Regulation of financial instruments – BaFin workshop on the status quo and implementation of MiFID II/MiFIR

KEY FACTS

-

BaFin workshop on implementing MiFID II/MiFIR held on February 16, 2017

-

The Second Financial Market Amendment Act (FiMaNoG II) heightens requirements on the transparency of reporting as of 2018

-

Regulatory requirements for data providers to be extended

-

Numerous unanswered questions remain for market infrastructure operators

-

Review of IT infrastructures needed for regulatory compliance

REPORT

Financial instruments such as securities, derivatives (warrants) and money market instruments are frequently used by firms and investors today for asset, liquidity and risk management. As was made crystal clear by the financial crisis of 2008, these instruments can be useful for risk management, but if used in the wrong way, they can also have a destabilizing effect on financial markets. Financial instruments are therefore quite rightly subject to greater critical scrutiny from the public and from regulators. The latter have produced a series of rules (especially EMIR, MiFID II, MAR, CRD IV and PRIIP) in order to ensure the stability of financial markets on the one hand and to protect consumers on the other.

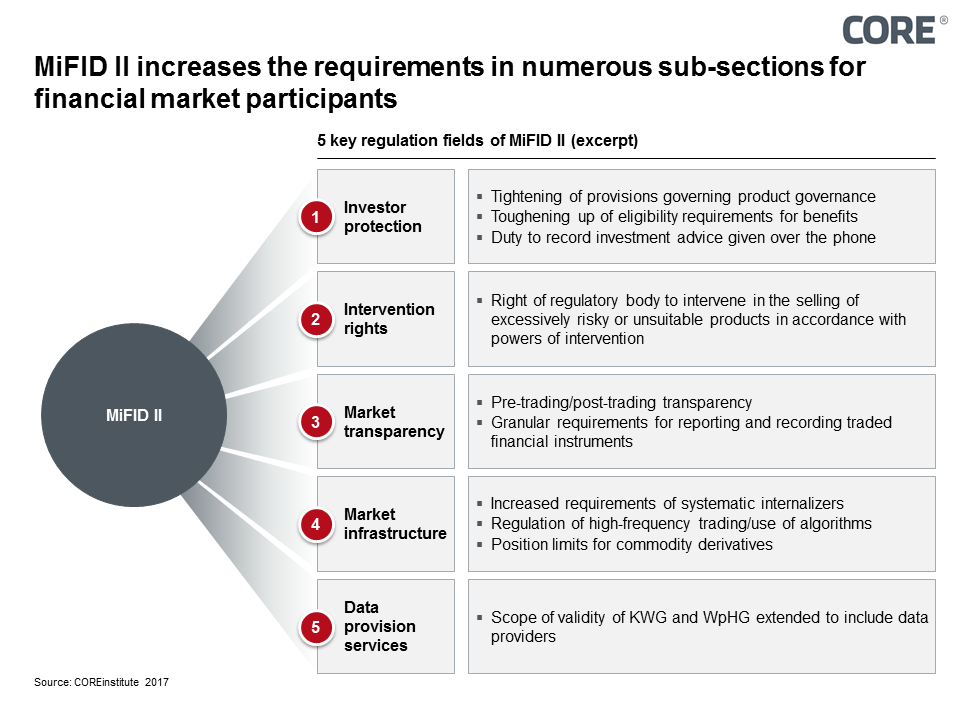

Fig 1: Overview of key regulatory fields of MiFID II

On February 16, 2017, BaFin held a workshop in Frankfurt on topics of the new regulation and directive concerning markets in financial instruments (MiFID II/MiFIR), notably market infrastructure and transparency, which was attended by more than 400 delegates. The aim of the workshop was to explain the current status of implementing MiFID II and to enter into a dialogue with participants from the German financial market. MiFID II will apply throughout the EU once the Second Financial Market Amendment Act, for which a white paper was published in December 2016, comes into force.

After delegates were welcomed by the executive director, Ms Roegele, Carsten Ostermann of the European Securities and Markets Authority (ESMA) began by giving an outline of further plans for the implementation of MiFID II. He emphasized that after a delay of one year, MiFID II would now come into force on January 3, 2018. He said that as well as producing guidelines, ESMA would offer support to financial market participants in the form of Q&A forums on the numerous aspects of detailed implementation that still remain unanswered.

He then went on to say that the prospect of Brexit was creating considerable uncertainty in regulatory matters. It remains to be seen whether it will still be possible in future to do business in London on the same terms, with the same rights as the city currently enjoys.

The requirements that MiFID II will place on financial market participants follow what is now a familiar pattern. Requirements for relevant market participants such as systematic internalizers will be substantially intensified. In addition, financial market participants will be required to submit numerous records to the regulatory bodies, in some cases at a much greater level of detail.

A cornerstone of this is the central recording of data on all financial instruments relevant to MiFID II through the Financial Instruments Reference Data System (FIRDS). This involves a central database of all financial instruments with 48 fields. This database will be available to the public free of charge. Consideration is being given to delegating this project to the national authorities, who would have responsibility for this.

Besides these detailed reporting obligations, financial market participants are faced with more extensive controlling and monitoring responsibilities. In addition to the more rigorous definition of systematic internalizers and the ensuing monitoring obligations, the requirement to stay within the position limit for commodity derivatives will call for greater attentiveness on the part of those financial market participants involved.

In line with the particular significance of data for the financial market, data providers will, in future, also be included in the scope of the German Banking Act (KWG) and the Securities Trading Act (WpHG). This will result in, most notably, data providers being subject to the existing organizational requirements for securities firms and securities service companies.

Conclusion

The topics discussed above illustrate that the public perception of MiFID II is focused on consumer protection. However, these guidelines will also lead to a considerable increase in regulatory requirements for reporting and monitoring processes. Financial services companies as well as financial institutions themselves are now clearly faced with the challenge of auditing their IT infrastructure and data processing systems to check their compliance with regulations and their performance. This raises the prospect of pre-existing contracts for the outsourcing of IT services becoming less competitive for financial institutions than more recent proposals making more use of technological progress to improve efficiency.

For example, cloud and container structures will go a long way towards making up for the growth in costs which can be expected. Another aspect to be dealt with will be the exponential increase in volume of granular data, and modern NoSQL concepts seem likely to offer affordable solutions here.

As regards future reporting and recording requirements, financial market participants should ask themselves whether these increased requirements can be met more efficiently by applying API interfaces, insofar as reporting system projects have not been finalized and IT architectural principles laid down.

SOURCES

https://www.bafin.de/SharedDocs/Veranstaltungen/DE/170216_workshop_MiFIDII_MiFIR.html

Meet our authors

Expert En - Artur Burgardt

Artur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment ...

Read moreArtur Burgardt is Managing Partner at CORE. He focuses, among other things, on the conceptual design and implementation of digital products. His focus is on identity management, innovative payment and banking products, modern technologies / technical standards, architecture conceptualisation and their use in complex heterogeneous system environments.

Read less