EU Retail Banking Trends 2026

Retail Banking at the Efficiency Wall: How Banks Can Rebuild Profitability, Relevance, and Trust by 2026

Key Facts

- The interest-rate uplift from 2022-2024 temporarily masked structural inefficiencies; as rates normalize, rigid cost bases and limited pricing power are re-exposing underlying margin compression

- European retail banks are approaching an efficiency wall where incremental cost reduction within existing operating models no longer restores operating leverage

- AI has moved from experimentation to expectation, yet most institutions struggle to industrialize execution at enterprise scale, limiting measurable productivity impact

- Legacy complexity, sovereignty constraints, and regulatory requirements increasingly shape technology architecture and operating models, embedding resilience and compliance as design parameters rather than overlay functions

- In a system defined by reinforcing structural pressures, banks can no longer optimize all dimensions simultaneously; leadership requires an explicit strategic prioritization and deliberate orchestration of trade-offs

The End of the Cyclical Tailwind Illusion

For much of the past decade, European retail banking operated under persistent structural pressure. Between 2015 and 2021, prolonged low and negative interest rates compressed net interest margins, while operating costs continued to rise due to regulation, technology modernization, and labor inflation. Revenue attrition consistently outpaced cost-mitigation efforts.

Banks responded with branch closures, offshoring initiatives, and digitalization programs. While these measures slowed cost growth, they largely stabilized rather than structurally reduced operating expenses. Fixed costs remained elevated, and organizational and technological complexity continued to accumulate. Profitability was weak, and management attention focused on defensive efficiency programs aimed at stabilizing results rather than fundamentally reshaping the cost base.

This dynamic changed abruptly between 2022 and 2024. Rapid interest rate hikes by the European Central Bank (ECB) created an extraordinary, but temporary, uplift in net interest income. Across most Euro area markets, margins expanded faster than operating costs, driving record profitability and restoring headline financial ratios to levels not seen in more than a decade.

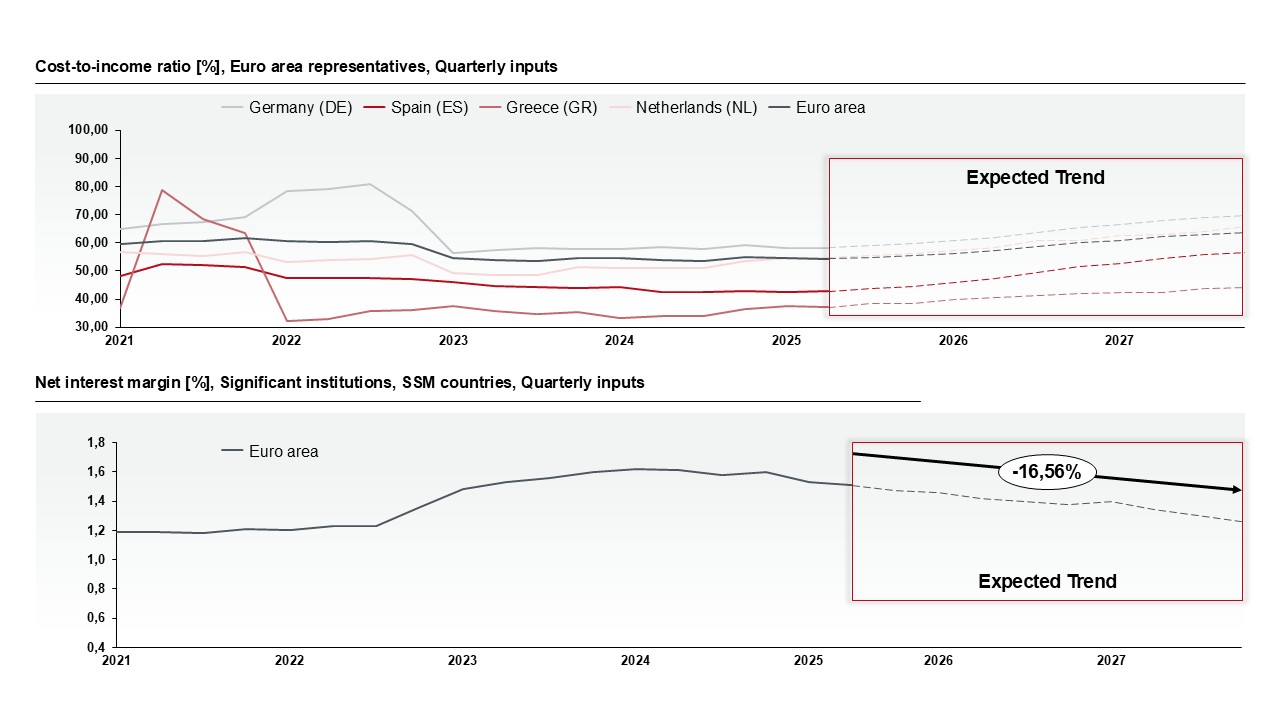

Figure 1: Illustration of selected Cost-to-income ratio and Net interest margin within the European retail banking market representing the revenue upwind

Figure 1: Illustration of selected Cost-to-income ratio and Net interest margin within the European retail banking market representing the revenue upwind

As illustrated in Figure 1, net interest margins across major Euro area markets expanded materially between 2022 and 2024, reaching peak levels not observed in more than a decade. However, forward projections indicate a normalization of margins of approximately 15–17% from peak levels as interest rates stabilize. At the same time, operating expenses remain structurally elevated and continue trending upward, reflecting regulatory mandates, IT modernization programs, cyber resilience investments, and sustained wage inflation. The expected trajectory shows cost-to-income ratios beginning to deteriorate again from 2025 onward, reversing part of the temporary cyclical improvement.

As interest rates normalize, the underlying imbalance becomes fully visible. Revenues flatten or decline modestly, while operating costs remain largely inflexible in the short to medium term. Every structural inefficiency now directly translates into margin pressure. Personnel costs, regulatory obligations, cyber and resilience investments, and run-the-bank IT spending cannot be reduced quickly without fundamental changes to operating models.

The result is a classic scissors effect: revenues normalize while costs remain rigid, compressing margins and exposing inefficiencies that were previously masked by cyclical tailwinds.

Unlike previous downturns, several structural factors make cost discipline a permanent strategic constraint rather than a cyclical adjustment. Cost structures have shifted decisively toward fixed and semi-fixed components, driven by higher run-the-bank IT spending, regulatory compliance programs, cyber resilience investments, and sustained wage inflation. Prior optimization waves have already harvested the most accessible efficiency gains, leaving only structurally harder trade-offs. At the same time, competitive dynamics limit banks’ ability to pass rising costs on to customers.

In this environment, revenue growth no longer compensates for inefficiency. Every structural weakness now hits the P&L directly.

