planning, and growth. At every step, from intuitive onboarding to personalized investment strategies and diligent advisory support, clients are empowered to navigate their financial landscape with confidence. Engaging interactions and streamlined banking transactions further enrich the experience, ensuring that every aspect of wealth management is accessible, informed, and aligned with our clients’ ambitions.

Tackle the challenges

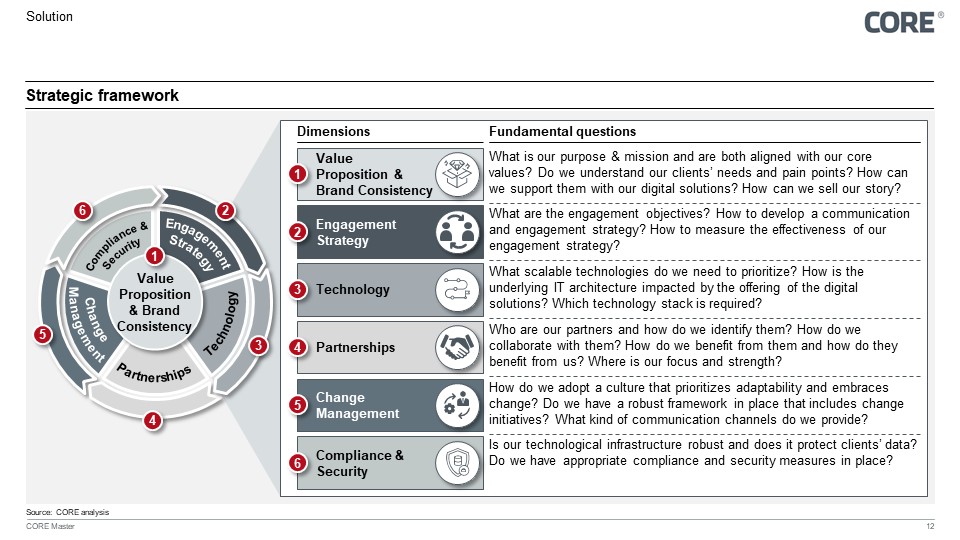

Expanding upon the challenges wealth managers face when adopting a hybrid engagement model, as detailed in the preceding chapter, this subsequent section provides insights on how to effectively address and overcome those previously outlined issues.

To navigate these obstacles and support wealth managers in integrating a hybrid engagement model, COREtransform has developed a proprietary framework including the following dimensions: Value proposition & brand consistency, client engagement strategy, technology & data, partnerships, change management, and compliance & security:

Figure 15: Strategic framework to tackle the challenges.

Figure 15: Strategic framework to tackle the challenges.

CORE has the privilege of supporting both mid-sized wealth managers and large banks on their digital transformation journey, from strategy to implementation. Our experience gives us a deep understanding of market trends, needs, challenges and potential obstacles on your upcoming transformative journey. As a trusted partner, EPAM provides CORE with a high degree of adaptability and management of their sophisticated technology transformations.

Our methodology commences by elucidating the goal and underscoring the significance of these dimensions. Subsequently, the requisite measures are detailed and concluded by outlining actionable steps and best practices.

Define clear value proposition to ensure brand consistency

A key strategic business objective is to establish a robust value proposition and maintain brand consistency to ensure a compelling presence. Coupling these elements produce a strong and memorable brand that resonates with well-informed customers.

To achieve brand consistency, a business must:

- Identify a clear purpose, mission, and aspirations aligned with core values such as integrity, trust, and expertise.

- Understand client needs, preferences, and challenges by conducting surveys or focus groups and segmenting target client groups accordingly.

- Blend technology with personalized services, including the development of comprehensive digital platforms and a digital advisory team, real-time notifications, and user-friendly interfaces for independent online transactions.

- Offer educational support for clients unfamiliar with digital tools, encouraging informed financial decisions.

- Communicate the unique value proposition and narrative to differentiate the brand from competitors.

- Collect and analyze client feedback to refine the value proposition and adapt services to ever-changing client needs.

Wealth managers need to formulate a value proposition that integrates high-tech and high-touch elements within a hybrid engagement model. This enables clients to choose their preferred mode of interaction and helps the brand to build trust and stand out in a competitive marketplace.

Develop a client engagement strategy

Creating a customized digital-hybrid experience is essential after identifying and segmenting clients. This engagement strategy, tailored to each client group's preferences, aims to bolster relationships.

Key elements of a successful engagement strategy involve:

- Establishing engagement Goals: Define clear objectives for the engagement strategy, such as increasing client retention rates or enhancing cross-selling opportunities.

- Designing a communication approach: Develop a communication strategy that fits both client expectations and the bank's strengths. This includes:

- Creating a balanced mix of digital and personal approaches, letting clients set their content and engagement options.

- Identifying essential channels, touchpoints, and ideal communication frequency for proper client interaction.

- Evaluating effectiveness: Consistently measure the success of engagement strategies, adapting based on feedback and obtained results, with metrics like client satisfaction and net promoter scores.

By following these steps, wealth managers can cultivate an effective, client-centric engagement strategy that encourages long-term loyalty and satisfaction.

Identify technology requirements and close the digital capabilities gap

The objective is to implement a range of digital solutions, both back-end and front-end, to boost scalability and client experience in wealth managers.

Achieving this target involves:

- IT Architecture & Infrastructure: Design an effective IT strategy that aligns with the business strategy. Assess existing infrastructure and consider transitioning to cloud services.