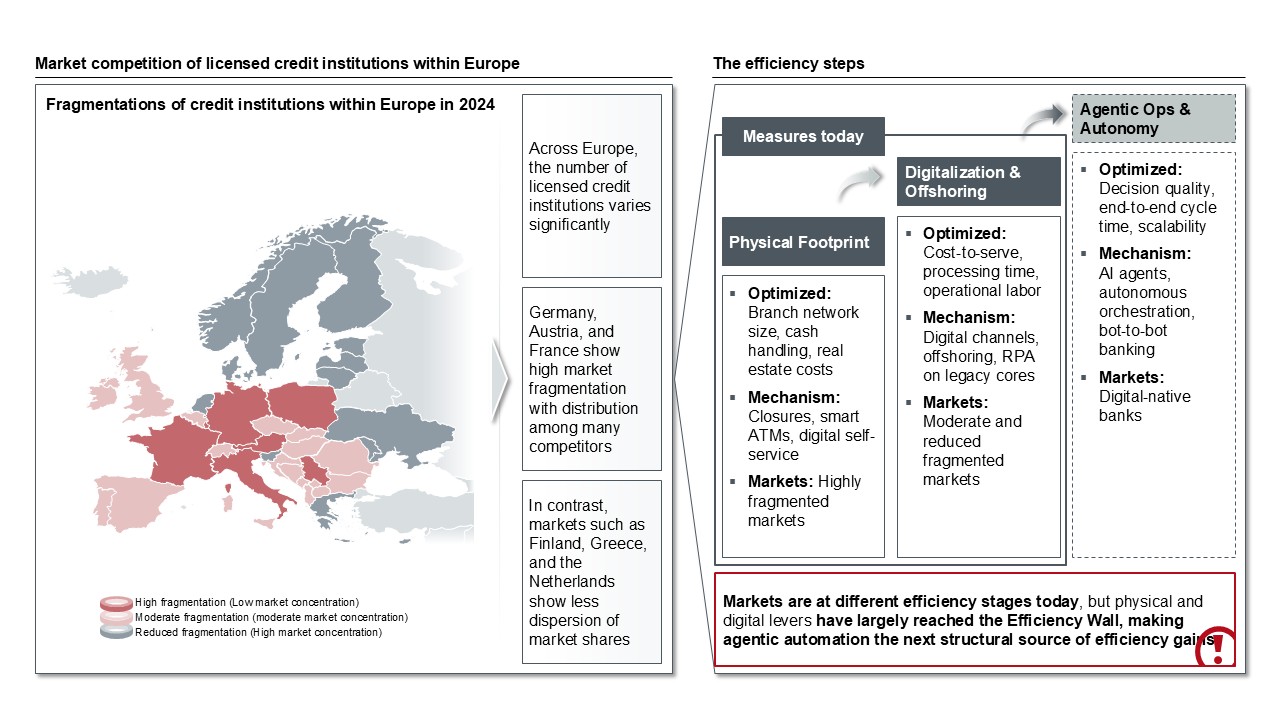

Figure 2: Fragmentation of the European retail banking market and derived efficiency steps to enhance profitability

This creates a fundamental shift in the strategic agenda for European retail banks. Efficiency is no longer about optimizing within existing complexity. It is about confronting the structural limits of operating models that were initially designed for stability, control, and incremental change - not for speed, scalability, and automation at enterprise level.

The implication is straightforward. European retail banking is moving into a phase where incremental optimization no longer restores operating leverage. The industry is approaching an efficiency wall; a point at which further cost reduction within the current model delivers diminishing financial returns while gradually eroding agility and resilience.

This is the context in which today’s strategic challenges must be understood. What once appeared as a cyclical profitability challenge has become a structural operating model constraint. As internal efficiency gains stall, external pressures continue to accelerate. Customer expectations rise, AI shifts from experimentation to execution, regulatory and cyber requirements harden into architectural constraints, and legacy platforms increasingly constrain both delivery speed and organizational adaptability.

Rising Customer Expectations and the Relevance Gap

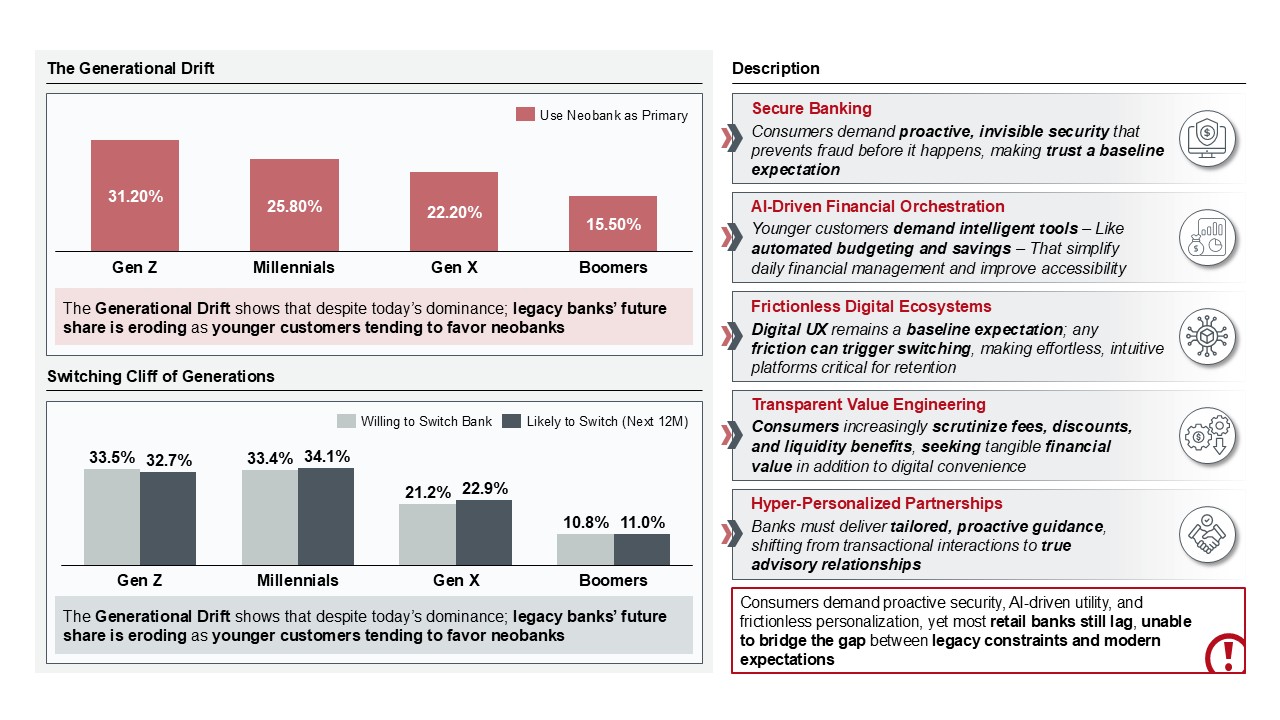

External pressure is not only driven by competition within the retail banking sector, but increasingly by customer demand. Consumer data shows a pronounced generational shift: more than 30% of Gen Z and Millennials already use neobanks as their primary bank, compared to around 15% among Baby Boomers. At the same time, younger generations are up to three times more likely to switch banks within the next 12 months. This signals not just temporary dissatisfaction but a structural erosion of customer stickiness. Now more than ever retail banks must focus on customer Expectations as they have also shifted structurally:

- Proactive, invisible security,

- AI-driven financial orchestration,

- frictionless digital journeys,

- transparent pricing,

- and hyper-personalized guidance

are now baseline requirements rather than differentiators. The competitive threshold has shifted from product provision to continuous, data-driven financial orchestration. Most incumbent banks struggle to meet these expectations consistently, as legacy platforms, fragmented data, and slow delivery cycles limit their ability to adapt at the pace customers increasingly expect. The constraint is not awareness but structural delivery capacity.

Figure 3: Generational shift in primary banking relationships and switching propensity

Figure 3: Generational shift in primary banking relationships and switching propensity

These shifts in customer expectations are not occurring in a vacuum. BigTech and FinTech players are systematically capitalizing on them. Built on platform-based, data-driven operating models, they are able to translate customer signals into new features and services within weeks rather than years. Rapid release cycles, open ecosystems, and direct ownership of the customer interface allow them to continuously refine propositions, embed banking into broader digital journeys, and set new benchmarks for speed and experience. This creates a compounding relevance advantage: faster iteration improves customer data, which in turn enables more targeted propositions. Coupled with the elevating switching propensity of younger generations this indicates that, over the coming years, customer growth will increasingly accrue to providers with the most relevant and consistently improving offerings - capabilities that are currently characteristic of BigTech and FinTech players rather than of incumbent retail banks. The emerging relevance gap is therefore not cyclical but structural and are rooted in differences in architecture, data integration, and execution speed.

Figure 4: Comparison of Feature shipping between BigTech/Fintech and Retail Banks

Figure 4: Comparison of Feature shipping between BigTech/Fintech and Retail Banks

The Structural Forces Reshaping European Retail Banking

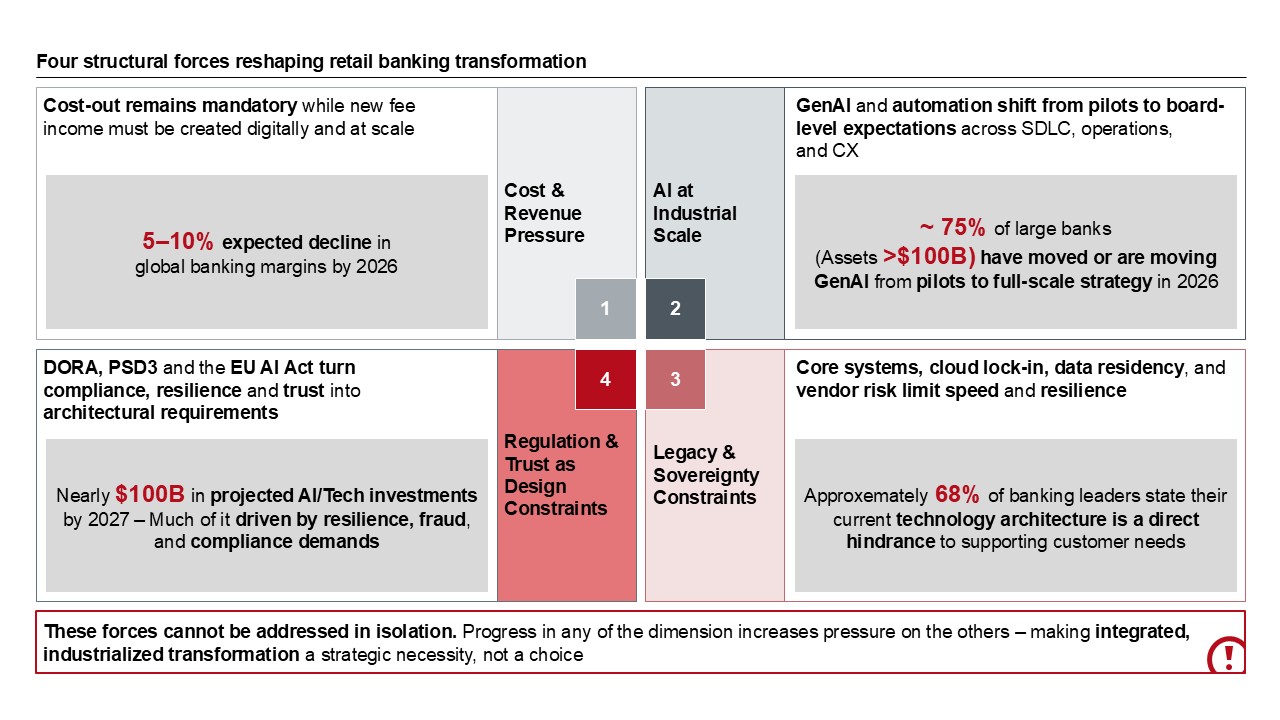

The challenges and external pressures described above do not act in isolation. They are reinforced by a set of structural forces that increasingly define the economic reality of European retail banking. Individually, none of these forces are new. What is new is their simultaneity - and the way they amplify one another. Their interaction creates systemic pressure rather than isolated challenges. Four structural forces are particularly relevant:

- Cost & Revenue Pressure

- AI at Industrial Scale

- Legacy & Sovereignty Constraints

- Regulation & Trust as Design Constraints

Together, these forces place retail banks in a situation where progress in one dimension frequently increases pressure in another. The resulting dynamic resembles a closed pressure system: local optimization often increases global complexity. Cost-reduction initiatives collide with regulatory and resilience requirements. Faster delivery heightens cyber and operational risk exposure. AI initiatives struggle to scale due to fragmented architectures and governance. Rather than reinforcing transformation, these dynamics frequently offset each other, limiting measurable structural progress.

Figure 5: Four Forces reshaping the European retail banking landscape

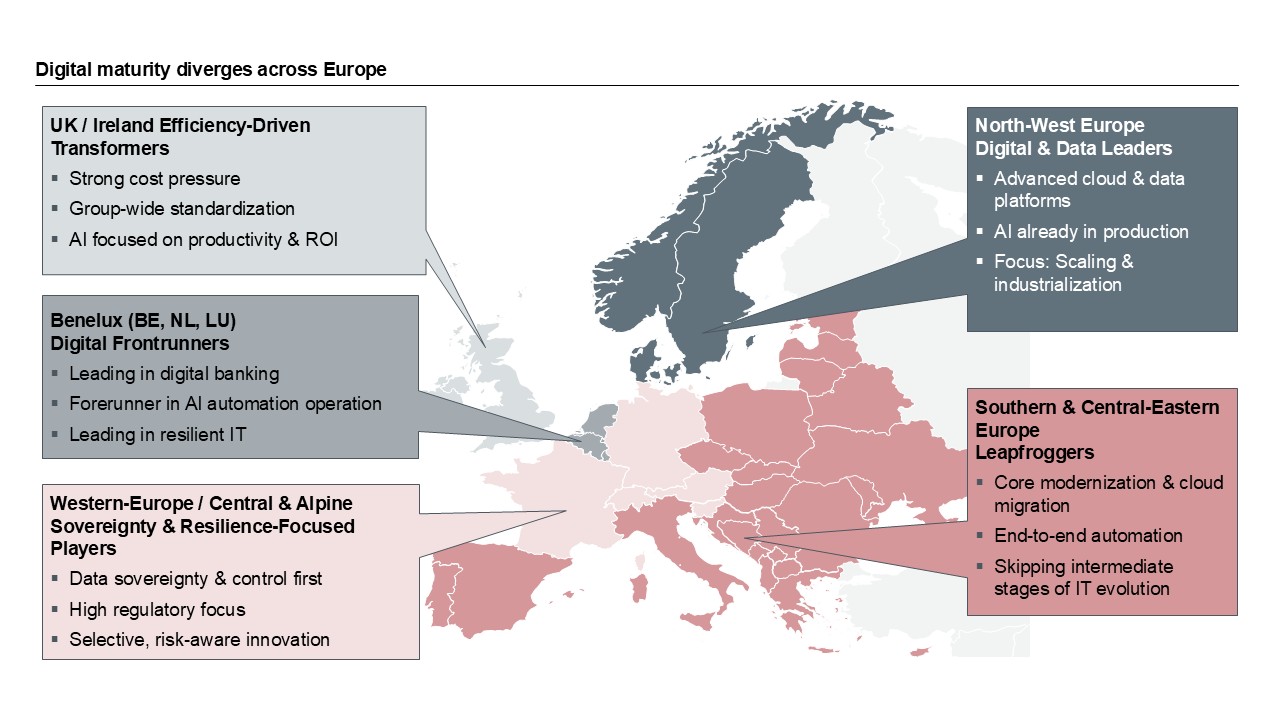

However, the impact of these forces varies significantly across markets. Differences in digital maturity, legacy depth, regulatory intensity, and competitive dynamics mean that European retail banks face the same structural pressures from very different starting positions. As a result, the magnitude, urgency, and sequencing of required actions differ materially by country and by institution. There is no uniform European baseline - and therefore no universal transformation blueprint. Strategies that ignore starting position and regulatory intensity risk increasing complexity without restoring leverage. Effective responses must be tailored to local market conditions and the specific maturity profile of each bank, rather than applied as standardized, one-size-fits-all solutions.

Figure 6: Diverging digital maturity levels of retail banks within Europe

To understand how these differences translate into concrete strategic challenges, it is necessary to examine each force in more detail. The first and most immediately visible manifestation is cost and revenue pressure.