- Core and Surrounding Banking System: Implement a suitable core banking system like IMSplus, Extend, Wealth in One, or Altimis, known for strong integration capabilities. Implement and integrate surrounding systems such as compliance & risk management, investment & fund, and CRM systems seamlessly.

- Data Platform and Analytics: Build a compliant data platform to leverage customer data and provide personalized experiences. The platform should have strong analytical capabilities, ideally enhanced by AI.

- AI and Generative AI: Apply AI and GenAI for various functions. This might include enhancing customer engagement, identifying and converting prospective clients, enhancing visual interaction of portfolio simulations, creating smart chat bots, and strengthening robo-advisory capabilities.

- Multi-channel customer experience: Superior UI/UX design is vital for a premium customer feel in the digital space. Managing clients across multiple channels without information asymmetry requires real-time data processing capabilities.

Engaging in partnerships

When applying a hybrid engagement model, forming partnerships may be an effective strategy to access new technologies, tap into new markets, enhancing our ability to serve clients with more advanced digital solutions, while maintaining a focus on our primary areas of expertise.

To achieve this, the following steps must be considered:

- Identifying potential partners whose core values align with your private bank, ensuring a mutual benefit, through methods such as market analysis or research, attending industry conferences and networking events or by simply connecting with innovative startups, such as fintech incubators or accelerators, that are looking to collaborate with established financial institutions

- Once a suitable partner is identified, determining the most effective way to collaboratively serve the client base.

- Determine the division of responsibilities for each aspect of the service or product between the partners.

- Establish which areas to concentrate on your core strengths, where to utilize your expertise, and what to delegate to your partners.

Partnerships are vital as they allow for the sharing of risks and expenses, maintaining a competitive edge in the fast-changing financial sector, capitalizing on combined expertise, and accelerating innovation

Navigating through change

Change management is critical in wealth management to stay agile, meet evolving client needs and respond flexibly to global financial landscape changes.

To manage change efficiently, wealth managers should consider steps like:

- Fostering a Culture of Adaptability: Embrace a culture that values adaptability, resilience, and continuous learning across all levels in the organization. This could involve leadership demonstrating commitment to new platforms and conducting regular training sessions.

- Implementing a Robust Framework: Use a robust framework for assessing, planning and executing change initiatives. This ensures alignment with broader business objectives. For instance, establish a structured approach to integrate digital assets into the bank's offering that includes market analysis, risk assessment, compliance checks, and clear guidelines for advising clients

- Effective Communication Channels: Provide efficient communication channels for information dissemination and feedback collection. This could involve establishing a communication plan, detailing how changes are communicated to clients and staff, and how feedback is gathered to refine the system.

By utilizing efficient change management tools and methodologies alongside fostering an agile culture, wealth managers can navigate through changes more effectively. This will aid in the successful transition to a hybrid engagement model that best serves their diverse client segments.

Applying compliance measures and mitigating data privacy concerns

In the digital-centered, hybrid engagement model, data security and privacy are critical. The aim is to safeguard sensitive client information and adhere to regulatory standards to prevent financial misconduct and breaches.

The following essentials should be addressed for data protection and compliance:

• Robust Technological Infrastructure: Implement a secure, advanced technological infrastructure that can defend against threats through data encryption, multi-factor authentication, and robust firewalls.

- Regular Audits: Perform both internal and external audits to ensure continuous adherence to data protection measures and identify areas of improvement.

- Cultural Emphasis on Data Privacy: Promote an organizational culture prioritizing data privacy with staff training in technical and ethical aspects of data protection.

- Access Controls: Establish strict access controls and authentication methods to limit data access to authorized personnel.

- Incident Response Plan: Develop a detailed incident response plan to address data breaches or security incidents promptly and effectively.

- Vendor Due Diligence: Conduct due diligence on third-party vendors and service providers to ensure their adherence to robust data privacy and security standards.

Clients should also play an active role in protecting their data through strong passwords, multi-factor authentication, and awareness of cybersecurity best practices. Blockchain technology can further enhance security.

Stringent compliance measures combined with proactive client engagement can effectively mitigate data privacy concerns, creating a secure digital environment aligned with regulatory requirements.

Conclusion

In conclusion, the wealth management sector is undergoing significant changes. The increasing pressure on profit margins, the impending intergenerational wealth transfer, and the rise of technology are reshaping the market. The traditional 'white glove service' is proving to be costly and not scalable enough to cater to the new customer segments.

The future of wealth management lies in successfully integrating high-tech and high-touch elements within a hybrid engagement model, creating a customized digital-hybrid experience tailored to each client group's preferences.

However, Wealth managers are facing challenges to adopt the hybrid engagement model in strategical, technological, financial, organizational, regulatory levels. To navigate these challenges, CORE provides a strategic framework that will empower wealth managers to navigate market shifts and continue to thrive in the evolving financial landscape.

Questions? Speak to our experts

Expert EN - Sihan Huang

Sihan Huang is a Senior Consultant at CORE and holds a Grande École degree at HEC Paris and B.Sc. in Information Systems. She has project experience on business strategy, operating model, digital ...

Read moreSihan Huang is a Senior Consultant at CORE and holds a Grande École degree at HEC Paris and B.Sc. in Information Systems. She has project experience on business strategy, operating model, digital transformation in various sectors including banking, insurance, retail, gaming, logistics, hospitality, and automotive. Her current focus is wealth management and green finance

Read less