Fore 1: Cost & Revenue Pressure

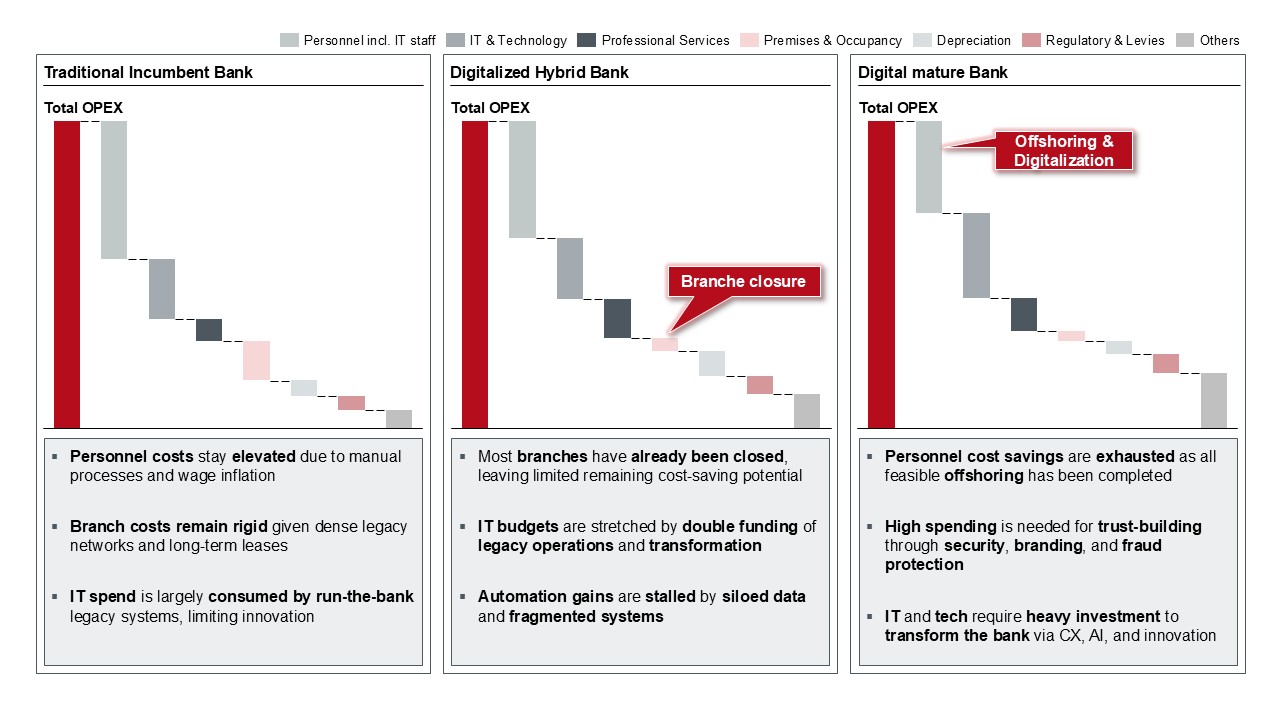

Structural cost discipline becomes unavoidable as banks progress along the digital maturity curve. However, the composition and accessibility of cost levers shift materially across stages.

In traditional incumbent models, operating expenditure is heavily concentrated in personnel-intensive processes, extensive branch networks, and legacy run-the-bank IT. Although structural cost reduction potential exists, the cost base is characterized by high fixed components and organizational rigidity. Consequently, short-term cost flexibility remains limited, while earnings become increasingly sensitive to revenue volatility.

In digitally hybrid banks, many traditional efficiency levers (particularly branch reduction and workforce optimization) have already been partially activated. Yet the parallel funding of legacy infrastructure and transformation initiatives constrains IT budgets and delays automation benefits. This creates a structural investment tension: modernization requires upfront capital before legacy cost layers can be structurally dismantled.

In digitally mature banks, classical structural savings are largely exhausted. The cost base shifts toward sustained investment in technology architecture, cybersecurity, regulatory resilience, and customer experience capabilities. At this stage, efficiency gains no longer stem primarily from cost cutting, but from scalable digital productivity and operating model optimization.

Figure 7: Cost allocation based on diverging digital maturity levels (Disclaimer: Figures and chart proportions are indicative and intended for illustrative purposes of cost composition shifts only; they do not represent absolute values or scale)

Figure 7: Cost allocation based on diverging digital maturity levels (Disclaimer: Figures and chart proportions are indicative and intended for illustrative purposes of cost composition shifts only; they do not represent absolute values or scale)

As a result, restoring operating leverage can no longer rely on incremental cost reduction. Instead, restoring operating leverage requires a structural shift. By moving from task-level automation to AI-driven, end-to-end orchestration, banks can improve decision quality, reduce cycle times, and achieve scalable cost efficiency - mirroring the operating models of digital-native players and enabling scalable operating leverage beyond linear headcount productivity.

Force 2: AI at Industrial Scale

In theory, AI-enabled automation, autonomous decisioning, and end-to-end orchestration should allow banks to scale efficiency beyond what incremental process optimization can deliver. In practice, however, this theoretical leverage has not translated into structural productivity gains.

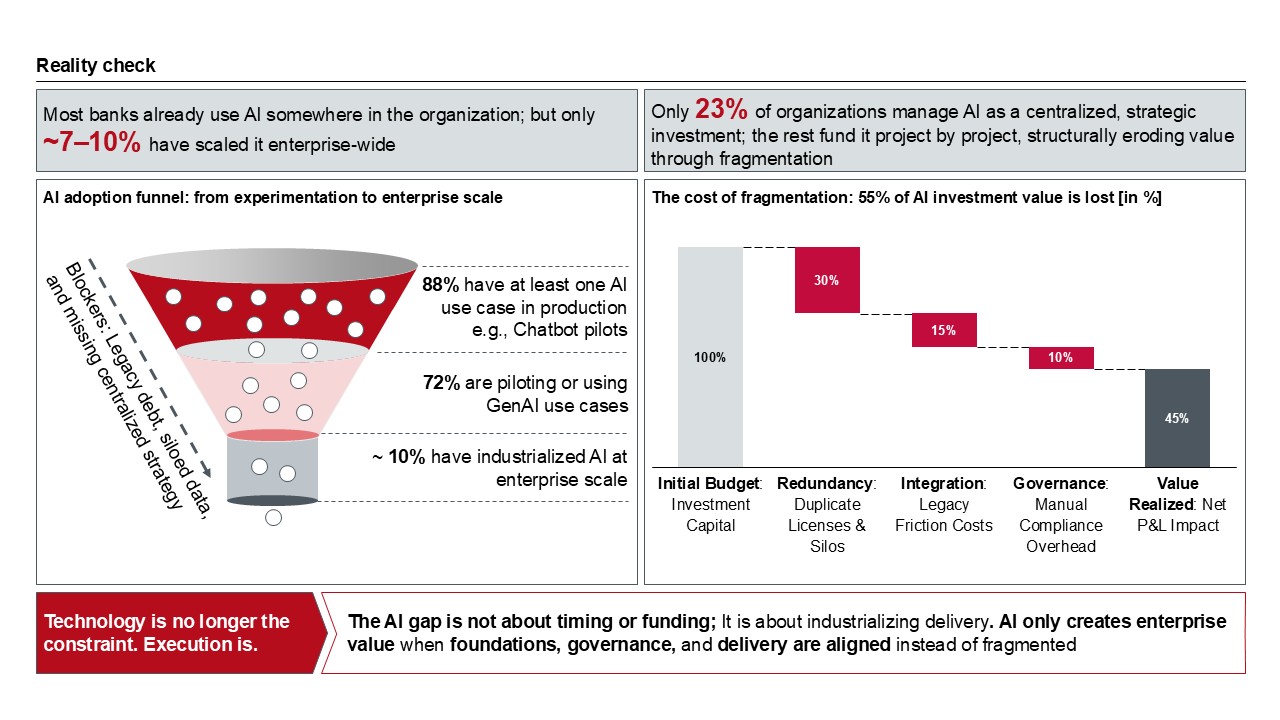

Instead of industrialized execution, 2025 remains characterized by extensive experimentation. Most retail banks have launched multiple AI initiatives and placed AI firmly on the strategic agenda. Yet, as the funnel below illustrates, only a small fraction has succeeded in translating pilots and isolated use cases into enterprise-wide capabilities with measurable P&L impact. The gap between experimentation and enterprise impact remains the central execution bottleneck. The constraint is no longer access to technology or funding, but the ability to execute AI at scale.

Figure 8: AI adoption of uses cases on enterprise scale

A significant share of AI investment value in 2025 was lost through fragmented delivery, duplicated tooling, integration friction, and manual governance overhead. As a result, AI initiatives often increase cost and complexity faster than they improve productivity. While individual use cases may deliver local benefits, their cumulative impact on productivity, speed, and cost efficiency remains limited. Without centralized governance, standardized tooling, and enterprise-level value tracking, these gains fail to compound. As AI initiatives proliferate without a coherent execution model, costs increase faster than value realization, and confidence in AI as a transformative lever erodes.

Fully capturing the potential of AI requires a structural shift: from decentralized experimentation to industrialized, enterprise-wide execution. Only when AI delivery, governance, and value tracking are aligned at enterprise level can AI move from an additive capability to a structural driver of productivity and operating leverage for European retail banks. Otherwise, AI remains an incremental enhancement layered onto an already complex operating model.

Force 3: Legacy & Sovereignty Constraints

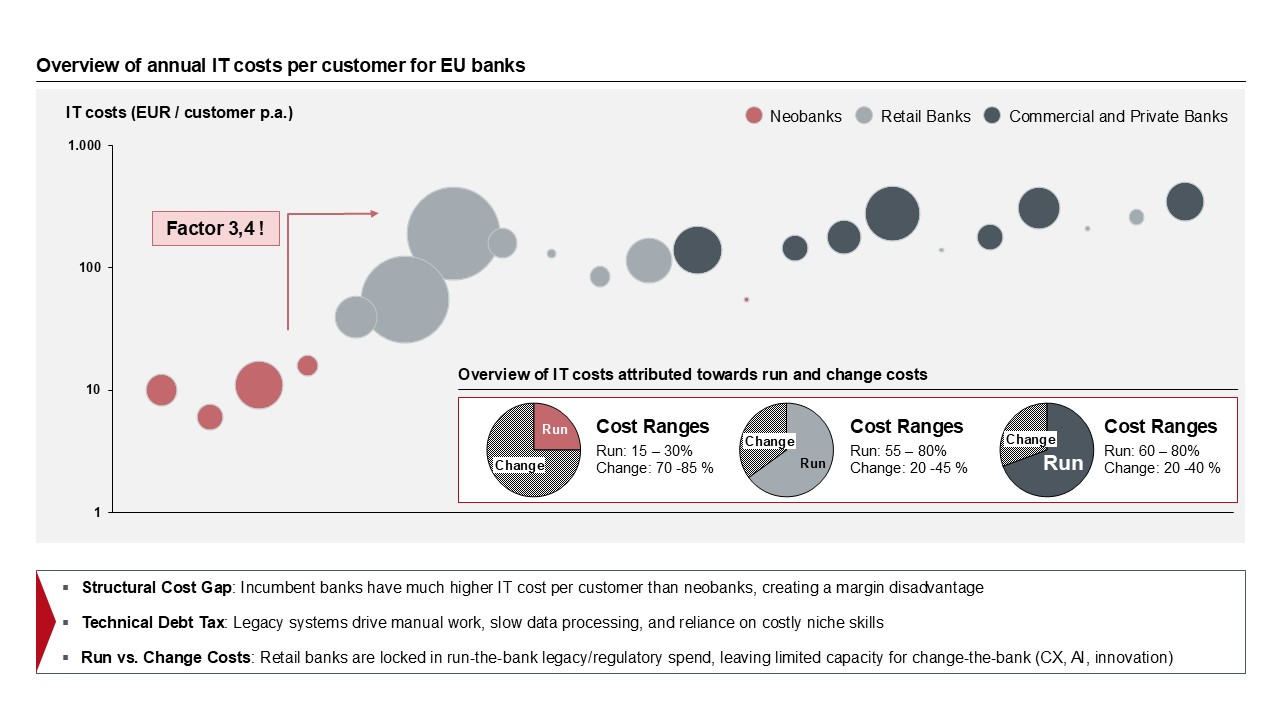

The limitations of AI execution are not solely a matter of delivery and governance. They are rooted in architectural fragmentation and structurally high run-the-bank cost ratios. For many incumbent banks, legacy systems continue to drive high IT costs per customer and extensive manual effort across core processes, constraining both speed and scalability. These structural inefficiencies not only dilute AI productivity gains but also absorb the investment capacity required to industrialize AI at enterprise level. Incumbent retail banks exhibit materially higher IT costs per customer than Neobanks, driven primarily by run-the-bank spending on legacy platforms and manual processes. This differential directly constraints pricing flexibility and investment capacity.

The concentration of spend on maintenance and compliance, rather than change and innovation, constrains scalability and leaves limited financial and organizational capacity for broader modernization initiatives.

Figure 9: Overview of annual IT costs per customer for selected EU banks and attribution of costs (Based on annual reports)

Figure 9: Overview of annual IT costs per customer for selected EU banks and attribution of costs (Based on annual reports)

Banks that have advanced further in their technological transformation face a different but equally material set of constraints. While cloud migration and platform modernization reduce legacy operating costs, they introduce a dependency shift toward a small number of hyperscale providers. This “dependency flip” creates new challenges around data sovereignty, vendor lock-in, and regulatory compliance, particularly under increasingly stringent regulatory requirements such as e.g. DORA. The shift replaces internal legacy rigidity with external platform dependency.

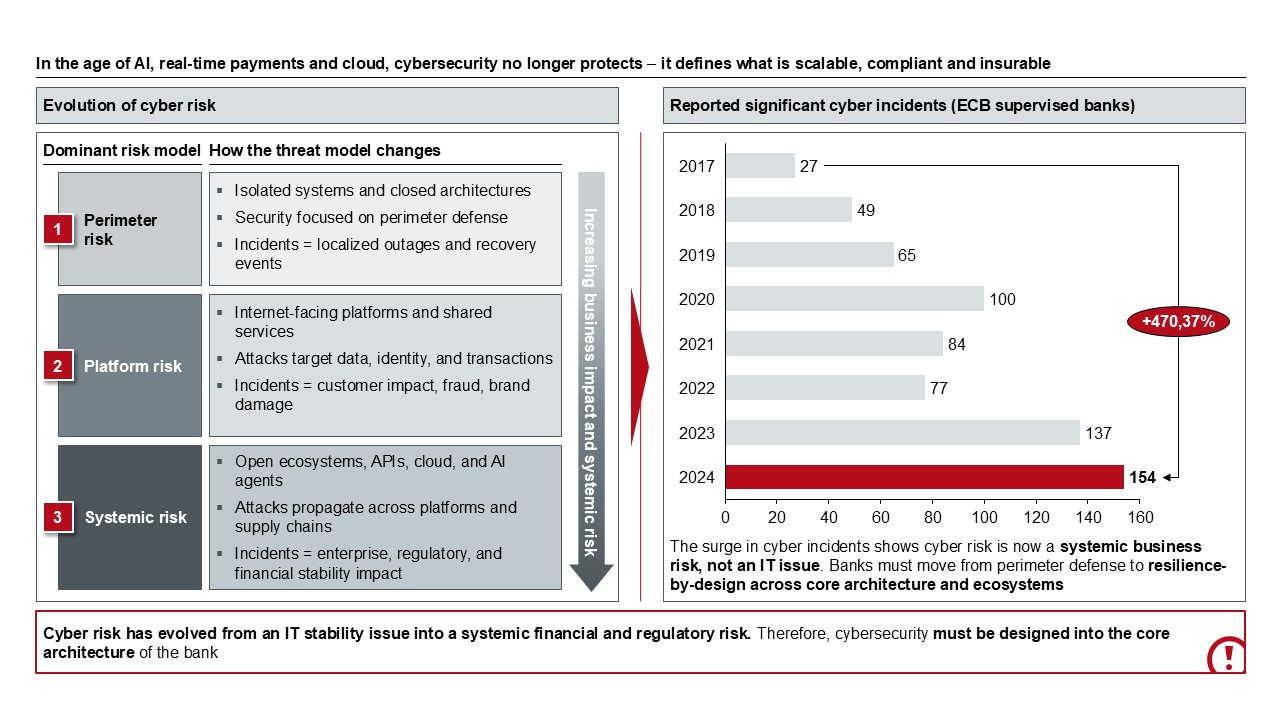

Even where geopolitical and sovereignty risks are explicitly addressed in transformation programs, a further constraint emerges. The shift from largely self-contained, on-premise systems to highly interconnected cloud platforms and open-banking ecosystems fundamentally changes the risk profile of retail banking. As manual, locally controlled processes are replaced by real-time integrations, APIs, and shared services, operational dependencies increase and failure modes propagate more easily across systems and institutions.

In this environment, cyber risk evolves from a localized IT concern into a systemic business and regulatory risk. The probability of localized incidents may decline, but the impact of systemic failures increases. The growing number and severity of cyber incidents, as illustrated, reflect this structural shift. Rising attack volumes, coupled with greater interconnectivity, significantly increase the likelihood and impact of outages; elevating cyber security to a core design and management priority for banks undergoing transformation.

Figure 10: Evolution of cyber security risks and ECB supervised incidents

Figure 10: Evolution of cyber security risks and ECB supervised incidents

The consequences of this shift are material and immediate. As outage duration and incident severity increase, regulatory penalties escalate rapidly. Beyond fines, prolonged outages directly affect customer retention, funding perception, and long-term valuation. At the same time, data breaches and prolonged service disruptions risk permanent erosion of customer trust, with long-term implications for brand and market position. Beyond regulatory and reputational impact, cyber incidents also trigger substantial operational recovery costs, as systems must be restored, vulnerabilities remediated, and resilience gaps closed. Together, these effects reinforce cyber security as a core business risk that directly influences financial performance, customer retention, and strategic flexibility.

What becomes visible at this point is that cyber risk is not an isolated phenomenon. It is the most tangible expression of a broader structural shift: regulation and trust are no longer external constraints that can be managed through incremental controls or downstream compliance. They determine architectural degrees of freedom.

Force 4: Regulation & Trust as Design Constraints

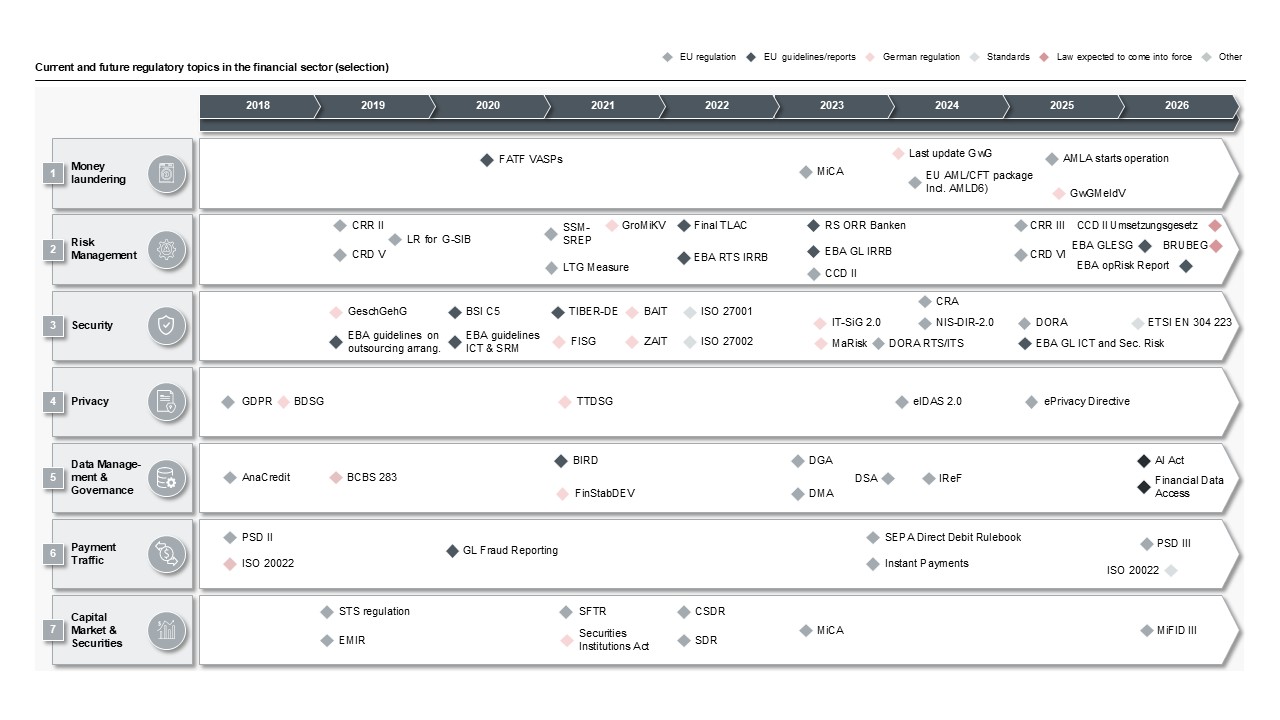

Across Europe, regulatory intent is clear. Supervisors and legislators aim to strengthen the resilience of critical banking services, protect consumers, safeguard financial stability, and reduce systemic and geopolitical risk. Frameworks such as DORA, PSD3, the EU AI Act, and evolving AML/KYC regimes reflect this ambition and respond to the growing complexity and interconnectedness of modern banking. These frameworks reflect not incremental supervision but structural risk redefinition.

At the same time, today’s regulatory burden is not the result of recent policy alone. It is the cumulative outcome of the post-financial-crisis response, during which stability, control, and risk containment rightly took precedence over efficiency and simplicity. Over more than a decade, successive regulatory waves were implemented rapidly, often in parallel and in isolation. While effective in stabilizing the system, they left banks with deeply layered processes, fragmented control environments, and structurally elevated compliance costs. Each regulatory wave solved a stability problem while incrementally increasing structural complexity.

Figure 11: Insights into a selection of current and future regulatory requirements in the financial sector

Figure 11: Insights into a selection of current and future regulatory requirements in the financial sector

For retail banks, the implications now go far beyond compliance programs. Regulation increasingly shapes how systems are designed, how platforms are operated, and how innovation can be deployed. Compliance, resilience, and explainability can no longer be added late in delivery cycles or managed as overlay functions. They must be embedded by design into core systems, data platforms, and operating models - particularly in highly interconnected environments such as open banking, real-time payments, cloud platforms, and AI-enabled processes. As a result, regulatory requirements increasingly define architectural boundaries rather than compliance checklists. As dependencies expand across internal functions, third parties, and ecosystems, regulatory requirements directly determine what can be automated, what can be scaled, and how fast change can occur.

This has created a visible gap between regulatory intent and operational reality. While regulation seeks to enable trust, stability, and fair competition, banks often experience rising cost, increasing complexity, and limited customer-facing value. Sovereignty requirements, explainability constraints, and expanding compliance scopes frequently act as structural friction, slowing innovation and constraining efficiency rather than reinforcing them. This creates a structural innovation dilemma: resilience requirements rise while change capacity declines.

Policymakers increasingly acknowledge this burden. Future initiatives should have the aim to reduce reporting complexity, streamline requirements, and introduce greater proportionality. Yet for retail banks, the benefits remain limited. Regulatory simplification initiatives reduce marginal reporting burden but rarely reverse structural compliance architecture. Much of the regulatory architecture introduced since the crisis is embedded in processes, systems, and organizational structures and cannot be unwound quickly.

As a result, even as the regulatory agenda shifts toward simplification, retail banks continue to operate under the full weight of legacy overregulation while still closing gaps from the post-crisis phase. This persistent “complexity hangover” remains a defining constraint on cost, change capacity, and strategic flexibility - and a key reason why regulation and trust have become first-order design parameters rather than boundary conditions for transformation, shaping not only risk management but capital allocation, technology choices, and strategic optionality.

From Trade-Offs to Strategic Focus: Orchestrating the Four Forces

Taken together, these four forces form a self-reinforcing system of pressure. The system is not additive but multiplicative: pressure compounds rather than accumulates. Addressing any one of them in isolation inevitably increases tension in the others. Attempting to optimize all simultaneously often results in strategic paralysis. Accelerating delivery amplifies resilience and compliance risk. Cost cutting undermines AI scale and customer relevance. Pushing AI without architectural and governance alignment increases complexity and expense.

This dynamic explains why many transformation efforts fail to achieve sustained impact. Banks attempt to balance all forces simultaneously, optimizing locally while complexity grows globally. Despite significant investment, cost structures remain rigid, delivery speed improves only marginally, and strategic optionality erodes. The absence of a clear prioritization logic diffuses capital, management attention, and accountability.

The conclusion is unavoidable: there is no balanced solution to this problem. Structural pressure cannot be neutralized through incremental compromise.

Breaking out of this structural trap requires a deliberate shift - from implicit trade-offs to explicit orchestration. Winning banks do not try to optimize all four forces at once. They consciously prioritize one strategic force as their primary optimization objective and align operating model, technology architecture, governance, and capital allocation around that choice. This strategic anchor determines architecture, capital allocation, governance design, and sequencing of transformation initiatives. The remaining forces are not ignored; they are actively managed within clearly defined, non-negotiable guardrails. They are constrained within predefined risk and complexity tolerances.

This marks the shift from continuous optimization to structural focus - and from reacting to pressure to deliberately shaping strategic outcomes, restoring agency in an environment otherwise dominated by structural constraint.

From Strategic Focus to Structural Levers

Defining a strategic focus clarifies what must be optimized. The decisive challenge is translating this focus into structural change without compounding complexity. Poor sequencing often reproduces the very inefficiencies transformation aims to eliminate.

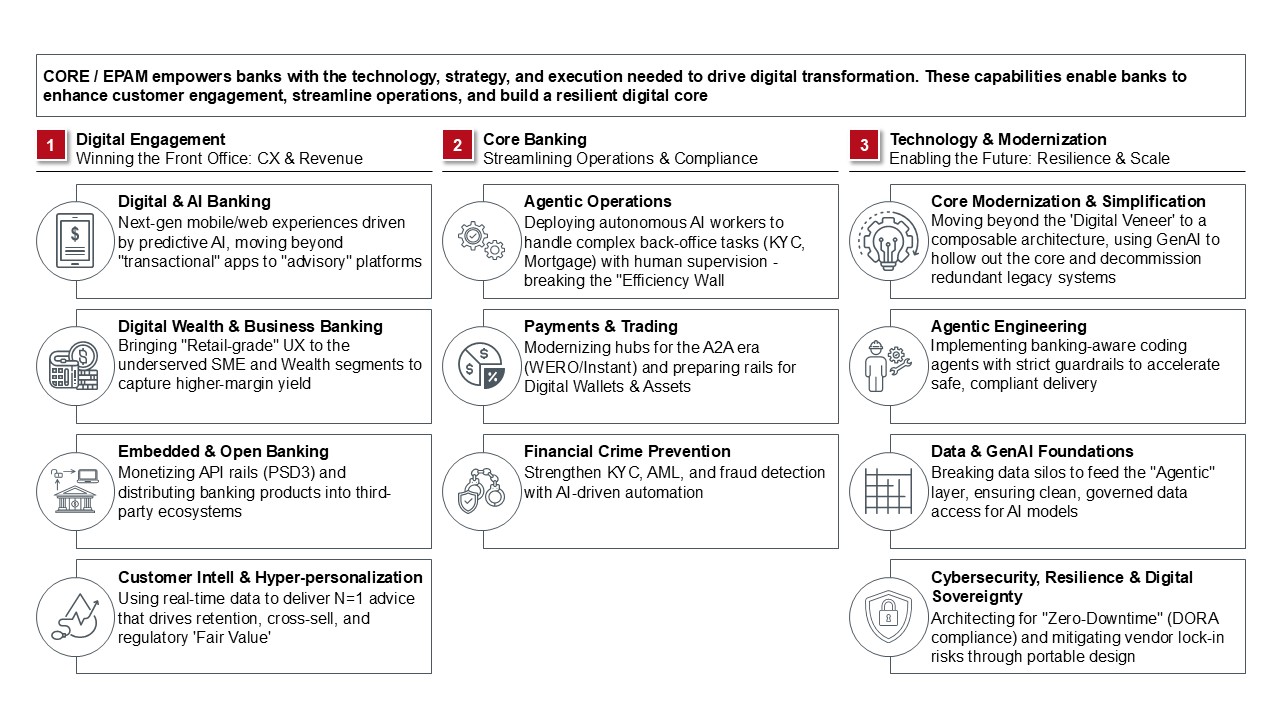

The industry is not short of answers. What is scarce is disciplined selection and architectural coherence. Leading banks are already applying a small number of high‑impact solution patterns to address the four forces in a coherent way. These include shifting from transactional to AI‑driven digital engagement, deploying agentic operations to break the efficiency wall in core processes, modernizing payments and core platforms to regain speed and scalability, and rebuilding data, AI, and resilience foundations so that compliance and trust are embedded by design rather than added as an afterthought. These patterns are not independent initiatives but structural enablers.

What matters is not adopting all of these at once but selecting and sequencing the right combination based on a bank’s strategic priority, starting position, and regulatory context. Sequencing determines whether investments compound or compete. When aligned with a clear strategic anchor, these capabilities become powerful levers for restoring operating leverage, accelerating execution, and rebuilding relevance - rather than isolated initiatives competing for attention and funding.

This is where many transformations succeed or fail: not in the availability of solutions, but in how deliberately they are chosen, orchestrated, and scaled. Structural leverages emerge from coherence, not from initiative volume.

In essence, moving from strategic focus to structural levers requires translating the chosen strategic anchor into a deliberately sequenced set of mutually reinforcing architectural shifts that concentrate resources, reduce complexity, and ensure that transformation compounds around one clear priority rather than fragmenting across competing agendas.

Figure 12: CORE and EPAM strategic capabilities

Figure 12: CORE and EPAM strategic capabilities

Conclusion: From Structural Constraints to Strategic Levers

The profitability surge of 2022–2024 created the appearance of renewed operating leverage. In reality, it deferred rather than resolved structural inefficiencies embedded in European retail banking operating models. As interest rates normalize, the temporary revenue tailwind dissipates while cost bases remain largely fixed.

The resulting scissors effect exposes a structural imbalance: limited pricing power, elevated run-the-bank spending, regulatory cost intensity, and accumulated architectural complexity constrain flexibility precisely when revenue momentum softens.

Incremental efficiency measures, branch rationalization, offshoring, and isolated automation no longer generate material structural relief. The industry is approaching an efficiency wall where further optimization within the existing model yields diminishing returns and increasing fragility.

At the same time, external pressure continues to intensify. Customer expectations shift toward AI-driven orchestration and frictionless digital journeys. AI moves from experimentation to board-level expectation, yet industrialized execution remains limited. Legacy architecture constrains speed and scalability. Regulation and cyber resilience increasingly define architectural boundaries rather than compliance overlays.

These four forces - Cost & Revenue Pressure, AI at Industrial Scale, Legacy & Sovereignty Constraints, and Regulation & Trust as Design Constraints – interact multiplicatively. Addressing one dimension in isolation frequently increases pressure in another. The challenge is therefore not initiative intensity, but structural coherence.

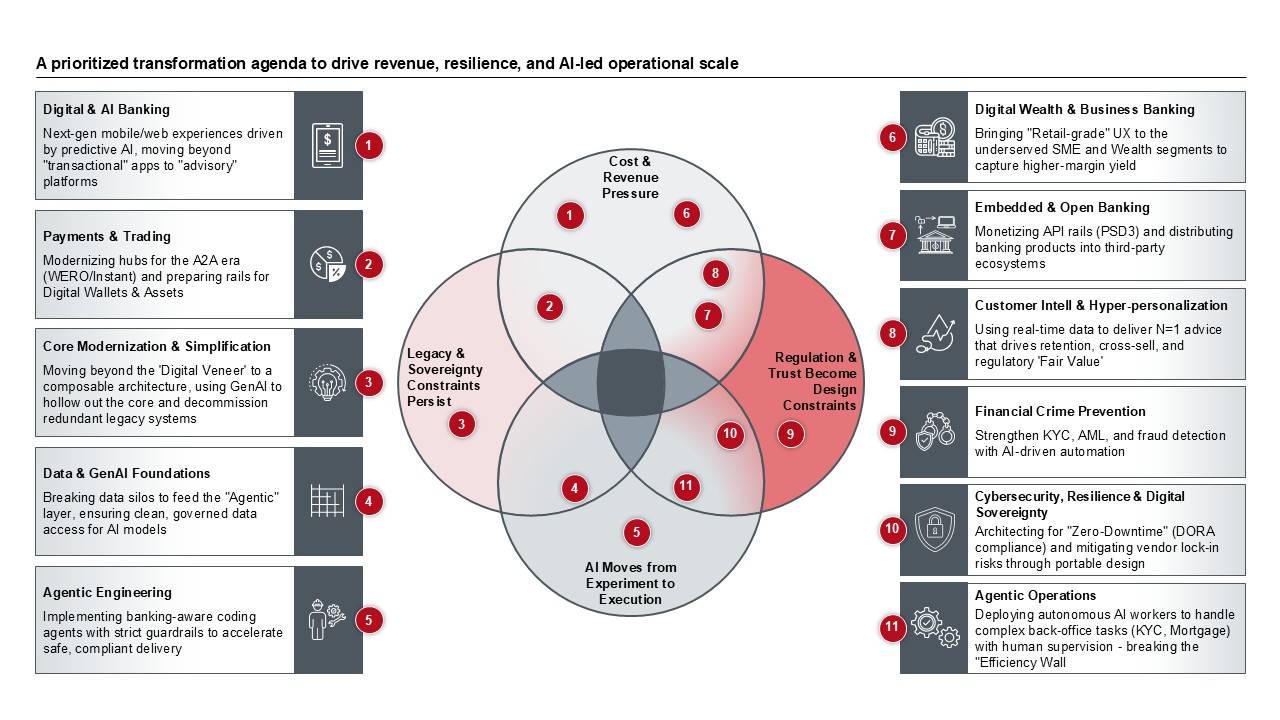

Figure 13: Interconnected capability levers shaping the four structural forces in European retail banking

Figure 13: Interconnected capability levers shaping the four structural forces in European retail banking

Based on our experience supporting large-scale retail banking transformations across Europe, these forces can be translated into a set of interconnected capability clusters within the operating model. Across institutions with varying maturity levels and regulatory contexts, a consistent pattern emerges: sustainable performance improvement is achieved not through isolated programs, but through coordinated capability development that addresses multiple structural pressures simultaneously.

Figure 13 visualizes this translation as the four forces are depicted at the center. The capability clusters are positioned on the left and right. The numbering indicates where each capability exerts structural impact within the four forces. Importantly, each capability is positioned against the force it most directly addresses. This anchoring reflects prioritization - not exclusivity of impact. In practice, most capabilities influence more than one of the four structural forces. Their placement indicates the primary lever, while their effects extend across cost structure, execution capacity, resilience, and revenue depth. The clusters therefore do not represent parallel projects mapped one-to-one to individual forces. They illustrate the operating model levers through which institutions can influence multiple structural constraints at once.

Strengthening these capabilities enables banks to structurally influence margin dynamics, execution capacity, architectural resilience, and customer relevance, ensuring that transformation efforts reinforce rather than counteract one another.

The capability clusters translate the four structural forces into concrete intervention points:

- Capabilities focused on digital engagement and ecosystem integration address revenue pressure by deepening customer relationships and strengthening relevance in a market characterized by rising switching propensity and accelerating feature velocity

- Capabilities centered on resilience, financial crime prevention, and sovereign architecture determine whether scale and automation remain controllable under intensifying regulatory and supervisory scrutiny

- Foundational modernization capabilities - data foundations, AI governance, core simplification, payments modernization, and engineering transformation - shape structural productivity and determine whether AI can be industrialized beyond isolated pilots

Taken together, these capabilities form an interconnected system. They are not additive initiatives, but interdependent adjustment levers. Strengthening one inevitably affects the others. Without robust data foundations, AI cannot scale. Without architectural simplification, automation amplifies complexity. Without resilience by design, speed increases systemic risk. Without revenue reinforcement, cost discipline alone cannot stabilize profitability.

The central task for leadership is therefore prioritization under constraint. Different starting positions - digital maturity, regulatory intensity, legacy depth - require different sequencing. What remains constant is the need for explicit orchestration. Structural improvement does not result from activating all levers simultaneously, but from aligning them around a clearly defined strategic anchor.

Questions? Please ask our experts

Expert - Nicolas Freitag

Nicolas Freitag ist Director bei CORE. Seine Erfahrungen aus der Berufsausbildung zum Bankkaufmann, dem Studium der Wirtschaftswissenschaften und der langjährigen Entwicklung deutschlandweiter Kar...

Mehr lesenNicolas Freitag ist Director bei CORE. Seine Erfahrungen aus der Berufsausbildung zum Bankkaufmann, dem Studium der Wirtschaftswissenschaften und der langjährigen Entwicklung deutschlandweiter Karriere-Netzwerke setzt Nicolas für Klienten bei der Erarbeitung von Unternehmensstrategien, der Entwicklung von digitalen Geschäftsmodellen sowie der Steuerung agiler Software-Entwicklungen ein.

Weniger lesenExpert - Lukas Barthel

Lukas Barthel ist Senior Consultant bei CORE und Teil des Bereichs Finanzdienstleistungsbranche. Er berät Banken und Finanzinstitute bei strategie- und geschäftsorientierten Transformationsinitia...

Mehr lesenLukas Barthel ist Senior Consultant bei CORE und Teil des Bereichs Finanzdienstleistungsbranche. Er berät Banken und Finanzinstitute bei strategie- und geschäftsorientierten Transformationsinitiativen mit Schwerpunkt auf Markt- und Wettbewerbsanalysen, digitalen Geschäftsmodellen und Leistungsbenchmarking. Seine Arbeit unterstützt Führungsteams dabei, fundierte strategische Entscheidungen in Bezug auf Effizienz, Wachstum und skalierbare Betriebsmodelle zu treffen, die direkt auf die strukturellen Herausforderungen des europäischen Privatkundengeschäfts abgestimmt sind.

Weniger lesenExpert - Jan Otis Ernst

Jan Otis Ernst ist Senior Consultant bei CORE und Teil des Bereichs Finanzdienstleistungsbranche. Er unterstützt Banken und Finanzinstitute bei strategie- und technologieorientierten Transformatio...

Mehr lesenJan Otis Ernst ist Senior Consultant bei CORE und Teil des Bereichs Finanzdienstleistungsbranche. Er unterstützt Banken und Finanzinstitute bei strategie- und technologieorientierten Transformationsinitiativen mit den Schwerpunkten IT- und Digitalstrategie, Produktentwicklung und Innovation sowie der Institutionalisierung ergebnisorientierter Governance-Modelle. Seine Arbeit verbindet analytische Strenge mit praktischer Umsetzung und setzt strategische Ziele in umsetzbare Transformationspläne um.

Weniger lesen